Advertisement

- France

- /

- Aerospace & Defense

- /

- ENXTPA:EXENS

Exosens (ENXTPA:EXENS) Valuation After Extending Theon Deal and Locking In Higher Night Vision Demand Through 2030

Simply Wall St

Reviewed by Simply Wall St

Exosens (ENXTPA:EXENS) just locked in a longer runway with Theon International by extending their image intensifier supply deal through 2030, turning future options into firm orders and backing ongoing capacity expansion.

See our latest analysis for Exosens.

The deal lands while Exosens trades around €48.9, after a powerful year to date share price return of 154.24 percent and a 1 year total shareholder return of 166.59 percent, suggesting momentum is still firmly building as investors reassess its growth and defense exposure.

If this contract has you thinking about where else demand driven growth could surprise, it might be worth exploring aerospace and defense stocks as a starting point for your next idea.

Yet with Exosens already up more than 150 percent this year and trading only slightly below its analyst target, the key question now is whether the extended Theon deal still leaves upside or if the market has fully priced in its growth.

Most Popular Narrative: 1.5% Undervalued

With the most followed narrative pointing to a fair value just above the latest €48.9 close, the focus shifts squarely to how far earnings can stretch.

Robust ongoing investment in R&D (over 7.6% of sales), with a pipeline of next-generation products (e.g. 5G-ready night vision) scheduled for launch, anchors Exosens' technology leadership, supports higher-margin product mixes, and provides pricing power, all positively impacting future gross and EBITDA margins.

Want to see how sustained double digit growth, rising profitability and a future earnings multiple come together in this valuation story? The key assumptions behind that fair value might surprise you. Discover which revenue trajectory, margin expansion and valuation reset underpin this seemingly modest discount.

Result: Fair Value of €49.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, supply chain bottlenecks in capacity expansion or prolonged margin drag from lower-margin acquisitions could quickly challenge this seemingly comfortable upside case.

Find out about the key risks to this Exosens narrative.

Another Angle on Valuation

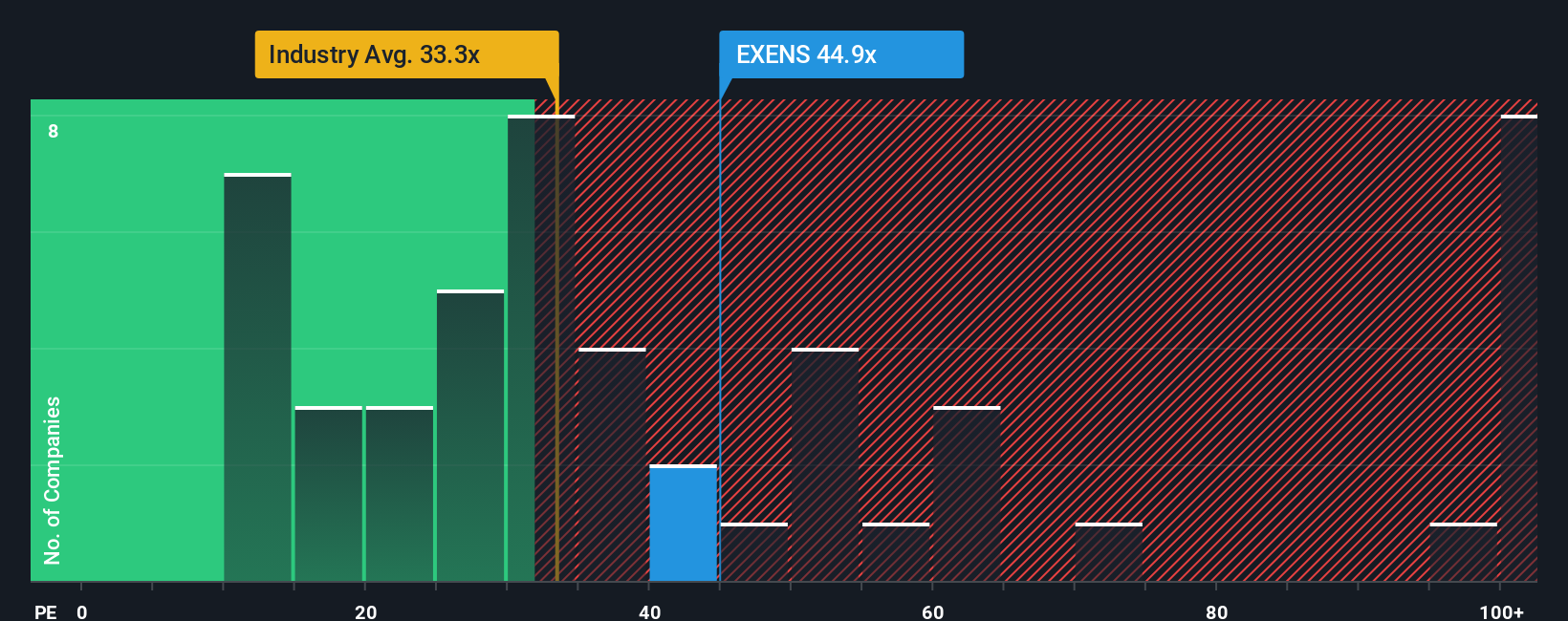

While our model suggests Exosens trades about 19.6 percent below fair value, the earnings multiple tells a different story. The shares are on 44.5 times earnings versus a 25 times fair ratio and 30.9 times for the wider European aerospace and defense group. Is upside already being borrowed from tomorrow’s growth?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Exosens Narrative

If you see the story differently or want to stress test the numbers yourself, you can build a complete view in just a few minutes: Do it your way.

A great starting point for your Exosens research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for your next investing move?

Do not stop with a single idea. Use the Simply Wall St Screener to uncover fresh opportunities that match your strategy before the market catches up.

- Capture early stage growth potential with these 3588 penny stocks with strong financials that already show stronger balance sheets and healthier fundamentals than typical speculative names.

- Position your portfolio for the next wave of intelligent automation by targeting these 27 AI penny stocks reshaping industries with scalable, data driven business models.

- Boost your income stream by focusing on these 15 dividend stocks with yields > 3% that combine solid yields with sustainable payout ratios and resilient cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Exosens might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ENXTPA:EXENS

Exosens

Engages in the development, manufacture, and sale of electro-optical technologies in the fields of amplification, and detection and imaging in France, rest of Europe, North America, Asia, Oceania, Africa, and internationally.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

OP

OpenHorizons on Channel Vas Investments ·

Growing between 25-50% for the next 3-5 years

Fair Value:R12.1161.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative