Advertisement

- France

- /

- Retail REITs

- /

- ENXTPA:MERY

Should Mercialys’s (ENXTPA:MERY) CEO Transition and Upgraded Earnings Outlook Prompt Investor Reassessment?

Simply Wall St

Reviewed by Sasha Jovanovic

- Mercialys announced that Deputy CEO Elizabeth Blaise will step down from her position effective December 31, 2025, following over a decade with the company, and outlined the accompanying compensation terms and a 12-month non-compete agreement pending shareholder approval.

- Alongside this leadership transition, the Board reaffirmed raised full-year earnings guidance, signaling confidence in the existing management team and a strong operational outlook.

- We'll explore how Mercialys's upgraded earnings guidance amid its executive change shapes the company's forward-looking investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Mercialys Investment Narrative Recap

To be a shareholder in Mercialys, you need to believe in the durability of French retail real estate, especially the company's focus on urban shopping centers and its ability to maintain strong occupancy and rental growth despite e-commerce pressures. The recent announcement of Deputy CEO Elizabeth Blaise’s planned departure does not appear to materially impact the biggest short-term catalyst, successful retenanting and asset repositioning, or the most pressing risk of execution delays in large anchor units.

Among recent announcements, Mercialys reaffirmed its full-year 2025 earnings guidance, raising expected net recurrent earnings per share to €1.24–€1.27. This guidance, delivered alongside news of the executive transition, aligns with the short-term catalyst: management’s confidence in operational execution and revenue stabilization during a period of leadership change.

In contrast, the company’s current exposure to large anchor unit retenanting still represents a risk investors should be mindful of, as ...

Read the full narrative on Mercialys (it's free!)

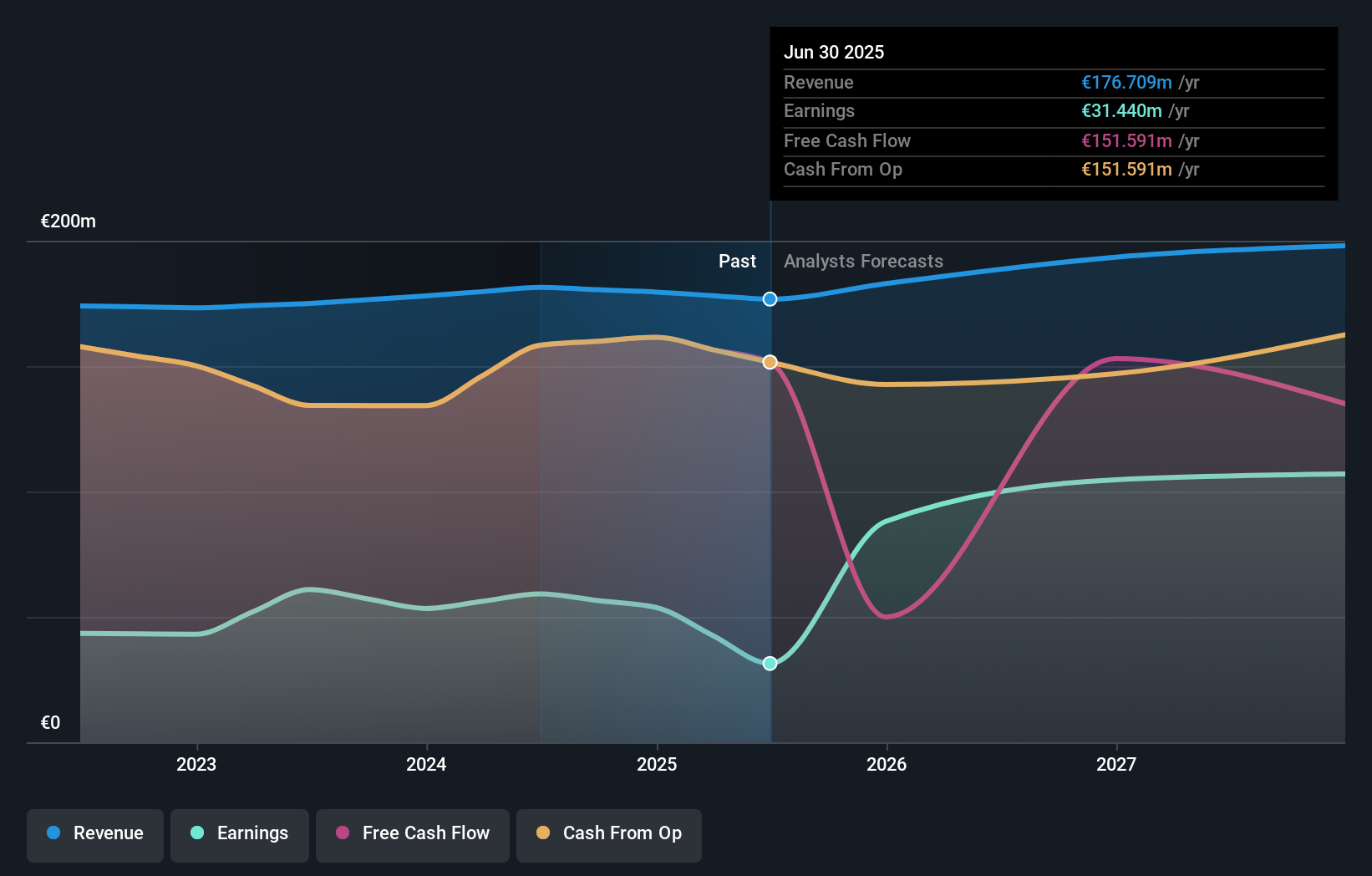

Mercialys' narrative projects €206.6 million revenue and €134.6 million earnings by 2028. This requires 5.4% yearly revenue growth and a €103.2 million increase in earnings from €31.4 million today.

Uncover how Mercialys' forecasts yield a €13.20 fair value, a 24% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members’ fair value estimates for Mercialys range from €13.20 to €15.94 across two submitted forecasts. While many focus on potential for earnings growth, ongoing execution risks tied to retenanting major anchor spaces may influence the strength and timing of any recovery. Explore other viewpoints to understand how these risks shape market sentiment.

Explore 2 other fair value estimates on Mercialys - why the stock might be worth just €13.20!

Build Your Own Mercialys Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Mercialys research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

- Our free Mercialys research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Mercialys' overall financial health at a glance.

No Opportunity In Mercialys?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:MERY

Good value average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets