Advertisement

- United Kingdom

- /

- Commercial Services

- /

- AIM:CPP

Is CPPGroup Plc (LON:CPP) Potentially Undervalued?

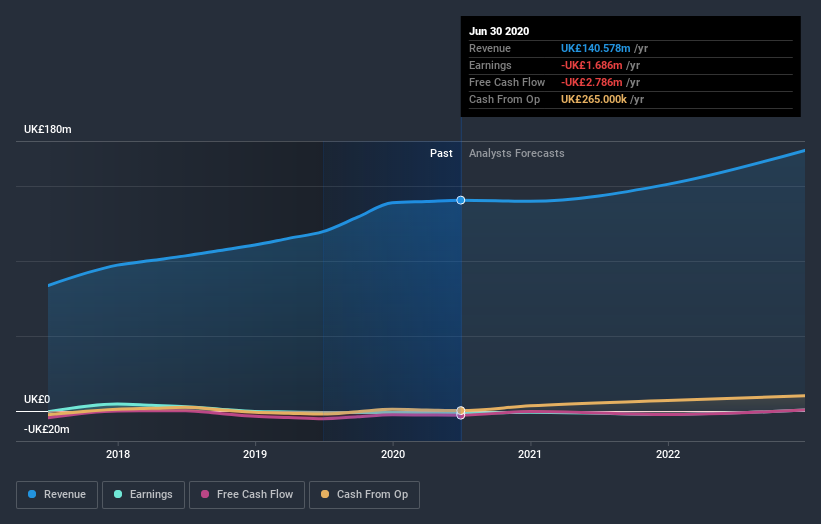

CPPGroup Plc (LON:CPP), is not the largest company out there, but it led the AIM gainers with a relatively large price hike in the past couple of weeks. As a small cap stock, hardly covered by any analysts, there is generally more of an opportunity for mispricing as there is less activity to push the stock closer to fair value. Is there still an opportunity here to buy? Let’s take a look at CPPGroup’s outlook and value based on the most recent financial data to see if the opportunity still exists.

View our latest analysis for CPPGroup

What is CPPGroup worth?

According to my valuation model, CPPGroup seems to be fairly priced at around 16.04% above my intrinsic value, which means if you buy CPPGroup today, you’d be paying a relatively reasonable price for it. And if you believe that the stock is really worth £4.01, there’s only an insignificant downside when the price falls to its real value. Is there another opportunity to buy low in the future? Since CPPGroup’s share price is quite volatile, we could potentially see it sink lower (or rise higher) in the future, giving us another chance to buy. This is based on its high beta, which is a good indicator for how much the stock moves relative to the rest of the market.

What does the future of CPPGroup look like?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. With profit expected to grow by 52% over the next couple of years, the future seems bright for CPPGroup. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What this means for you:

Are you a shareholder? It seems like the market has already priced in CPP’s positive outlook, with shares trading around its fair value. However, there are also other important factors which we haven’t considered today, such as the financial strength of the company. Have these factors changed since the last time you looked at the stock? Will you have enough confidence to invest in the company should the price drop below its fair value?

Are you a potential investor? If you’ve been keeping tabs on CPP, now may not be the most optimal time to buy, given it is trading around its fair value. However, the positive outlook is encouraging for the company, which means it’s worth diving deeper into other factors such as the strength of its balance sheet, in order to take advantage of the next price drop.

If you want to dive deeper into CPPGroup, you'd also look into what risks it is currently facing. While conducting our analysis, we found that CPPGroup has 3 warning signs and it would be unwise to ignore them.

If you are no longer interested in CPPGroup, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

When trading CPPGroup or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About AIM:CPP

CPPGroup

Engages in creating embedded and ancillary real-time assistance products and resolution service in the India, Turkey, and internationally.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$471.3% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17030.5% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.5% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

RO

Robbo on Barclays ·

Why Is Barclays Trading Below Book Value?

Fair Value:UK£5.6416.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DC

DCA_rules on Micron Technology ·

Micron Technology (MU): Riding the AI Supercycle to a $100B+ Revenue Horizon and Historic 40%+ Net Profit Margins

Fair Value:US$1.25k14.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Aoyama Zaisan Networks CompanyLimited ·

Preparing for re-acceleration in FY12/27

Fair Value:JP¥1.31k0.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.2% undervalued

123 followersusers have followed this narrative

2 commentsusers have commented on this narrative

35 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.7% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1926.5% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative