Advertisement

- United Kingdom

- /

- Construction

- /

- LSE:BBY

New Forecasts: Here's What Analysts Think The Future Holds For Balfour Beatty plc (LON:BBY)

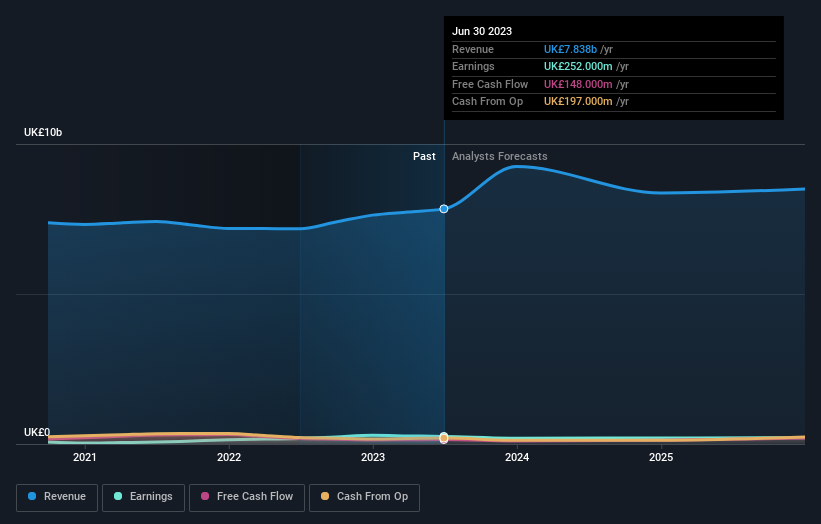

Shareholders in Balfour Beatty plc (LON:BBY) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

After this upgrade, Balfour Beatty's six analysts are now forecasting revenues of UK£9.3b in 2023. This would be a meaningful 18% improvement in sales compared to the last 12 months. Statutory earnings per share are anticipated to plunge 28% to UK£0.33 in the same period. Before this latest update, the analysts had been forecasting revenues of UK£8.3b and earnings per share (EPS) of UK£0.32 in 2023. The forecasts seem more optimistic now, with a nice gain to revenue and a slight bump in earnings per share estimates.

See our latest analysis for Balfour Beatty

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. The analysts are definitely expecting Balfour Beatty's growth to accelerate, with the forecast 39% annualised growth to the end of 2023 ranking favourably alongside historical growth of 2.7% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 3.5% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Balfour Beatty to grow faster than the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts upgraded their earnings per share estimates for this year, expecting improving business conditions. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Balfour Beatty.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Balfour Beatty going out to 2025, and you can see them free on our platform here..

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Balfour Beatty might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:BBY

Balfour Beatty

Balfour Beatty plc finances, develops, builds, maintains, and operates infrastructure in the United Kingdom, the United States, and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor