Advertisement

- France

- /

- Commercial Services

- /

- ENXTPA:SPIE

SPIE SA (EPA:SPIE) Released Earnings Last Week And Analysts Lifted Their Price Target To €49.15

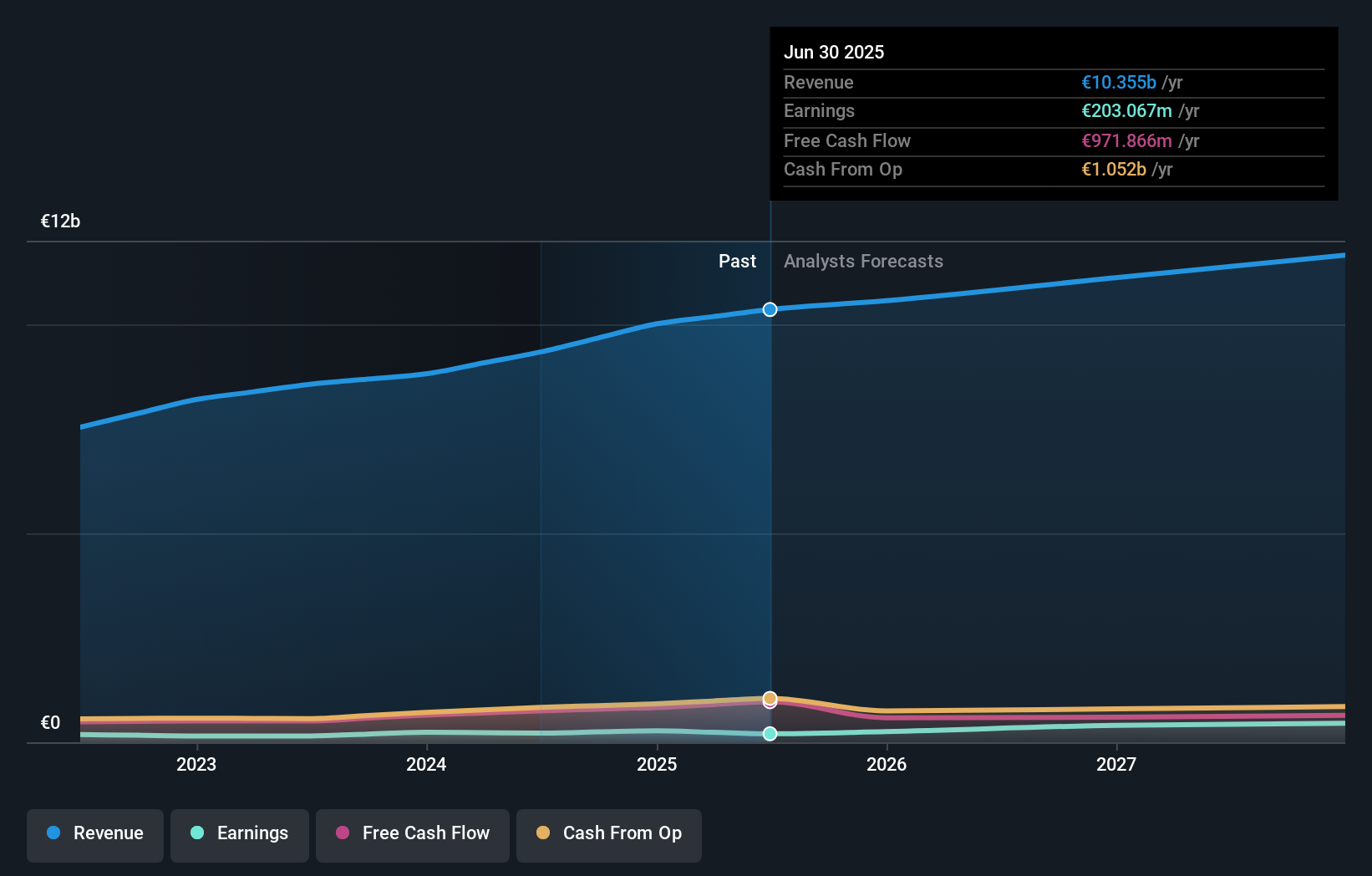

Investors in SPIE SA (EPA:SPIE) had a good week, as its shares rose 2.6% to close at €50.10 following the release of its half-year results. It was a credible result overall, with revenues of €5.0b and statutory earnings per share of €1.63 both in line with analyst estimates, showing that SPIE is executing in line with expectations. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

After the latest results, the nine analysts covering SPIE are now predicting revenues of €10.6b in 2025. If met, this would reflect a reasonable 2.0% improvement in revenue compared to the last 12 months. Before this earnings report, the analysts had been forecasting revenues of €10.6b and earnings per share (EPS) of €2.01 in 2025. Overall, while the analysts have reconfirmed their revenue estimates, the consensus now no longer provides an EPS estimate. This implies that the market believes revenue is more important after these latest results.

See our latest analysis for SPIE

Additionally, the consensus price target for SPIE rose 7.7% to €49.15, showing a clear increase in optimism from the the analysts involved. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on SPIE, with the most bullish analyst valuing it at €60.00 and the most bearish at €33.00 per share. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the SPIE's past performance and to peers in the same industry. We would highlight that SPIE's revenue growth is expected to slow, with the forecast 4.1% annualised growth rate until the end of 2025 being well below the historical 9.5% p.a. growth over the last five years. Compare this to the 16 other companies in this industry with analyst coverage, which are forecast to grow their revenue at 4.2% per year. Factoring in the forecast slowdown in growth, it looks like SPIE is forecast to grow at about the same rate as the wider industry.

The Bottom Line

The most important thing to take away is that the analysts reconfirmed their revenue estimates for next year, suggesting that the business is performing in line with expectations. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

We have estimates for SPIE from its nine analysts out to 2027, and you can see them free on our platform here.

Before you take the next step you should know about the 3 warning signs for SPIE that we have uncovered.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTPA:SPIE

SPIE

Provides multi-technical services in the areas of energy and communications in France, Germany, the Netherlands, and internationally.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|30.4% undervalued

MA

Community Contributor

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor