Ashtead Group (LSE:AHT) is navigating a dynamic environment marked by both opportunities and challenges. Recent highlights include a robust 7% increase in group rental revenue and significant capital investments, juxtaposed against concerns about overvaluation and rising interest expenses. In the discussion that follows, we will delve into Ashtead's financial health, operational strengths, strategic growth initiatives, and external threats to provide a comprehensive overview of the company's current business situation.

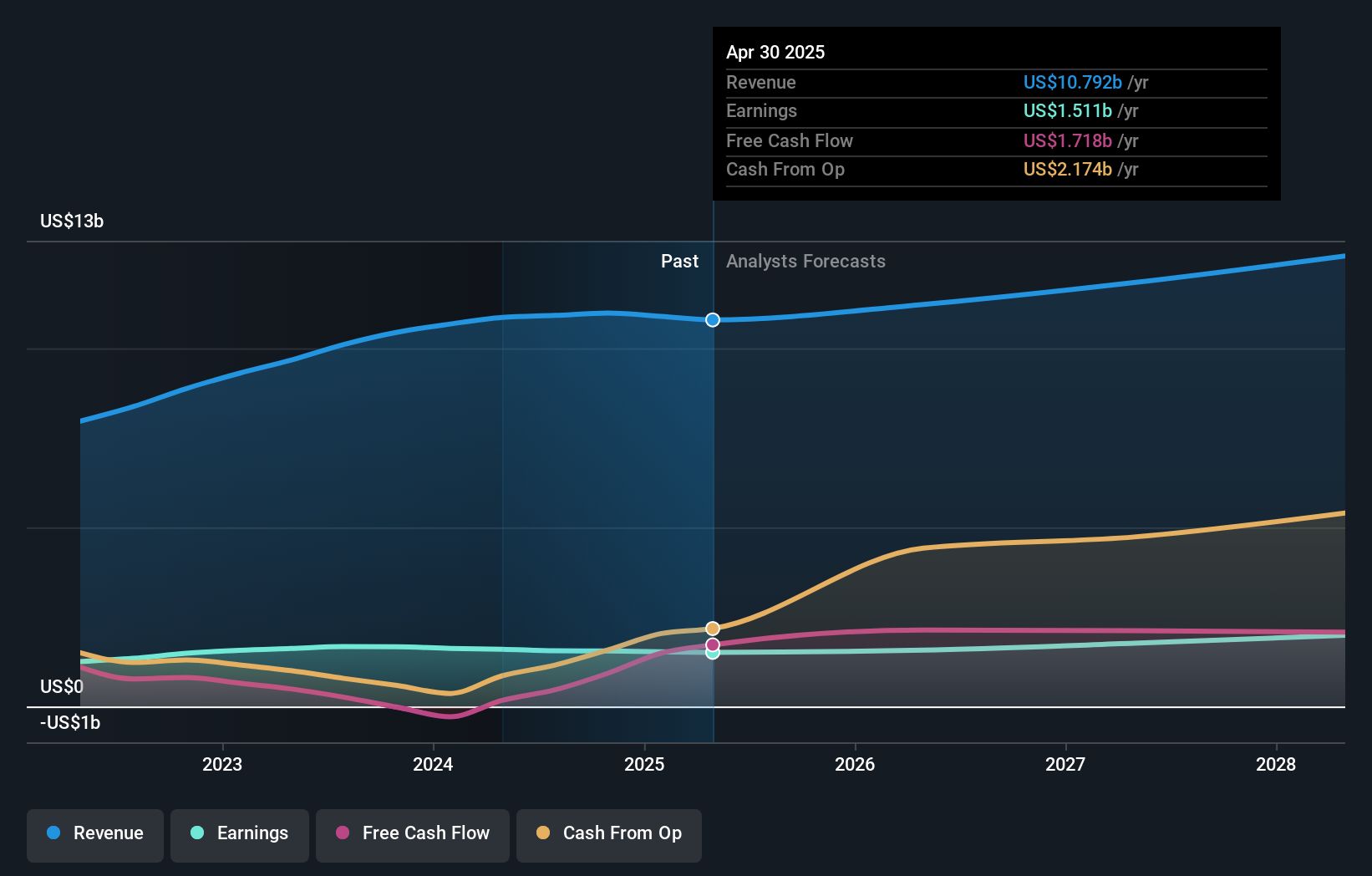

LSE:AHT Earnings and Revenue Growth as at Sep 2024

Advertisement

Strengths: Core Advantages Driving Sustained Success For Ashtead Group

Ashtead Group has demonstrated robust revenue growth, with group rental revenue and total revenue increasing by 7% and 2%, respectively, as highlighted by CEO Brendan Horgan. The group’s EBITDA improved by 5% to a record $1.3 billion, showcasing effective cost management and operational efficiency. Capital investments of $855 million in CapEx have fueled fleet growth and greenfield openings, further solidifying their market position. The company’s debt-to-EBITDA leverage stands at 1.7x, within their long-term range of 1 to 2x, indicating sound debt management. Additionally, Ashtead's strategic market positioning in the UK, with a 6% rental revenue growth driven by market share gains, underscores its competitive advantage.

Weaknesses: Critical Issues Affecting Ashtead Group's Performance and Areas For Growth

Despite its strengths, Ashtead Group faces several challenges. The company is currently trading above its estimated fair value of £29.79, with a share price of £55.7, indicating it may be considered expensive relative to industry standards. This is further supported by its Price-To-Earnings Ratio (20.9x) being higher than the European Trade Distributors industry average (15.3x). Lower used equipment sales and increased depreciation and interest costs on a larger fleet resulted in an adjusted PBT of $573 million and EPS of $0.97. Interest expenses increased by 22% to $144 million, reflecting higher absolute debt levels, as noted by CFO Michael Pratt. Additionally, time utilization was lower than in Q1 last year, impacting overall efficiency.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

Ashtead Group has several growth opportunities on the horizon. The company expanded its North American footprint by 33 locations, including 22 greenfield openings and 11 through acquisitions, as mentioned by Brendan Horgan. The outlook for construction growth is bolstered by megaprojects, which are increasingly contributing to rental revenue. Furthermore, Ashtead's focus on market diversification in Canada aims to increase addressable markets beyond construction, embedded in their 4.0 plan. These strategic moves are expected to enhance Ashtead's market position and capitalize on emerging opportunities.

Threats: Key Risks and Challenges That Could Impact Ashtead Group's Success

Ashtead faces significant market challenges, including the softening of the commercial construction sector due to prolonged higher interest rates, which affects local and regional developers. Competition remains intense, with competitors moderating CapEx, impacting the overall fleet balance in the marketplace. Economic factors, such as potential interest rate adjustments by the Fed, could also influence market dynamics. Additionally, Ashtead's debt is not well covered by operating cash flow, posing a financial risk. These external factors could threaten Ashtead's growth and market share if not managed effectively.

Conclusion

Ashtead Group's robust revenue growth and effective cost management, evidenced by a record $1.3 billion in EBITDA, highlight its operational efficiency and strong market positioning. However, the company's current share price of £55.7, significantly above its estimated fair value of £29.79, suggests it may be considered expensive relative to industry standards, despite being a good value compared to its peers. While strategic expansions and market diversification present substantial growth opportunities, challenges such as higher interest expenses and intense competition could impact future performance. Therefore, while Ashtead is well-positioned for growth, potential investors should weigh these factors carefully when considering its future outlook.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About LSE:AHT

Ashtead Group

Engages in the construction, industrial, and general equipment rental business under the Sunbelt Rentals brand name in the United States, the United Kingdom, and Canada.