Advertisement

Does The Data Make Manitou BF SA (EPA:MTU) An Attractive Investment?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

As an investor, I look for investments which does not compromise one fundamental factor for another. By this I mean, I look at stocks holistically, from their financial health to their future outlook. In the case of Manitou BF SA (EPA:MTU), it is a financially-sound company with a an impressive track record of performance, trading at a discount. Below is a brief commentary on these key aspects. For those interested in digger a bit deeper into my commentary, take a look at the report on Manitou BF here.

Solid track record and good value

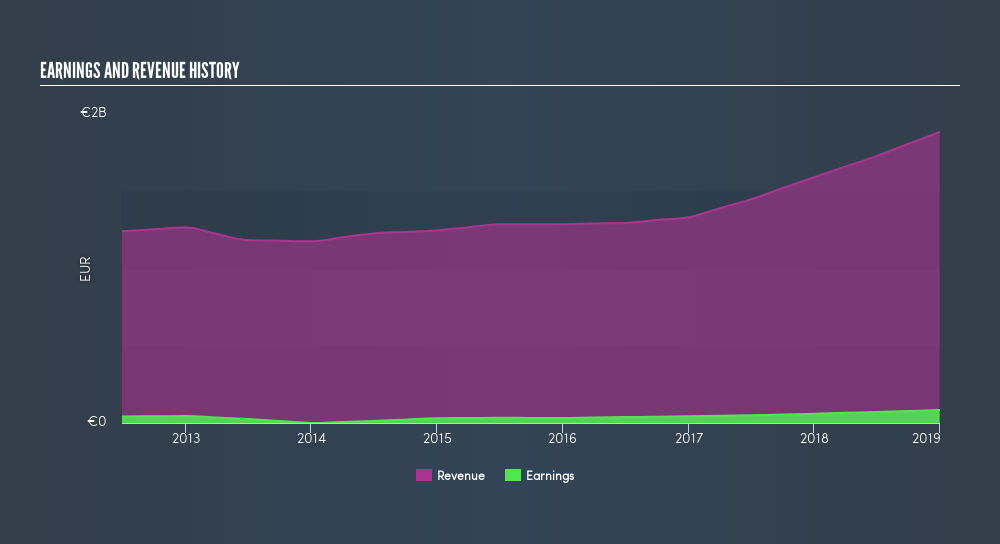

Over the past year, MTU has grown its earnings by 40%, with its most recent figure exceeding its annual average over the past five years. Not only did MTU outperformed its past performance, its growth also exceeded the Machinery industry expansion, which generated a 1.6% earnings growth. This is an notable feat for the company. MTU is financially robust, with ample cash on hand and short-term investments to meet upcoming liabilities. This indicates that MTU has sufficient cash flows and proper cash management in place, which is a crucial insight into the health of the company. MTU’s debt-to-equity ratio stands at 30%, which means its debt level is reasonable. This means that MTU’s capital structure strikes a good balance between low-cost debt funding and maintaining financial flexibility without overly restrictive terms of debt.

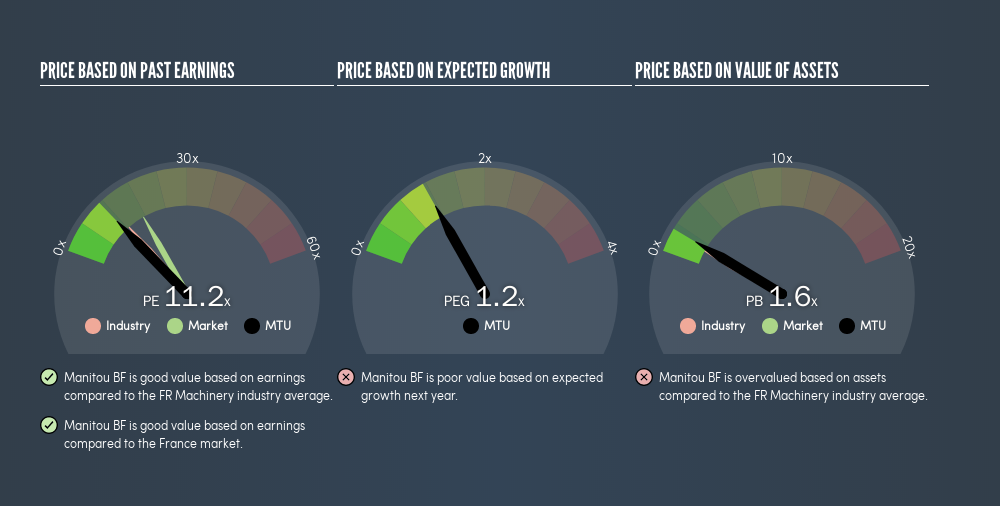

MTU is currently trading below its true value, which means the market is undervaluing the company's expected cash flow going forward. This mispricing gives investors the opportunity to buy into the stock at a cheap price compared to the value they will be receiving, should analysts' consensus forecast growth be correct. Compared to the rest of the machinery industry, MTU is also trading below its peers, relative to earnings generated. This further reaffirms that MTU is potentially undervalued.

Next Steps:

For Manitou BF, I've put together three relevant factors you should further examine:

- Future Outlook: What are well-informed industry analysts predicting for MTU’s future growth? Take a look at our free research report of analyst consensus for MTU’s outlook.

- Dividend Income vs Capital Gains: Does MTU return gains to shareholders through reinvesting in itself and growing earnings, or redistribute a decent portion of earnings as dividends? Our historical dividend yield visualization quickly tells you what your can expect from MTU as an investment.

- Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of MTU? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About ENXTPA:MTU

Manitou BF

Engages in the development, manufacture, and distribution of equipment and services in the France, Southern Europe, Northern Europe, the Americas, Asia, the Pacific, Africa, and the Middle East.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor