Advertisement

- France

- /

- Consumer Durables

- /

- ENXTPA:ALAST

AST Groupe (EPA:ASP) Is Looking To Continue Growing Its Returns On Capital

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So on that note, AST Groupe (EPA:ASP) looks quite promising in regards to its trends of return on capital.

What is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for AST Groupe, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

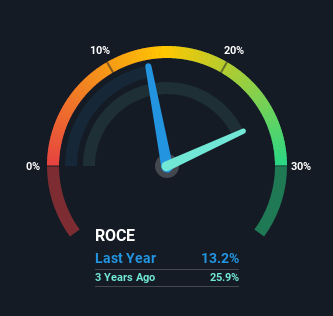

0.13 = €9.0m ÷ (€150m - €82m) (Based on the trailing twelve months to December 2020).

So, AST Groupe has an ROCE of 13%. In absolute terms, that's a satisfactory return, but compared to the Consumer Durables industry average of 10% it's much better.

See our latest analysis for AST Groupe

In the above chart we have measured AST Groupe's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering AST Groupe here for free.

What Can We Tell From AST Groupe's ROCE Trend?

Investors would be pleased with what's happening at AST Groupe. Over the last five years, returns on capital employed have risen substantially to 13%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 94%. So we're very much inspired by what we're seeing at AST Groupe thanks to its ability to profitably reinvest capital.

On a side note, AST Groupe's current liabilities are still rather high at 55% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

The Bottom Line

In summary, it's great to see that AST Groupe can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. Since the stock has returned a staggering 146% to shareholders over the last five years, it looks like investors are recognizing these changes. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

One more thing, we've spotted 3 warning signs facing AST Groupe that you might find interesting.

While AST Groupe isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you decide to trade AST Groupe, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTPA:ALAST

Very low with weak fundamentals.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

18 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.0% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8142.8% undervalued

41 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

MH

mhbb on Mastersystem Infotama ·

Mastersystem Infotama will achieve 18.9% revenue growth as fair value hits IDR1,650

Fair Value:Rp1.63k13.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Procter & Gamble ·

Insiders Sell, Investors Watch: What’s Going On at PG?

Fair Value:US$1506.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CW

Cwburton on Verano Holdings ·

Waiting for the Inevitable

Fair Value:CA$5.5278.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.6% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8684.3% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative