Hiab Oyj's (HEL:HIAB) 26% Share Price Surge Not Quite Adding Up

Hiab Oyj (HEL:HIAB) shareholders are no doubt pleased to see that the share price has bounced 26% in the last month, although it is still struggling to make up recently lost ground. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 41% in the last twelve months.

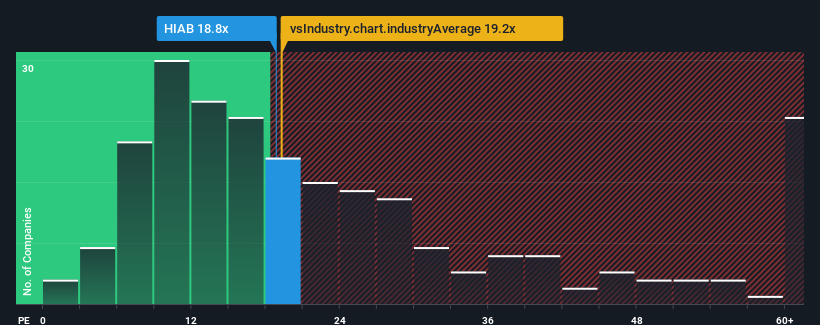

Even after such a large jump in price, there still wouldn't be many who think Hiab Oyj's price-to-earnings (or "P/E") ratio of 18.8x is worth a mention when the median P/E in Finland is similar at about 20x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Our free stock report includes 1 warning sign investors should be aware of before investing in Hiab Oyj. Read for free now.There hasn't been much to differentiate Hiab Oyj's and the market's retreating earnings lately. The P/E is probably moderate because investors think the company's earnings trend will continue to follow the rest of the market. You'd much rather the company wasn't bleeding earnings if you still believe in the business. In saying that, existing shareholders probably aren't too pessimistic about the share price if the company's earnings continue tracking the market.

View our latest analysis for Hiab Oyj

What Are Growth Metrics Telling Us About The P/E?

Hiab Oyj's P/E ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the market.

Retrospectively, the last year delivered a frustrating 6.1% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 38% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Shifting to the future, estimates from the four analysts covering the company suggest earnings should grow by 7.5% per year over the next three years. Meanwhile, the rest of the market is forecast to expand by 16% per annum, which is noticeably more attractive.

In light of this, it's curious that Hiab Oyj's P/E sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of earnings growth is likely to weigh down the shares eventually.

The Final Word

Its shares have lifted substantially and now Hiab Oyj's P/E is also back up to the market median. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Hiab Oyj's analyst forecasts revealed that its inferior earnings outlook isn't impacting its P/E as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the moderate P/E lower. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

We don't want to rain on the parade too much, but we did also find 1 warning sign for Hiab Oyj that you need to be mindful of.

You might be able to find a better investment than Hiab Oyj. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Hiab Oyj might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:HIAB

Hiab Oyj

Provides smart and on road load-handling solutions and services in Finland.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Community Narratives