Advertisement

Poxel S.A. (EPA:POXEL) Analysts Just Trimmed Their Revenue Forecasts By 28%

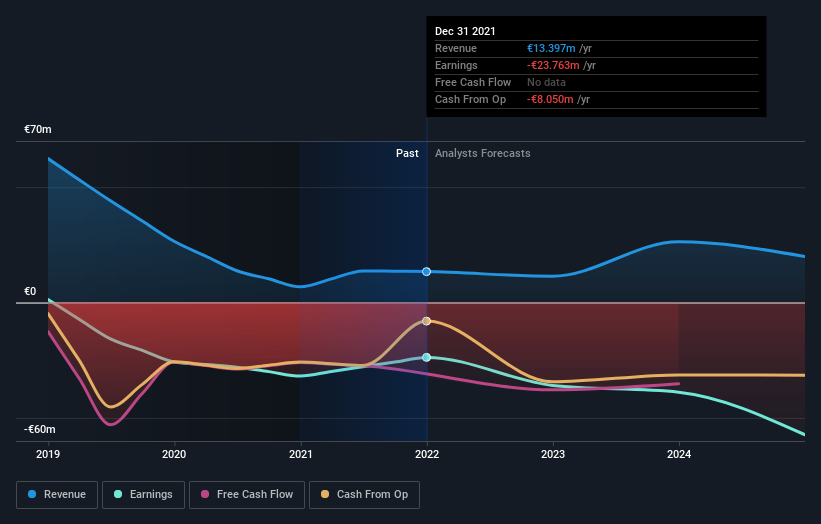

The analysts covering Poxel S.A. (EPA:POXEL) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

Following the downgrade, the consensus from three analysts covering Poxel is for revenues of €11m in 2022, implying a not inconsiderable 15% decline in sales compared to the last 12 months. Losses are supposed to balloon 52% to €1.26 per share. However, before this estimates update, the consensus had been expecting revenues of €16m and €1.21 per share in losses. Ergo, there's been a clear change in sentiment, with the analysts administering a notable cut to this year's revenue estimates, while at the same time increasing their loss per share forecasts.

Check out our latest analysis for Poxel

The consensus price target fell 16% to €13.43, implicitly signalling that lower earnings per share are a leading indicator for Poxel's valuation. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Poxel analyst has a price target of €21.00 per share, while the most pessimistic values it at €4.50. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how think this business will perform. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 15% by the end of 2022. This indicates a significant reduction from annual growth of 1.3% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 24% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Poxel is expected to lag the wider industry.

The Bottom Line

The most important thing to note from this downgrade is that the consensus increased its forecast losses this year, suggesting all may not be well at Poxel. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. The consensus price target fell measurably, with analysts seemingly not reassured by recent business developments, leading to a lower estimate of Poxel's future valuation. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of Poxel going forwards.

So things certainly aren't looking great, and you should also know that we've spotted some potential warning signs with Poxel, including a short cash runway. Learn more, and discover the 3 other warning signs we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:POXEL

Poxel

A clinical-stage biopharmaceutical company, develops novel treatments for metabolic diseases, type 2 diabetes, and liver diseases.

Medium-low with weak fundamentals.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor