Advertisement

Danone (ENXTPA:BN): Assessing Valuation After a Recent 3% Share Price Pullback

Simply Wall St

Reviewed by Simply Wall St

Danone (ENXTPA:BN) has quietly slipped about 3 % over the past month, even as its year to date gain sits near 17 %, prompting a fresh look at whether the current pullback offers value.

See our latest analysis for Danone.

That recent 3 % slide caps a softer 30 day share price return of around minus 3 %, but it comes after a solid year to date share price gain and strong multi year total shareholder returns. This suggests momentum is pausing rather than breaking.

If Danone’s quieter pullback has you thinking about where else capital might compound steadily, it might be worth scanning healthcare stocks for other resilient, demand driven names.

With earnings still growing, an intrinsic value estimate suggesting a sizable discount, and the share price hovering just below analyst targets, is Danone quietly offering upside potential, or is the market already baking in the next leg of growth?

Most Popular Narrative Narrative: 4.3% Undervalued

With Danone last closing at €75.66 against a narrative fair value of €79.02, the current pullback still sits below that implied mark. This frames the backdrop for how growth and margins are expected to evolve.

Strategic investments and recent acquisitions (Kate Farms, The Akkermansia Company) strengthen Danone's leadership in plant-based, gut health, and medical nutrition, reinforcing differentiation and supporting both premiumization (higher revenue per unit sold) and improved long-term margin potential.

Want to see what powers that premium nutrition bet? The narrative leans on steadily rising revenues, fatter margins, and a future earnings multiple that might surprise you.

Result: Fair Value of €79.02 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, lingering execution issues in North America and currency volatility across key markets could quickly challenge today’s steady growth and margin assumptions.

Find out about the key risks to this Danone narrative.

Another View: Multiples Paint a Richer Picture

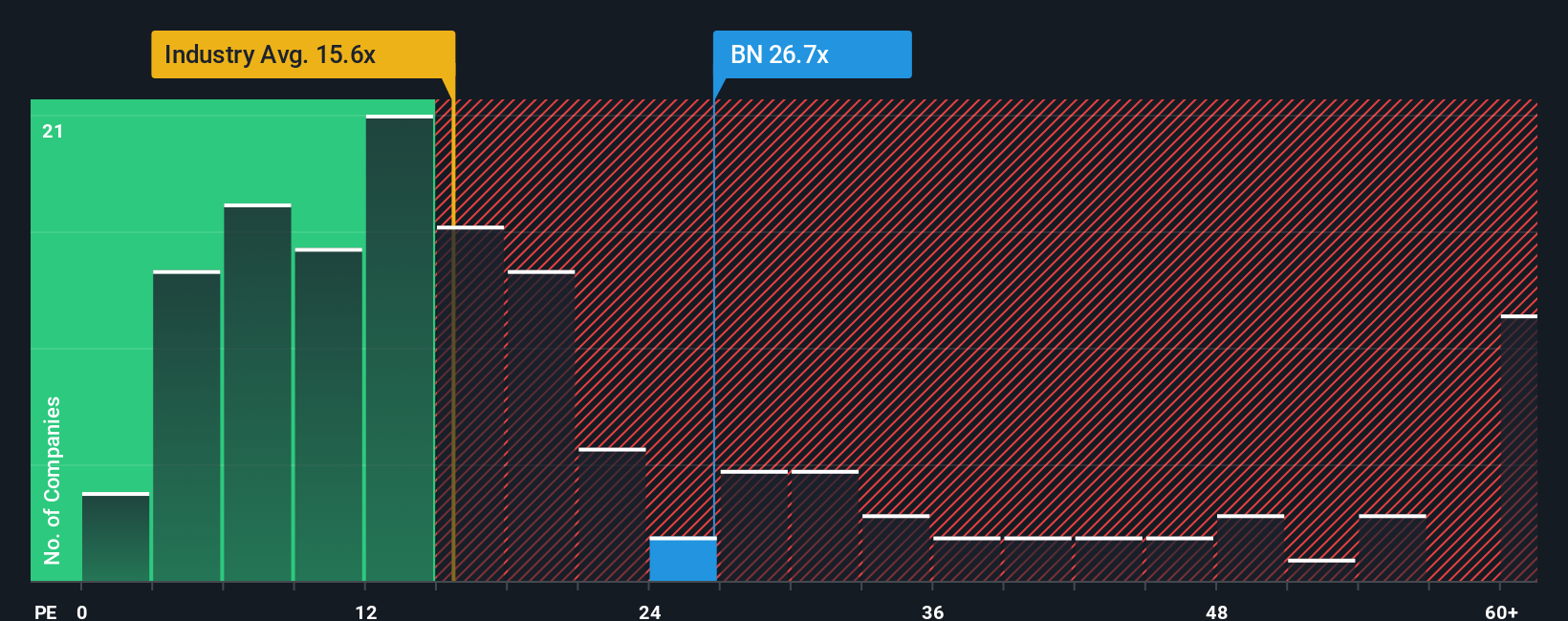

Set against that 4.3 % narrative discount, Danone’s price to earnings ratio of 26.6 times looks demanding versus the European food sector at 15.3 times and a fair ratio of 24.6 times, hinting at limited margin for error if growth or margins wobble.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Danone Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a personalized view in just minutes using Do it your way.

A great starting point for your Danone research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next opportunity by scanning targeted stock lists on Simply Wall Street, built to surface ideas you might otherwise miss.

- Capture potential mispricings early by running your own checks across these 906 undervalued stocks based on cash flows, where valuations lean in your favor.

- Ride structural shifts in technology by zeroing in on these 27 AI penny stocks positioned to benefit from accelerating AI adoption.

- Strengthen your income stream by reviewing these 15 dividend stocks with yields > 3% that aim to balance yield with sustainability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:BN

Danone

Operates in the food and beverage industry in Europe, Ukraine, North America, China, North Asia, the Oceania, Latin America, rest of Asia, Africa, Turkey, the Middle East, and the Commonwealth of Independent States.

Established dividend payer with proven track record.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4040.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6088.8% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

21 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative