- United Kingdom

- /

- Diversified Financial

- /

- LSE:OSB

OSB Group's (LON:OSB) Shareholders Will Receive A Bigger Dividend Than Last Year

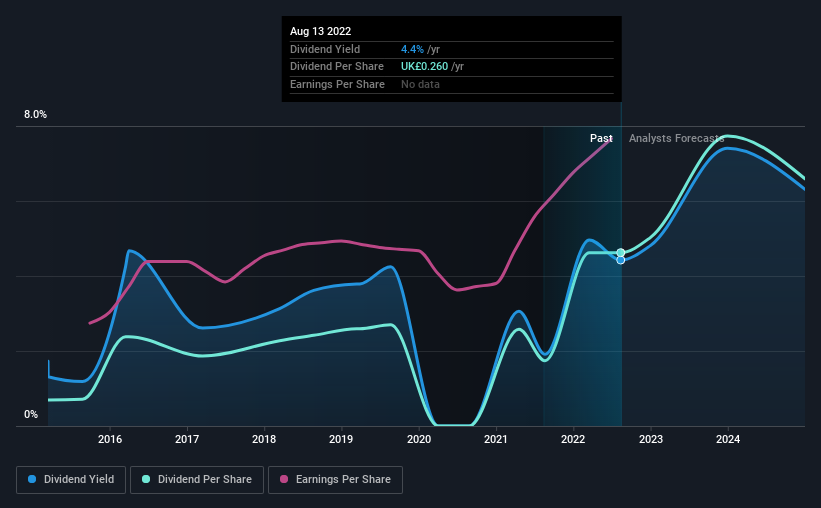

The board of OSB Group Plc (LON:OSB) has announced that it will be increasing its dividend by 78% on the 21st of September to £0.087, up from last year's comparable payment of £0.049. This takes the annual payment to 4.4% of the current stock price, which is about average for the industry.

Check out our latest analysis for OSB Group

OSB Group's Earnings Will Easily Cover The Distributions

We like to see a healthy dividend yield, but that is only helpful to us if the payment can continue.

OSB Group has established itself as a dividend paying company, given its 7-year history of distributing earnings to shareholders. Past distributions do not necessarily guarantee future ones, but OSB Group's payout ratio of 35% is a good sign for current shareholders as this means that earnings decently cover dividends.

The next 3 years are set to see EPS grow by 31.4%. Analysts forecast the future payout ratio could be 39% over the same time horizon, which is a number we think the company can maintain.

OSB Group's Dividend Has Lacked Consistency

It's comforting to see that OSB Group has been paying a dividend for a number of years now, however it has been cut at least once in that time. This suggests that the dividend might not be the most reliable. The annual payment during the last 7 years was £0.039 in 2015, and the most recent fiscal year payment was £0.26. This means that it has been growing its distributions at 31% per annum over that time. OSB Group has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. OSB Group has seen EPS rising for the last five years, at 15% per annum. A low payout ratio and decent growth suggests that the company is reinvesting well, and it also has plenty of room to increase the dividend over time.

OSB Group Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. Distributions are quite easily covered by earnings, which are also being converted to cash flows. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, OSB Group has 2 warning signs (and 1 which is concerning) we think you should know about. Is OSB Group not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:OSB

OSB Group

Through its subsidiaries, operates as a specialist mortgage lending company in the United Kingdom and India.

Undervalued with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion