3 Stocks Priced Below Estimated Value That Could Enhance Your Portfolio

Reviewed by Simply Wall St

In a week marked by volatility, global markets have been influenced by significant developments, including the European Central Bank's rate cuts and competitive pressures in the AI sector. As investors navigate these turbulent waters, identifying stocks that are priced below their estimated value can be an effective strategy to potentially enhance portfolio returns.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Alltop Technology (TPEX:3526) | NT$264.50 | NT$527.77 | 49.9% |

| Sichuan Injet Electric (SZSE:300820) | CN¥50.58 | CN¥100.70 | 49.8% |

| Gaming Realms (AIM:GMR) | £0.358 | £0.71 | 49.7% |

| GlobalData (AIM:DATA) | £1.78 | £3.55 | 49.9% |

| Zhaojin Mining Industry (SEHK:1818) | HK$12.14 | HK$24.15 | 49.7% |

| Bufab (OM:BUFAB) | SEK467.40 | SEK928.96 | 49.7% |

| GemPharmatech (SHSE:688046) | CN¥13.06 | CN¥25.94 | 49.7% |

| South32 (ASX:S32) | A$3.31 | A$6.70 | 50.6% |

| Prodways Group (ENXTPA:PWG) | €0.576 | €1.15 | 49.8% |

| Gold Royalty (NYSEAM:GROY) | US$1.32 | US$2.63 | 49.9% |

Let's explore several standout options from the results in the screener.

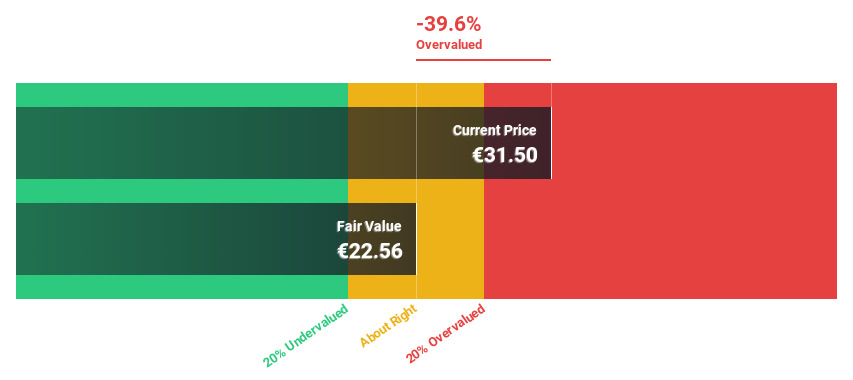

Kaufman & Broad (ENXTPA:KOF)

Overview: Kaufman & Broad S.A. is a property developer and builder based in France with a market capitalization of €688.48 million.

Operations: Kaufman & Broad S.A. generates revenue through its operations as a property developer and builder in France.

Estimated Discount To Fair Value: 19.5%

Kaufman & Broad appears undervalued, trading at €33.2 below its estimated fair value of €41.23, though not by a significant margin. Despite a decline in sales to €1.08 billion and net income to €44.97 million for 2024, earnings are forecasted to grow at 13.63% annually, outpacing the French market's 12.5%. However, its dividend yield of 7.23% is not well covered by earnings, posing sustainability concerns.

- The growth report we've compiled suggests that Kaufman & Broad's future prospects could be on the up.

- Click here to discover the nuances of Kaufman & Broad with our detailed financial health report.

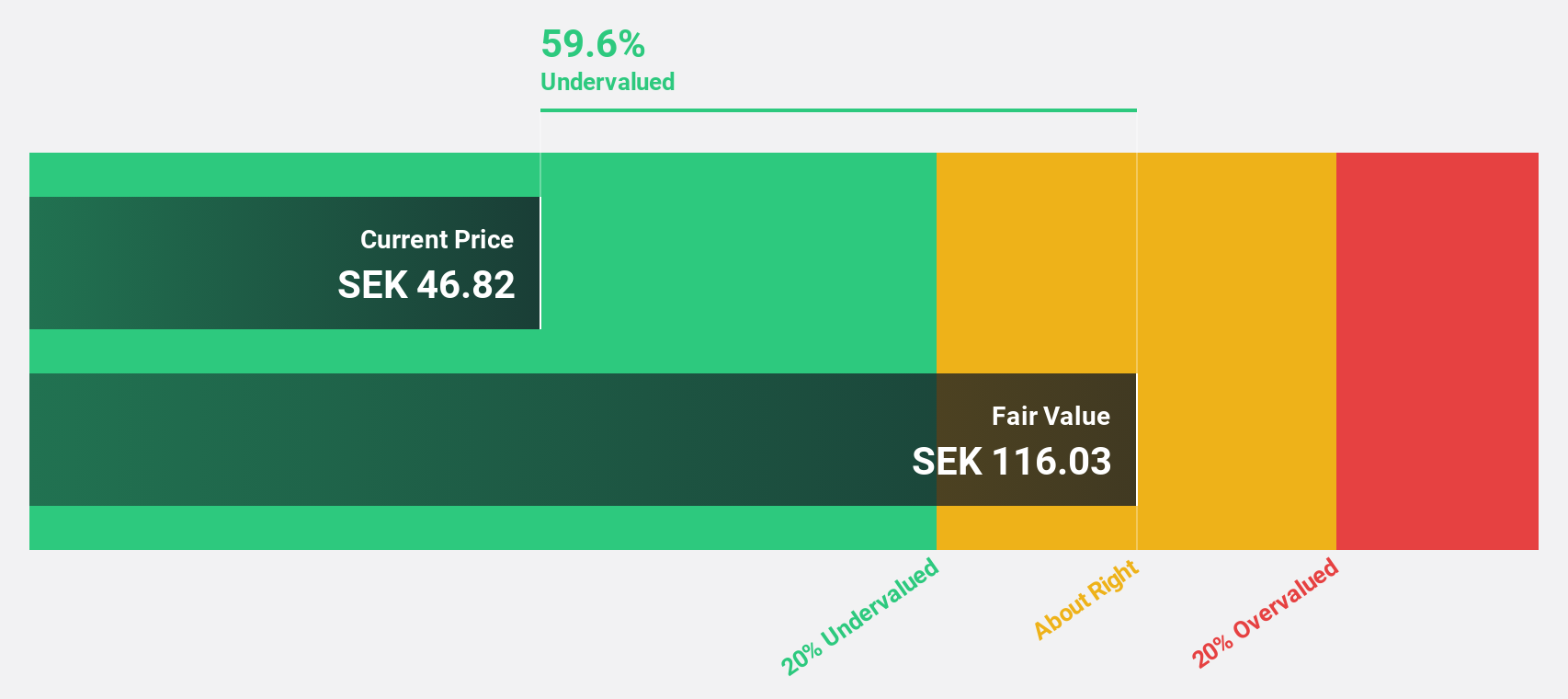

Elekta (OM:EKTA B)

Overview: Elekta AB (publ) is a medical technology company that provides clinical solutions for treating cancer and brain disorders globally, with a market cap of approximately SEK251.22 billion.

Operations: Elekta's revenue is derived from three primary regions: APAC with SEK6.08 billion, Americas contributing SEK5.41 billion, and Europe, Middle East and Africa (EMEA) generating SEK6.23 billion.

Estimated Discount To Fair Value: 48.8%

Elekta is trading at SEK65.75, significantly below its estimated fair value of SEK128.37, suggesting it may be undervalued based on cash flows. Despite a drop in sales to SEK 8.17 billion and net income to SEK 282 million for the first half of 2024, earnings are projected to grow at over 21% annually, surpassing the Swedish market's growth rate. However, its dividend yield of 1.83% isn't well covered by earnings and it carries high debt levels.

- Our growth report here indicates Elekta may be poised for an improving outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Elekta.

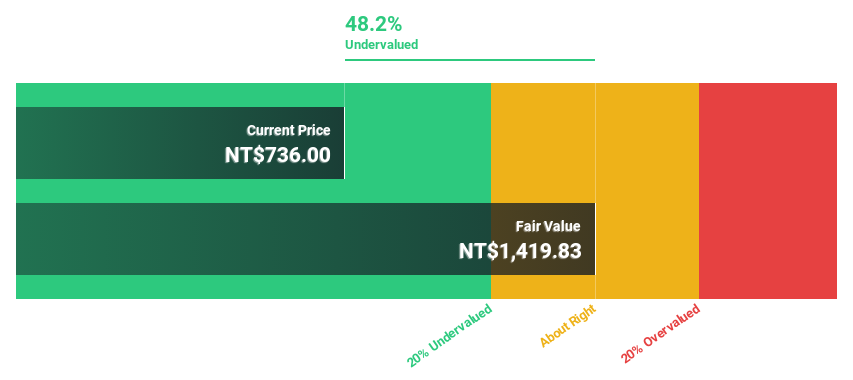

Bora Pharmaceuticals (TWSE:6472)

Overview: Bora Pharmaceuticals Co., LTD. is engaged in the research, development, manufacturing, distribution, and sales of pharmaceuticals on a global scale with a market cap of NT$83.09 billion.

Operations: The company's revenue is primarily derived from its Sales Operations Department at NT$14.08 billion and CDMO Operations Department at NT$6.33 billion.

Estimated Discount To Fair Value: 41.3%

Bora Pharmaceuticals is trading at NT$833, significantly below its fair value estimate of NT$1,419.83, indicating potential undervaluation based on cash flows. Recent earnings showed strong growth with sales reaching TWD 5.61 billion and net income TWD 1.45 billion for Q3 2024. However, despite a forecasted annual revenue growth of 22.5%, the company's debt is not well covered by operating cash flow, presenting a financial risk to consider.

- The analysis detailed in our Bora Pharmaceuticals growth report hints at robust future financial performance.

- Click to explore a detailed breakdown of our findings in Bora Pharmaceuticals' balance sheet health report.

Key Takeaways

- Discover the full array of 919 Undervalued Stocks Based On Cash Flows right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bora Pharmaceuticals might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:6472

Bora Pharmaceuticals

Researches and develops, manufactures, distributes, and sells pharmaceuticals worldwide.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives