Exploring None's High Growth Tech Stocks For Future Potential

Reviewed by Simply Wall St

In recent weeks, global markets have been marked by volatility, with small-cap stocks underperforming their larger counterparts and inflation fears contributing to a downward trend in U.S. equities. Amidst this backdrop, investors are keenly evaluating high-growth tech stocks for their potential to weather economic uncertainties and capitalize on evolving technological trends.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Ascelia Pharma | 76.15% | 47.16% | ★★★★★★ |

| CD Projekt | 23.18% | 27.00% | ★★★★★★ |

| Waystream Holding | 22.09% | 113.25% | ★★★★★★ |

| AVITA Medical | 33.33% | 51.81% | ★★★★★★ |

| Alkami Technology | 21.99% | 102.65% | ★★★★★★ |

| Pharma Mar | 25.43% | 56.19% | ★★★★★★ |

| Alnylam Pharmaceuticals | 21.39% | 56.40% | ★★★★★★ |

| TG Therapeutics | 30.33% | 44.07% | ★★★★★★ |

| Elliptic Laboratories | 70.09% | 111.37% | ★★★★★★ |

| Travere Therapeutics | 29.92% | 61.97% | ★★★★★★ |

Click here to see the full list of 1224 stocks from our High Growth Tech and AI Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

Planisware SAS (ENXTPA:PLNW)

Simply Wall St Growth Rating: ★★★★☆☆

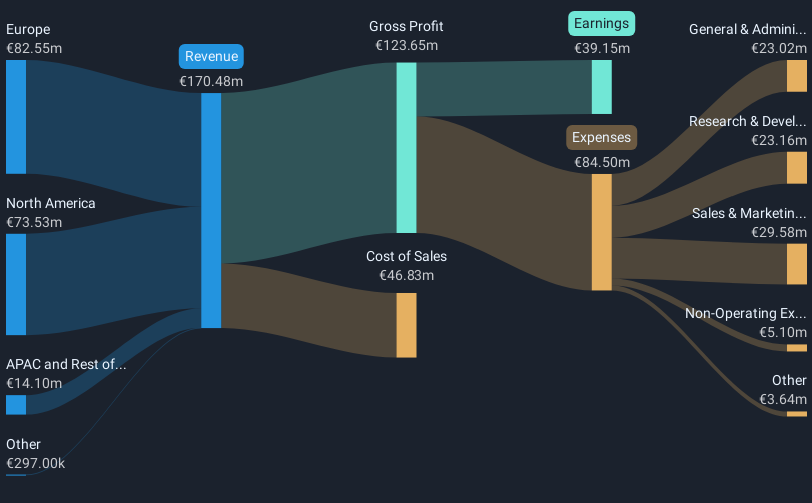

Overview: Planisware SAS is a business-to-business software-as-a-service provider with operations in Europe, the Americas, the Asia-Pacific, and internationally, and it has a market cap of €1.77 billion.

Operations: The company generates revenue primarily from its Software & Programming segment, amounting to €170.48 million. As a business-to-business software-as-a-service provider, it serves clients across various regions including Europe, the Americas, and Asia-Pacific.

Planisware SAS, a participant in the competitive software sector, recently showcased its strategies at the CIC Market Solutions Forum, reflecting its proactive stance in market engagement. With earnings projected to grow by 18.1% annually, outpacing the French market's 12.3%, Planisware demonstrates robust financial health and an upward trajectory in profitability. Despite lagging behind the industry growth rate last year, its revenue growth forecasts remain promising at 14.5% per year, suggesting a strong alignment with market demands and potential for sustained expansion. This performance is underpinned by high-quality earnings and an anticipated return on equity of 23.9% in three years, positioning Planisware well within a landscape that increasingly values technological innovation and effective capital deployment.

- Get an in-depth perspective on Planisware SAS' performance by reading our health report here.

Gain insights into Planisware SAS' past trends and performance with our Past report.

DAEDUCK ELECTRONICS (KOSE:A353200)

Simply Wall St Growth Rating: ★★★★☆☆

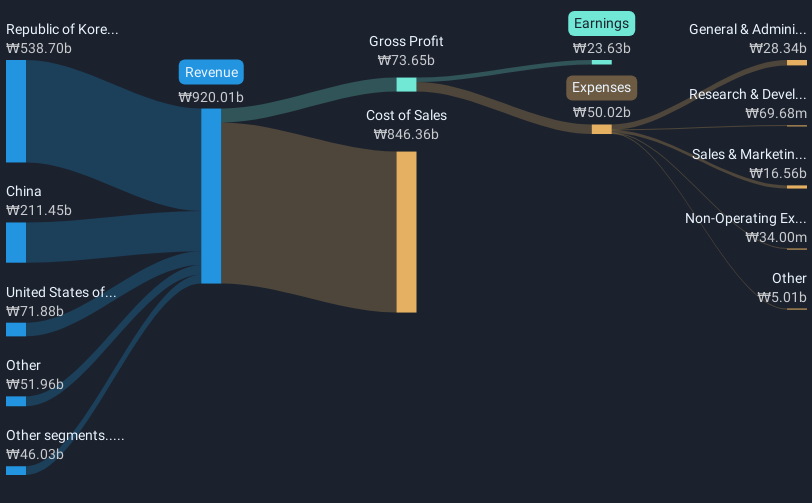

Overview: Daeduck Electronics Co., Ltd. specializes in the production and distribution of printed circuit boards (PCBs) both domestically in South Korea and internationally, with a market capitalization of approximately ₩801.85 billion.

Operations: Daeduck Electronics Co., Ltd. generates revenue primarily from the manufacture and sale of printed circuit boards (PCBs), amounting to approximately ₩920 billion. The company's operations span both domestic and international markets, contributing significantly to its financial performance.

DAEDUCK ELECTRONICS has demonstrated a robust growth trajectory with an expected annual earnings increase of 58%, significantly outpacing the South Korean market's forecast of 29%. This performance is anchored by a solid revenue growth rate of 13.2% per year, which exceeds the domestic market average of 9.2%. The company’s commitment to innovation is evident in its R&D spending, crucial for sustaining its competitive edge in the fast-evolving tech landscape. Recent financial results underscore this potential, with net income rising to KRW 19,378.71 million over nine months, up from KRW 19,285.59 million in the previous year, reflecting not only growth but also resilience and adaptability in challenging market conditions.

- Click here and access our complete health analysis report to understand the dynamics of DAEDUCK ELECTRONICS.

Understand DAEDUCK ELECTRONICS' track record by examining our Past report.

Oracle Corporation Japan (TSE:4716)

Simply Wall St Growth Rating: ★★★★☆☆

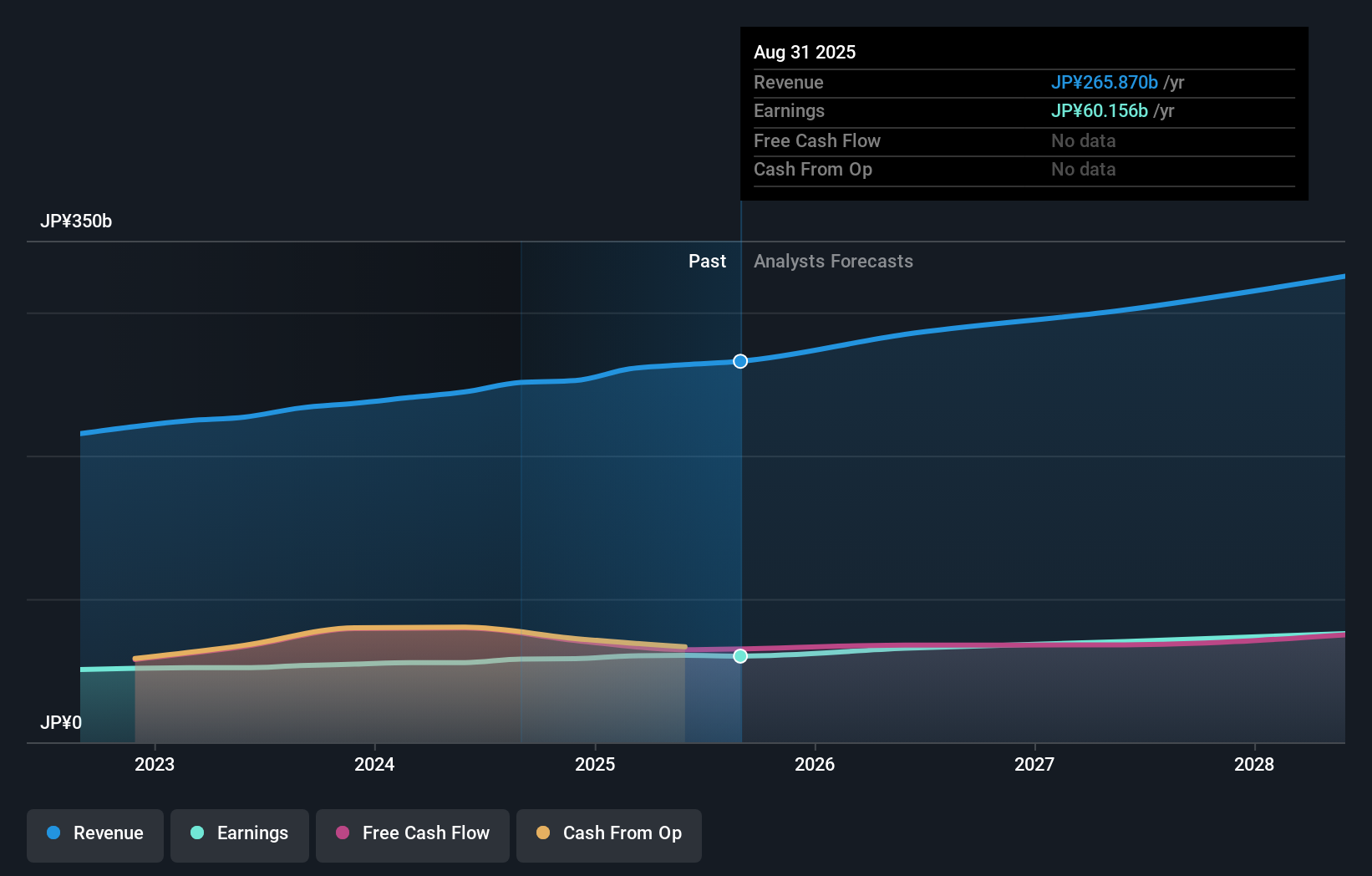

Overview: Oracle Corporation Japan focuses on developing and selling software and hardware products and solutions within Japan, with a market capitalization of ¥1.80 trillion.

Operations: Oracle Corporation Japan generates revenue primarily through its software and hardware product sales and related solutions in the Japanese market. The company's operations are centered on leveraging its technological offerings to cater to diverse business needs within the region.

Oracle Corporation Japan is charting a steady course in the tech sector with its expected annual revenue growth of 7.4%, outpacing the Japanese market's average of 4.2%. This growth is supported by an anticipated earnings increase of 8.6% annually, slightly above the national trend of 8%. The firm's commitment to innovation is reflected in its R&D spending, vital for maintaining competitiveness in a rapidly evolving industry. Notably, Oracle Japan’s recent preparations for their Q2 earnings report on December 20, 2024, underscore their proactive approach in transparency and market communication.

Summing It All Up

- Access the full spectrum of 1224 High Growth Tech and AI Stocks by clicking on this link.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:PLNW

Planisware SAS

Operates as a business-to-business software-as-a-service provider in Europe, the Americas, the Asia-Pacific, and internationally.

Excellent balance sheet with reasonable growth potential.