Advertisement

€6.63 - That's What Analysts Think CS Communication & Systemes SA (EPA:SX) Is Worth After These Results

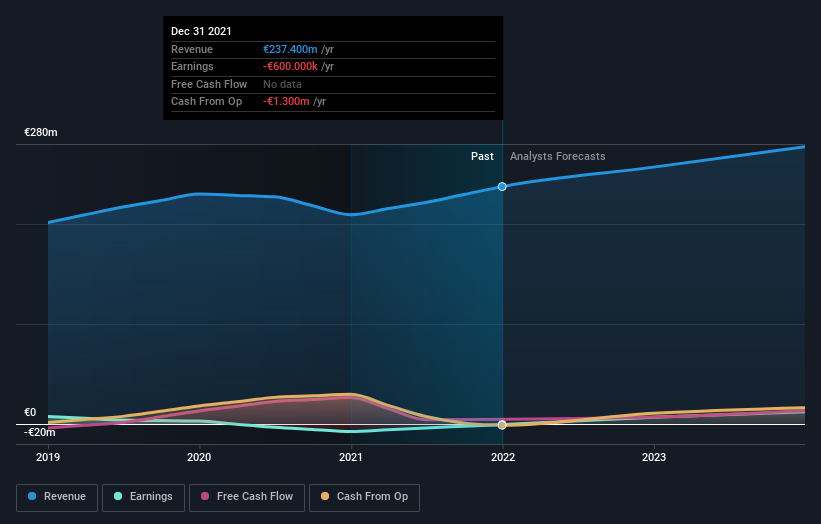

Shareholders might have noticed that CS Communication & Systemes SA (EPA:SX) filed its yearly result this time last week. The early response was not positive, with shares down 2.7% to €6.38 in the past week. It was an okay report, and revenues came in at €237m, approximately in line with analyst estimates leading up to the results announcement. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

See our latest analysis for CS Communication & Systemes

Taking into account the latest results, the most recent consensus for CS Communication & Systemes from three analysts is for revenues of €256.9m in 2022 which, if met, would be a decent 8.2% increase on its sales over the past 12 months. CS Communication & Systemes is also expected to turn profitable, with statutory earnings of €0.24 per share. Yet prior to the latest earnings, the analysts had been anticipated revenues of €257.4m and earnings per share (EPS) of €0.30 in 2022. So there's definitely been a decline in sentiment after the latest results, noting the substantial drop in new EPS forecasts.

Despite cutting their earnings forecasts,the analysts have lifted their price target 11% to €6.63, suggesting that these impacts are not expected to weigh on the stock's value in the long term. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic CS Communication & Systemes analyst has a price target of €7.00 per share, while the most pessimistic values it at €6.00. This is a very narrow spread of estimates, implying either that CS Communication & Systemes is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that CS Communication & Systemes' rate of growth is expected to accelerate meaningfully, with the forecast 8.2% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 6.3% p.a. over the past five years. Other similar companies in the industry (with analyst coverage) are also forecast to grow their revenue at 8.6% per year. CS Communication & Systemes is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple CS Communication & Systemes analysts - going out to 2023, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 1 warning sign for CS Communication & Systemes that you should be aware of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:SX

CS Communication & Systemes

CS Communication & Systemes SA designs, integrates, and operates mission critical systems worldwide.

Reasonable growth potential and slightly overvalued.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1157.5% undervalued

41 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.4% undervalued

61 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19013.7% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

JA

Jamesiskindacool on Woodside Energy Group ·

Does WDS Have More in the Tank?

Fair Value:AU$36.611.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Jamesiskindacool on Treasury Wine Estates ·

Is TWE Aging Well?

Fair Value:AU$7.0733.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JA

Jamesiskindacool on Transurban Group ·

Is TCL Worth the Toll?

Fair Value:AU$14.252.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

78 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.6% undervalued

71 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.1% undervalued

181 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative