- France

- /

- Energy Services

- /

- ENXTPA:VIRI

Increases to CGG's (EPA:CGG) CEO Compensation Might Cool off for now

Key Insights

- CGG will host its Annual General Meeting on 15th of May

- Salary of US$751.2k is part of CEO Sophie Zurquiyah-Rousset's total remuneration

- Total compensation is 113% above industry average

- CGG's three-year loss to shareholders was 47% while its EPS grew by 114% over the past three years

Shareholders of CGG (EPA:CGG) will have been dismayed by the negative share price return over the last three years. Despite positive EPS growth in the past few years, the share price hasn't tracked the fundamental performance of the company. Shareholders may want to question the board on the future direction of the company at the upcoming AGM on 15th of May. Voting on resolutions such as executive remuneration and other matters could also be a way to influence management. We think shareholders might be reluctant to increase compensation for the CEO at the moment, according to our analysis below.

View our latest analysis for CGG

Comparing CGG's CEO Compensation With The Industry

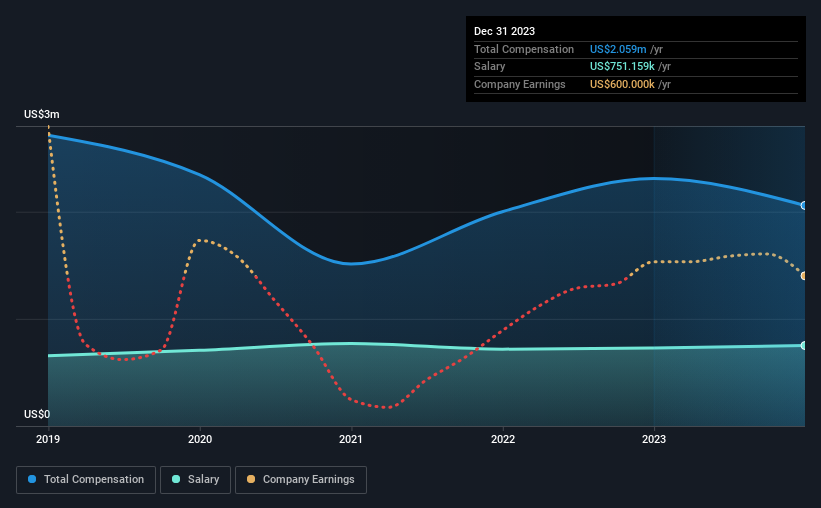

According to our data, CGG has a market capitalization of €326m, and paid its CEO total annual compensation worth US$2.1m over the year to December 2023. Notably, that's a decrease of 11% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at US$751k.

On examining similar-sized companies in the France Energy Services industry with market capitalizations between €185m and €742m, we discovered that the median CEO total compensation of that group was US$968k. Hence, we can conclude that Sophie Zurquiyah-Rousset is remunerated higher than the industry median. Moreover, Sophie Zurquiyah-Rousset also holds €140k worth of CGG stock directly under their own name.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$751k | US$729k | 36% |

| Other | US$1.3m | US$1.6m | 64% |

| Total Compensation | US$2.1m | US$2.3m | 100% |

On an industry level, roughly 61% of total compensation represents salary and 39% is other remuneration. In CGG's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

CGG's Growth

CGG has seen its earnings per share (EPS) increase by 114% a year over the past three years. In the last year, its revenue is up 16%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has CGG Been A Good Investment?

The return of -47% over three years would not have pleased CGG shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

In Summary...

The fact that shareholders are sitting on a loss on the value of their shares in the past few years is certainly disconcerting. The fact that the stock price hasn't grown along with earnings may indicate that other issues may be affecting that stock. Shareholders would be keen to know what's holding the stock back when earnings have grown. At the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 3 warning signs for CGG (1 is a bit unpleasant!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you're looking to trade Viridien Société anonyme, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:VIRI

Viridien Société anonyme

Provides data, products, services, and solutions in Earth science, data science, sensing, and monitoring in North America, Latin America, the Central and South Americas, Europe, Africa, the Middle East, and the Asia Pacific.

Good value with proven track record.

Similar Companies

Market Insights

Community Narratives