Advertisement

- United Kingdom

- /

- Trade Distributors

- /

- AIM:BMT

We Think The Compensation For Braime Group PLC's (LON:BMT) CEO Looks About Right

Key Insights

- Braime Group to hold its Annual General Meeting on 17th of June

- CEO Carl Braime's total compensation includes salary of UK£196.0k

- The total compensation is 39% less than the average for the industry

- Braime Group's three-year loss to shareholders was 40% while its EPS grew by 51% over the past three years

Performance at Braime Group PLC (LON:BMT) has been rather uninspiring recently and shareholders may be wondering how CEO Carl Braime plans to fix this. At the next AGM coming up on 17th of June, they can influence managerial decision making through voting on resolutions, including executive remuneration. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. In our opinion, CEO compensation does not look excessive and we discuss why.

View our latest analysis for Braime Group

How Does Total Compensation For Carl Braime Compare With Other Companies In The Industry?

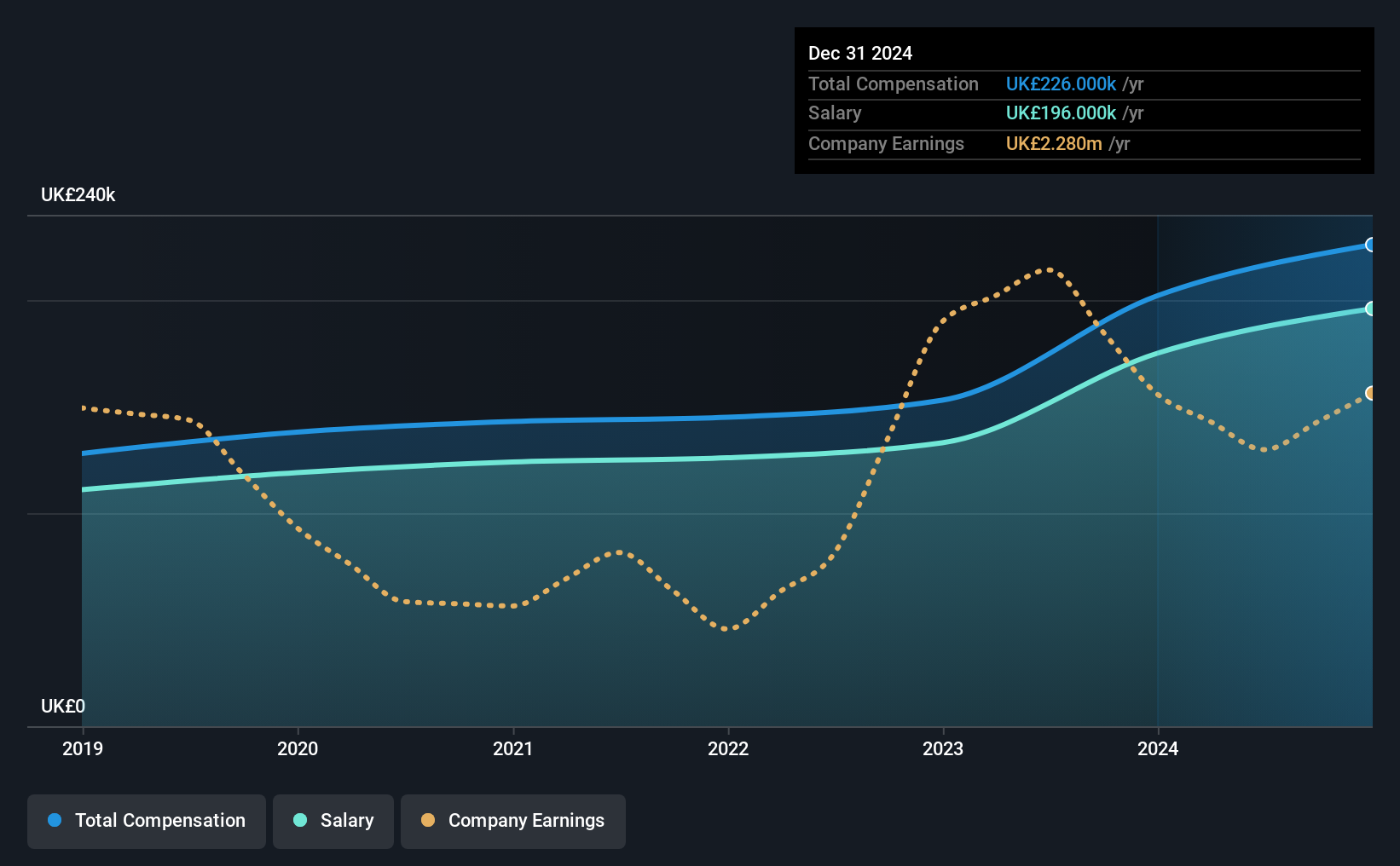

Our data indicates that Braime Group PLC has a market capitalization of UK£16m, and total annual CEO compensation was reported as UK£226k for the year to December 2024. Notably, that's an increase of 12% over the year before. Notably, the salary which is UK£196.0k, represents most of the total compensation being paid.

For comparison, other companies in the British Trade Distributors industry with market capitalizations below UK£148m, reported a median total CEO compensation of UK£373k. In other words, Braime Group pays its CEO lower than the industry median. Moreover, Carl Braime also holds UK£325k worth of Braime Group stock directly under their own name.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | UK£196k | UK£175k | 87% |

| Other | UK£30k | UK£27k | 13% |

| Total Compensation | UK£226k | UK£202k | 100% |

Talking in terms of the industry, salary represented approximately 59% of total compensation out of all the companies we analyzed, while other remuneration made up 41% of the pie. According to our research, Braime Group has allocated a higher percentage of pay to salary in comparison to the wider industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Braime Group PLC's Growth

Braime Group PLC has seen its earnings per share (EPS) increase by 51% a year over the past three years. Its revenue is up 1.6% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's good to see a bit of revenue growth, as this suggests the business is able to grow sustainably. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Braime Group PLC Been A Good Investment?

The return of -40% over three years would not have pleased Braime Group PLC shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

The fact that shareholders are sitting on a loss is certainly disheartening. This diverges with the robust growth in EPS, suggesting that there is a large discrepancy between share price and fundamentals. There needs to be more focus by management and the board to examine why the share price has diverged from fundamentals. In the upcoming AGM, shareholders will get the opportunity to discuss these concerns with the board and assess if the board's plan is likely to improve company performance.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 2 warning signs for Braime Group that investors should think about before committing capital to this stock.

Important note: Braime Group is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Braime Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:BMT

Braime Group

Engages in the distribution of bulk material handling components and monitoring equipment in the United Kingdom, Rest of Europe, the Middle East, the United States, Africa, Australia, and Asia.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor