Advertisement

- United Kingdom

- /

- Trade Distributors

- /

- AIM:ASY

Uncovering Andrews Sykes Group And 2 Hidden Small Cap Gems In The UK Market

Simply Wall St

Reviewed by Simply Wall St

Over the last 7 days, the United Kingdom market has remained flat, yet it has shown a robust growth of 11% over the past year with earnings projected to increase by 14% annually in the coming years. In such a dynamic environment, identifying stocks like Andrews Sykes Group and other small-cap gems can be crucial for investors seeking opportunities that align with these promising market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| B.P. Marsh & Partners | NA | 24.01% | 24.81% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | 17.28% | 15.80% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Kodal Minerals | NA | nan | 72.74% | ★★★★★★ |

| VH Global Sustainable Energy Opportunities | NA | 18.30% | 20.03% | ★★★★★★ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

We're going to check out a few of the best picks from our screener tool.

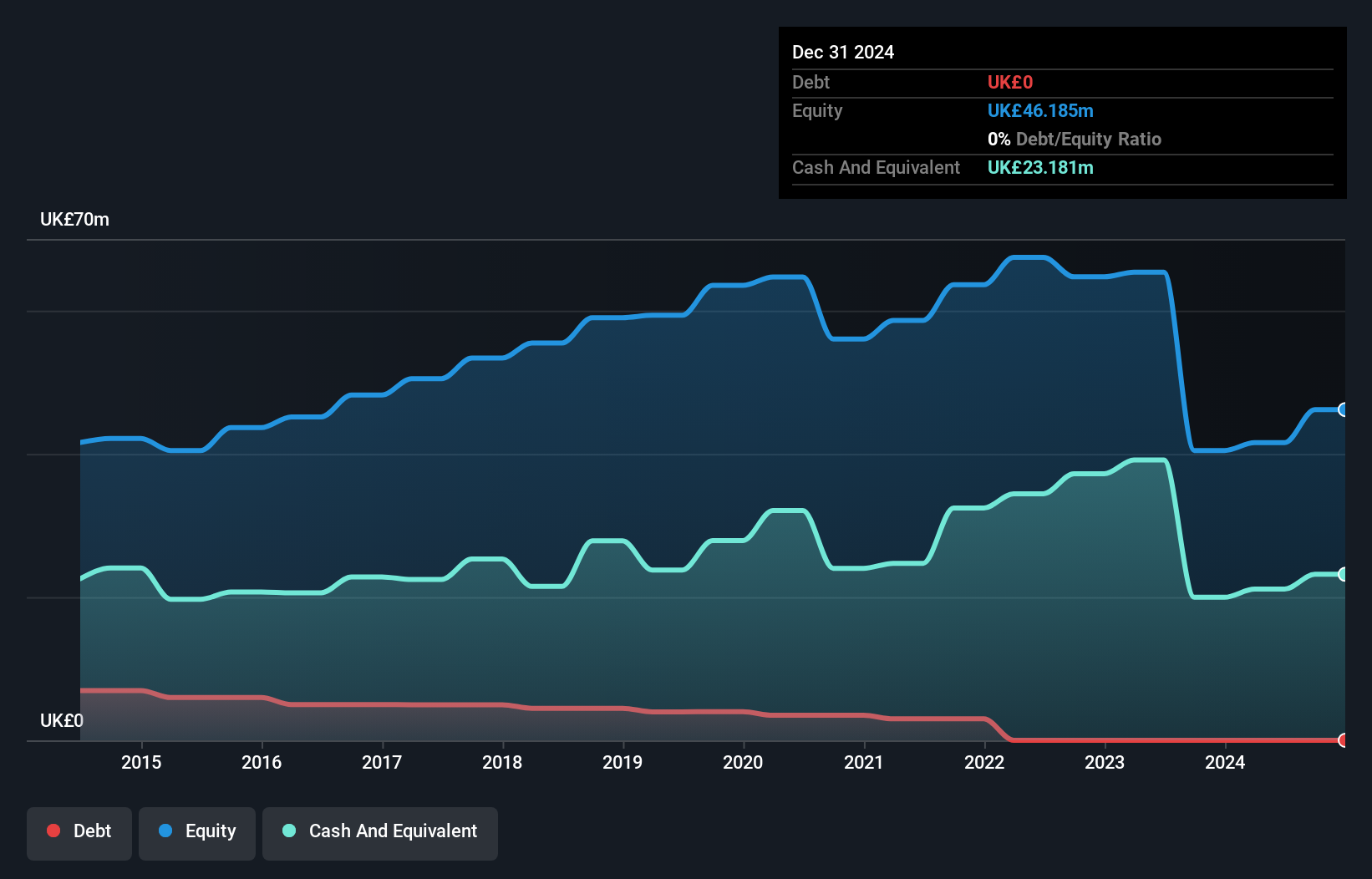

Andrews Sykes Group (AIM:ASY)

Simply Wall St Value Rating: ★★★★★★

Overview: Andrews Sykes Group plc is an investment holding company involved in the hire, sale, and installation of environmental control equipment across the United Kingdom, Europe, the Middle East, Africa, and internationally with a market capitalization of £222.90 million.

Operations: The company generates revenue primarily through the hire, sale, and installation of environmental control equipment across various regions. It operates with a market capitalization of £222.90 million.

Andrews Sykes Group, a UK-based company, stands out with its debt-free balance sheet and high-quality earnings. Despite a slight dip in earnings growth at -4.3%, it fares better than the industry average of -5.6%. Trading at 39.8% below its estimated fair value, this stock appears undervalued. The firm reported sales of £38.39 million for the half-year ending June 2024, compared to £38.84 million previously, with net income reaching £7.08 million versus last year's £7.53 million; basic EPS was GBP 0.169 against GBP 0.1788 prior year figures show consistent performance amidst challenges.

- Click here to discover the nuances of Andrews Sykes Group with our detailed analytical health report.

Gain insights into Andrews Sykes Group's past trends and performance with our Past report.

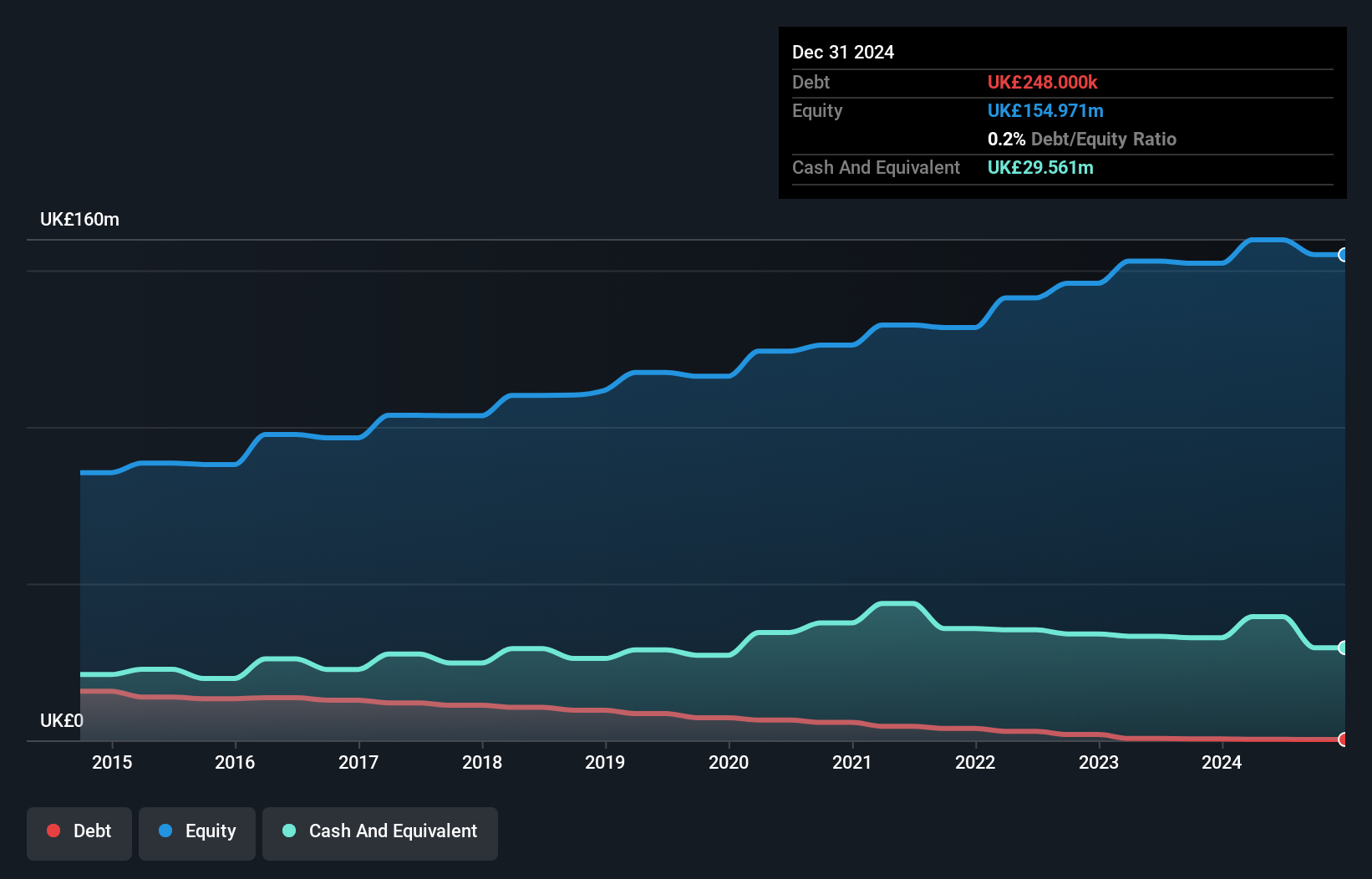

London Security (AIM:LSC)

Simply Wall St Value Rating: ★★★★★★

Overview: London Security plc is an investment holding company that manufactures, sells, and rents fire protection equipment across several European countries, with a market cap of £465.88 million.

Operations: Revenue for London Security plc primarily comes from the provision and maintenance of fire protection and security equipment, amounting to £221.72 million.

London Security, a smaller player in the UK market, has shown financial resilience with its debt to equity ratio dropping from 7.3% to 0.2% over five years. The firm is trading at 50.3% below estimated fair value, suggesting potential undervaluation. Recent earnings for the half-year show sales of £110.86 million and net income of £9.59 million, slightly lower than last year’s figures but still robust given industry challenges. Notably, earnings growth outpaced the machinery sector's decline by achieving a 5.2% increase this past year, indicating strong operational performance amidst broader industry struggles.

AO World (LSE:AO.)

Simply Wall St Value Rating: ★★★★★☆

Overview: AO World plc operates as an online retailer specializing in domestic appliances and ancillary services across the United Kingdom and Germany, with a market capitalization of £615.58 million.

Operations: AO World generates revenue primarily from its online retailing of domestic appliances and ancillary services, totaling £1.04 billion. The company's financial performance is influenced by its gross profit margin trends.

AO World, a standout in the UK market, has shown impressive financial resilience with earnings growth of 298% over the past year, outpacing the Specialty Retail sector's -4.5%. The company trades at 11% below its estimated fair value and maintains a debt-to-equity ratio that improved from 37.2% to just 1.5% in five years. With interest payments well-covered by EBIT at 9.1x and positive free cash flow standing at £53 million as of October 2024, AO World appears financially robust despite recent insider selling activity over the last quarter.

- Get an in-depth perspective on AO World's performance by reading our health report here.

Review our historical performance report to gain insights into AO World's's past performance.

Taking Advantage

- Gain an insight into the universe of 81 UK Undiscovered Gems With Strong Fundamentals by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:ASY

Andrews Sykes Group

An investment holding company, engages in the hire, sale, and installation of environmental control equipment in the United Kingdom, rest of Europe, the Middle East, Africa, and internationally.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor