Advertisement

- Finland

- /

- Food and Staples Retail

- /

- HLSE:KESKOB

It Might Not Be A Great Idea To Buy Kesko Oyj (HEL:KESKOB) For Its Next Dividend

Kesko Oyj (HEL:KESKOB) stock is about to trade ex-dividend in 3 days. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is of consequence because whenever a stock is bought or sold, the trade takes at least two business day to settle. Therefore, if you purchase Kesko Oyj's shares on or after the 13th of January, you won't be eligible to receive the dividend, when it is paid on the 21st of January.

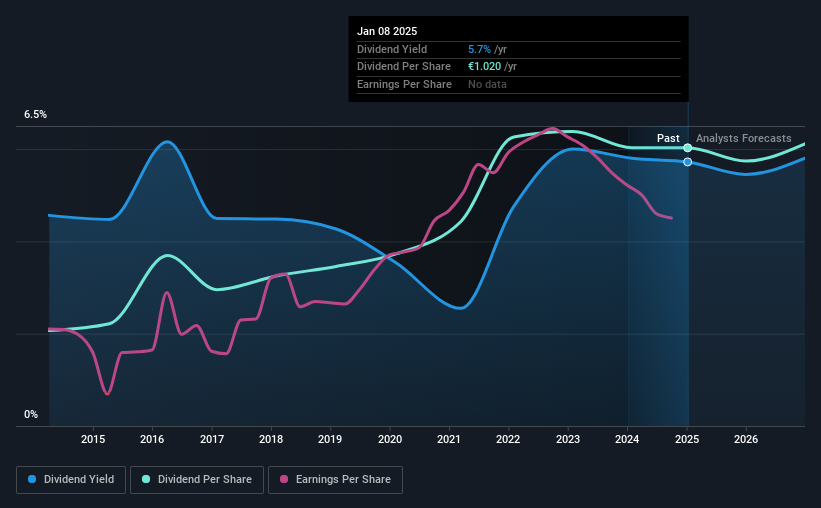

The company's next dividend payment will be €0.25 per share. Last year, in total, the company distributed €1.02 to shareholders. Calculating the last year's worth of payments shows that Kesko Oyj has a trailing yield of 5.7% on the current share price of €17.825. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to check whether the dividend payments are covered, and if earnings are growing.

Check out our latest analysis for Kesko Oyj

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Last year Kesko Oyj paid out 97% of its profits as dividends to shareholders, suggesting the dividend is not well covered by earnings. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Dividends consumed 70% of the company's free cash flow last year, which is within a normal range for most dividend-paying organisations.

It's good to see that while Kesko Oyj's dividends were not well covered by profits, at least they are affordable from a cash perspective. Still, if this were to happen repeatedly, we'd be concerned about whether the dividend is sustainable in a downturn.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. For this reason, we're glad to see Kesko Oyj's earnings per share have risen 14% per annum over the last five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Kesko Oyj has delivered 11% dividend growth per year on average over the past 10 years. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

Final Takeaway

Should investors buy Kesko Oyj for the upcoming dividend? Growing earnings per share and a normal cashflow payout ratio is an ok combination, but we're concerned that the company is paying out such a high percentage of its income as dividends. All things considered, we are not particularly enthused about Kesko Oyj from a dividend perspective.

If you want to look further into Kesko Oyj, it's worth knowing the risks this business faces. To help with this, we've discovered 1 warning sign for Kesko Oyj that you should be aware of before investing in their shares.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Kesko Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:KESKOB

Kesko Oyj

Engages in the chain operations in Finland, Sweden, Norway, Estonia, Latvia, Lithuania, Denmark, and Poland.

Adequate balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|37.8% undervalued

IN

Community Contributor

CSL is undervalued in High Tax Scenario

Fair Value AU$263.33|10.2% undervalued

RA

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor