Advertisement

- France

- /

- Semiconductors

- /

- ENXTPA:XFAB

Earnings Release: Here's Why Analysts Cut Their X-FAB Silicon Foundries SE (EPA:XFAB) Price Target To €11.78

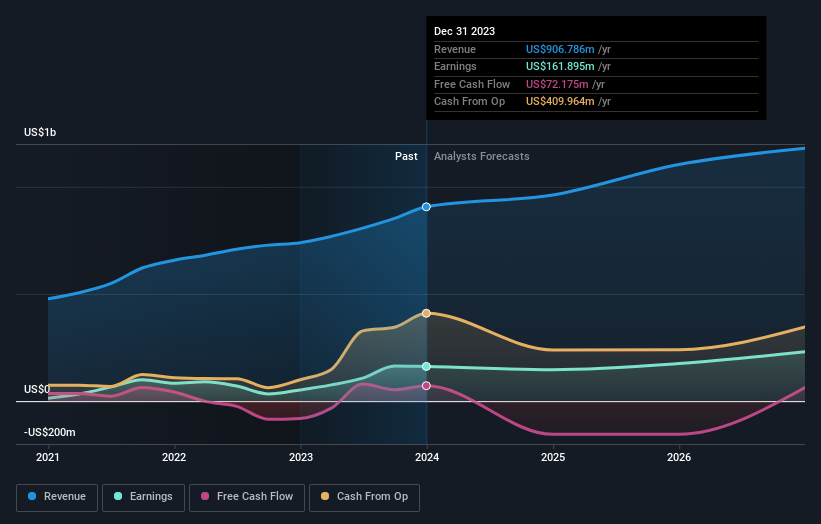

There's been a notable change in appetite for X-FAB Silicon Foundries SE (EPA:XFAB) shares in the week since its annual report, with the stock down 12% to €7.82. The result was positive overall - although revenues of US$907m were in line with what the analysts predicted, X-FAB Silicon Foundries surprised by delivering a statutory profit of US$1.24 per share, modestly greater than expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

View our latest analysis for X-FAB Silicon Foundries

Taking into account the latest results, the consensus forecast from X-FAB Silicon Foundries' seven analysts is for revenues of US$961.8m in 2024. This reflects a modest 6.1% improvement in revenue compared to the last 12 months. Statutory earnings per share are forecast to reduce 9.2% to US$1.13 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.00b and earnings per share (EPS) of US$1.19 in 2024. The analysts are less bullish than they were before these results, given the reduced revenue forecasts and the small dip in earnings per share expectations.

It'll come as no surprise then, to learn that the analysts have cut their price target 7.1% to €11.78. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on X-FAB Silicon Foundries, with the most bullish analyst valuing it at €12.96 and the most bearish at €9.98 per share. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. We would highlight that X-FAB Silicon Foundries' revenue growth is expected to slow, with the forecast 6.1% annualised growth rate until the end of 2024 being well below the historical 12% p.a. growth over the last five years. Compare this to the 6 other companies in this industry with analyst coverage, which are forecast to grow their revenue at 6.9% per year. So it's pretty clear that, while X-FAB Silicon Foundries' revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for X-FAB Silicon Foundries. Sadly, they also downgraded their revenue forecasts, but the business is still expected to grow at roughly the same rate as the industry itself. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of X-FAB Silicon Foundries' future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for X-FAB Silicon Foundries going out to 2026, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:XFAB

X-FAB Silicon Foundries

Develops, produces, and sells analog/mixed-signal IC, micro-electro-mechanical systems, and silicon carbide products for automotive, medical, industrial, communication, and consumer sectors in the Europe, the United States, Asia, and internationally.

Very undervalued with reasonable growth potential.

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.3% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

AB

Abc on Global X Etfs Icav - Global X Silver Miners Ucits ETF ·

Many trends acting at the same time

Fair Value:€10068.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Texas Instruments ·

Engineered for Stability. Positioned for Growth.

Fair Value:US$314.4446.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

109 followersusers have followed this narrative

11 commentsusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

939 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative