HSBC Holdings (LSE:HSBA) has delivered a return of 12% over the past month, building on a strong year so far for the banking group. With steady revenue and rising net income, investors are paying close attention.

Momentum has definitely been building for HSBC Holdings, with a sharp 12% share price return over the past month, adding to an already impressive 43% gain year-to-date. In addition, the company’s total shareholder return of 67% over the last twelve months and nearly 190% across three years highlights a compelling track record that continues to catch investors’ attention.

With shares surging and the company’s fundamentals improving, the key question now is whether HSBC still trades at a discount or if the market has already priced in future growth, leaving little room for upside.

Advertisement

Most Popular Narrative: 5% Overvalued

HSBC Holdings recently closed at £11.20, while the most popular narrative places fair value at £10.66. This suggests current optimism has pushed the price above what analysts expect, and sets up a clash between recent performance and long-term expectations.

The strategic shift away from underperforming and non-core businesses in Europe and the Americas, and redeployment of capital into high-return businesses in Asia and the Middle East is expected to improve overall net interest margins and boost group return on equity through better allocation of resources. Disproportionate investment in digital transformation, including AI-driven efficiency gains and digital onboarding, will generate structural cost reductions (organizational simplification savings), directly improving the cost-to-income ratio and lifting long-term operating leverage and net margins.

Want to know what calculated bets underlie this bold price call? The linchpin is a projected transformation in profitability, led by management’s geographic pivot and ambitious tech upgrades. If you are curious about the earnings and margin leaps that support this outlook, take a closer look at the numbers that drive this narrative’s fair value.

However, persistent volatility in Asian markets and mounting commercial real estate risks could quickly undermine the current optimism surrounding HSBC's growth outlook.

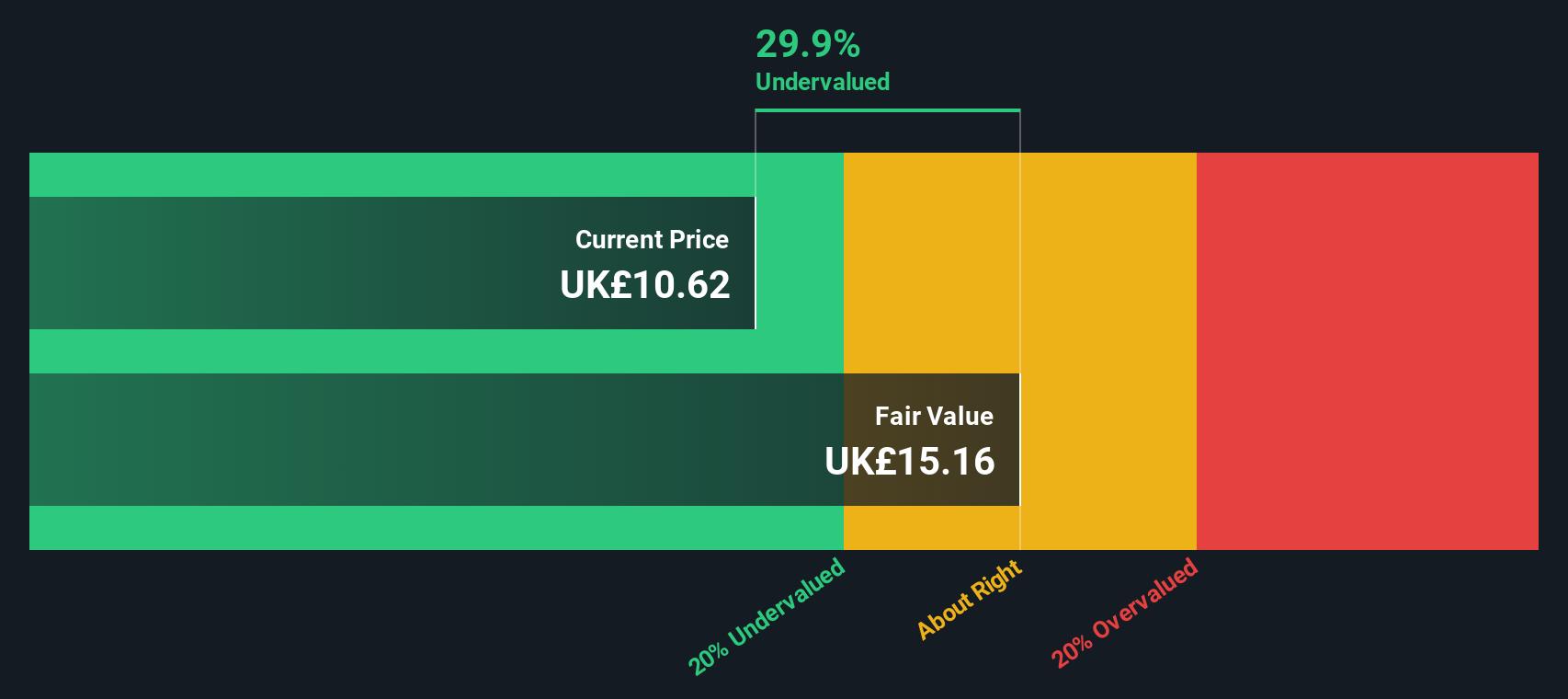

Another View: Discounted Cash Flow Says Undervalued

Taking a contrasting approach, our SWS DCF model values HSBC at £16.60 per share. This is well above the current price and suggests the market might be overlooking long-term cash flow potential, even as other metrics flag overvaluation. Could this signal an opportunity beneath the recent optimism?

If you'd rather dig into the numbers and shape your own perspective, you can easily build a personalized narrative in just a few minutes. Do it your way.

Smart investors know the next opportunity is never far away. Act now and expand your horizons with tailored stock ideas. Don’t let new winners slip by.

Seize the tech revolution by tapping into these 27 AI penny stocks that power breakthroughs in automation, machine learning, and future-focused industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if HSBC Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.