Advertisement

- United Kingdom

- /

- Insurance

- /

- LSE:CRE

Conduit Holdings And 2 Other Undiscovered Gems In The United Kingdom

Simply Wall St

Reviewed by Simply Wall St

The United Kingdom's stock market has recently been influenced by global economic challenges, with the FTSE 100 and FTSE 250 indices experiencing declines due to weak trade data from China. As major companies tied to international markets face headwinds, investors may find opportunities in lesser-known stocks that demonstrate resilience and potential for growth amid these conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| B.P. Marsh & Partners | NA | 29.42% | 31.34% | ★★★★★★ |

| Livermore Investments Group | NA | 9.92% | 13.65% | ★★★★★★ |

| Rights and Issues Investment Trust | NA | -7.93% | -8.41% | ★★★★★★ |

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | 17.28% | 15.80% | ★★★★★★ |

| VH Global Energy Infrastructure | NA | 18.30% | 20.03% | ★★★★★★ |

| Goodwin | 37.02% | 9.75% | 15.68% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| AltynGold | 77.07% | 28.64% | 38.10% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

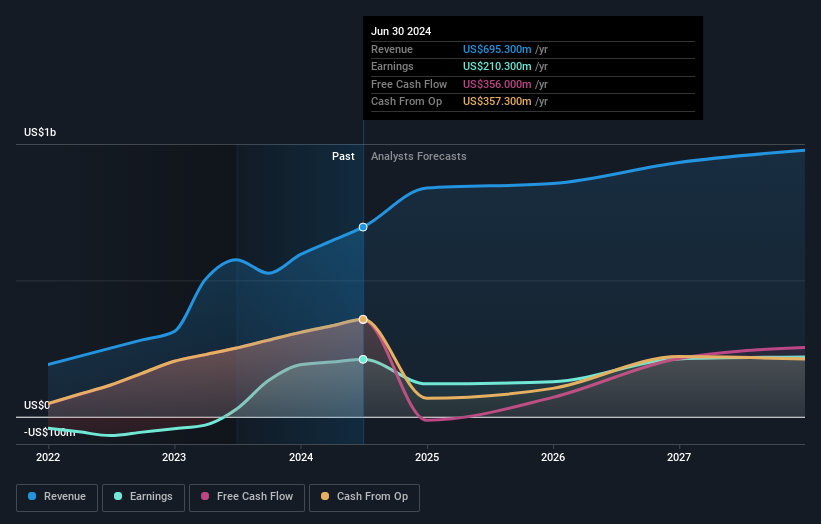

Conduit Holdings (LSE:CRE)

Simply Wall St Value Rating: ★★★★★☆

Overview: Conduit Holdings Limited, along with its subsidiaries, operates globally by offering reinsurance products and services and has a market capitalization of £613 million.

Operations: The company generates revenue from three primary segments: Property ($320 million), Casualty ($174.60 million), and Specialty ($124.30 million).

Conduit Holdings, a small cap player in the UK insurance sector, is showing impressive growth potential with earnings surging by 643% over the past year, far outpacing the industry's -10.3%. Its P/E ratio of 3.8x is notably below the UK market average of 15.5x, indicating good value relative to peers. The company operates debt-free and has consistently maintained this status for five years, eliminating concerns about interest coverage. Despite recent insider selling and a decreased dividend to $0.18 per share for 2024, Conduit's strategic expansion in property and specialty lines suggests promising revenue prospects ahead.

Goodwin (LSE:GDWN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Goodwin PLC, along with its subsidiaries, offers mechanical and refractory engineering solutions across the UK, Europe, the US, the Pacific Basin, and other international markets with a market cap of £527.17 million.

Operations: The company generates revenue from two primary segments: Mechanical (£168.02 million) and Refractory (£75.58 million). The net profit margin shows a notable trend, reflecting the company's efficiency in managing its operations and costs within these segments.

Trading at a significant discount to its estimated fair value, Goodwin has been making waves with a 22.9% earnings growth over the past year, outpacing the broader machinery industry. Its net debt to equity ratio stands at a satisfactory 25.3%, and interest payments are well covered by EBIT at 8.4 times, indicating solid financial health. The company reported half-year sales of £106 million, up from £98 million last year, while net income increased to £11 million from £9 million previously. With high-quality earnings and positive free cash flow trends, Goodwin presents an intriguing opportunity in the UK market.

Mears Group (LSE:MER)

Simply Wall St Value Rating: ★★★★★☆

Overview: Mears Group plc, operating in the United Kingdom, offers a range of outsourced services to both public and private sectors with a market capitalization of £322.52 million.

Operations: Mears Group generates revenue primarily from its Management (£591.63 million) and Maintenance (£551.73 million) segments.

Mears Group, a notable player in the UK, has demonstrated robust earnings growth of 43% over the past year, outpacing its industry peers. With no debt on its books, concerns about interest payments are nonexistent, and this solid financial footing is further supported by high-quality earnings. The company's Price-To-Earnings ratio stands at a favorable 7.8x compared to the broader UK market's 15.5x, suggesting good value for investors. Despite recent board changes and an upcoming shareholder meeting to authorize share repurchases up to 10%, future earnings are projected to decline by an average of nearly 14% annually over the next three years.

- Unlock comprehensive insights into our analysis of Mears Group stock in this health report.

Gain insights into Mears Group's past trends and performance with our Past report.

Next Steps

- Explore the 64 names from our UK Undiscovered Gems With Strong Fundamentals screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:CRE

Conduit Holdings

Through its subsidiary, provides reinsurance products and services worldwide.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor