Advertisement

Kering SA Beat Analyst Estimates: See What The Consensus Is Forecasting For This Year

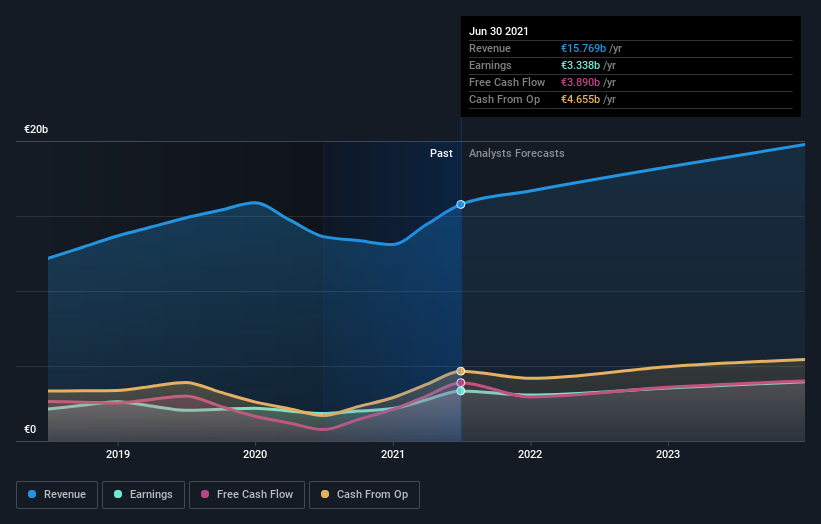

Kering SA (EPA:KER) just released its latest interim results and things are looking bullish. Kering beat earnings, with revenues hitting €8.0b, ahead of expectations, and statutory earnings per share outperforming analyst reckonings by a solid 14%. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

View our latest analysis for Kering

Taking into account the latest results, the current consensus from Kering's 24 analysts is for revenues of €16.7b in 2021, which would reflect a satisfactory 5.7% increase on its sales over the past 12 months. Statutory earnings per share are forecast to reduce 7.9% to €24.61 in the same period. In the lead-up to this report, the analysts had been modelling revenues of €16.4b and earnings per share (EPS) of €24.00 in 2021. So the consensus seems to have become somewhat more optimistic on Kering's earnings potential following these results.

The consensus price target was unchanged at €796, implying that the improved earnings outlook is not expected to have a long term impact on value creation for shareholders. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on Kering, with the most bullish analyst valuing it at €950 and the most bearish at €455 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The analysts are definitely expecting Kering's growth to accelerate, with the forecast 12% annualised growth to the end of 2021 ranking favourably alongside historical growth of 5.6% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 8.7% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Kering is expected to grow much faster than its industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Kering following these results. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Kering analysts - going out to 2023, and you can see them free on our platform here.

However, before you get too enthused, we've discovered 1 warning sign for Kering that you should be aware of.

If you decide to trade Kering, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kering might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTPA:KER

Kering

Manages the development of a collection of renowned houses in fashion, leather goods, and jewelry in the Asia Pacific, Western Europe, North America, Japan, and internationally.

Average dividend payer with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.9% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.9% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|64.1% undervalued

ME

Community Contributor