Advertisement

How the Recent Share Price Surge Shapes the 2025 Outlook for Nordea Bank

Simply Wall St

Reviewed by Bailey Pemberton

Thinking about what to do with your shares, or possibly adding Nordea Bank Abp to your portfolio? You’re not alone. The stock has been turning heads lately with a steady climb that’s hard to ignore. In just the past week, Nordea edged up by 0.1%. Looking at a broader view, that’s a 4.4% rise over the past month, a 29.7% jump year-to-date, and a remarkable 44.7% increase over the last year. If you had invested five years ago, you’d be sitting on a gain of nearly 198%. Those are not numbers you see every day in the banking sector and they speak to shifting perceptions of risk and opportunity as European banks navigate changing economic winds.

What’s driving this upward run? Several sector-wide movements have played a role, including renewed optimism around European financial stocks and improved sentiment as regulatory tailwinds ease some previous concerns. Nordea’s performance reflects more than momentum, though. When you dig into the numbers, the company boasts a value score of 4, which indicates it checks the “undervalued” box in four out of six recognized valuation criteria. Not bad for a major Nordic bank with decades of industry experience and market leadership.

With that background, how exactly is Nordea valued right now, and what do those four “undervalued” checks tell us? Let’s examine the main valuation methods before exploring a more refined perspective on what the stock is really worth.

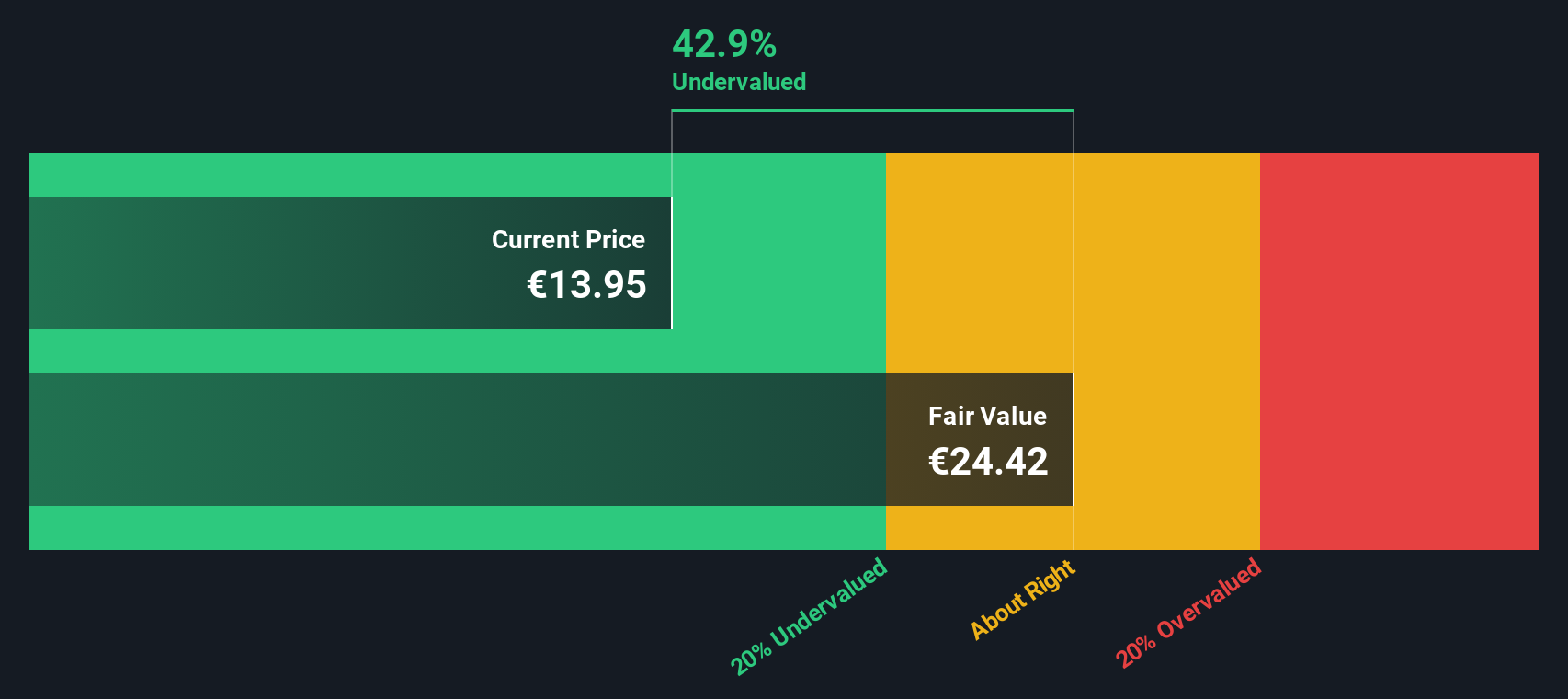

Approach 1: Nordea Bank Abp Excess Returns Analysis

The Excess Returns valuation model focuses on how effectively a company generates profits above its cost of equity. In other words, it assesses whether Nordea Bank Abp is earning more on its invested capital than it costs to obtain that capital, which is a key factor for long-term shareholder value.

For Nordea Bank Abp, the latest numbers look compelling. The current Book Value stands at €8.78 per share, while forward-looking analyst estimates peg the Stable EPS at €1.43 per share, based on data from 14 analysts. The company’s Cost of Equity is €0.68 per share, and the projected Excess Return per share is €0.74. With an average Return on Equity of 14.46%, Nordea ranks strongly compared to both its regional and sector peers. Looking further out, the Stable Book Value is expected to reach €9.86 per share according to weighted estimates from three analysts.

Based on this approach, the intrinsic value for Nordea shares is estimated significantly above the current market price. The Excess Returns valuation suggests the stock is trading at a 43.1% discount to its intrinsic worth, indicating considerable undervaluation in the current market.

Result: UNDERVALUED

Our Excess Returns analysis suggests Nordea Bank Abp is undervalued by 43.1%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

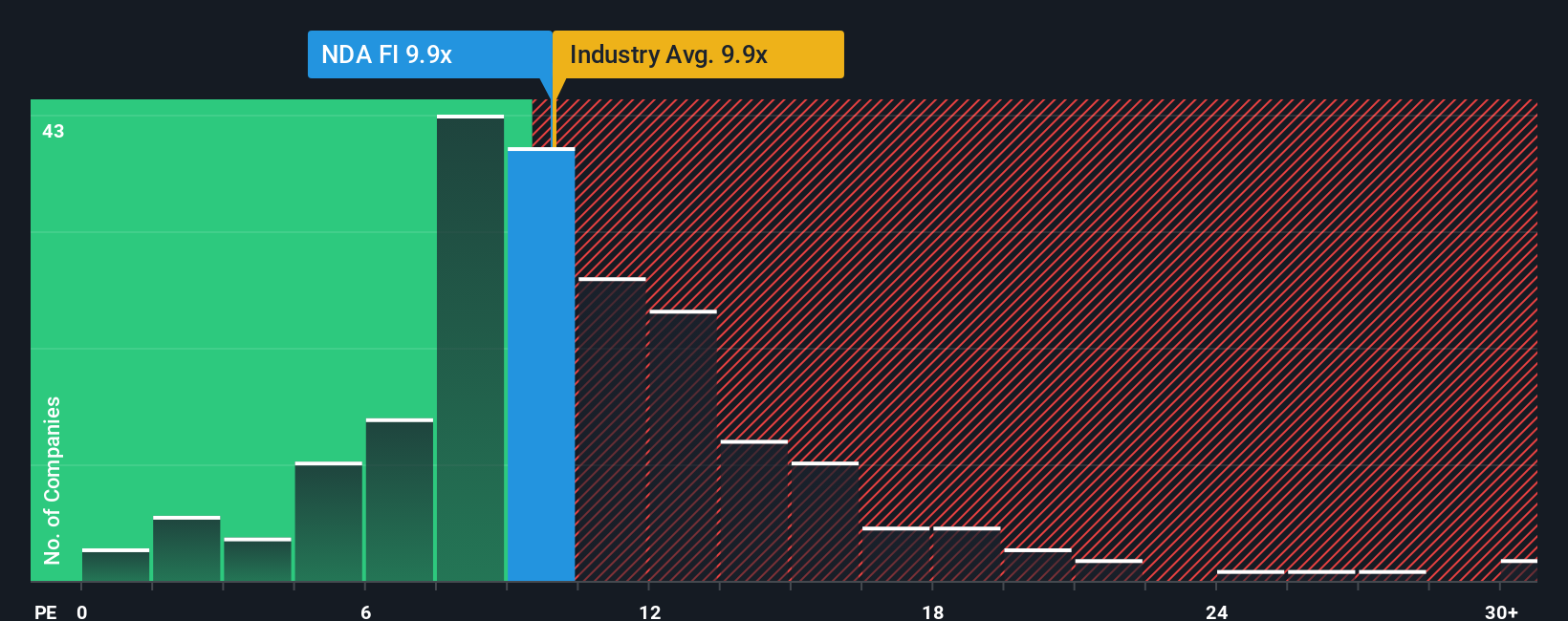

Approach 2: Nordea Bank Abp Price vs Earnings

For profitable companies like Nordea Bank Abp, the Price-to-Earnings (PE) ratio remains one of the most trusted valuation metrics. It helps investors gauge how much they are paying for each euro of earnings, making it especially useful when a company has stable profits. Generally, higher growth expectations or lower perceived risk justify a higher PE ratio. In contrast, slower growth or elevated risks suggest a lower fair multiple.

Currently, Nordea trades at a PE ratio of 9.88x. This is slightly below the industry average for banks, which stands at 10.33x, and is also lower than its typical peer group, which averages 11.76x. These comparisons suggest Nordea is valued conservatively relative to its sector. However, simply benchmarking against peers or the industry can present a limited view because it ignores company-specific factors such as unique growth prospects or risk profile.

That is where Simply Wall St’s “Fair Ratio” comes in. This proprietary metric weighs not only Nordea’s expected earnings growth and margins but also factors in its size, risk profile, and the realities of its sector. For Nordea, the Fair Ratio is calculated at 9.37x. Since this is very close to the actual PE ratio, it suggests the market is pricing Nordea’s earnings quite efficiently. Investors may not be getting a clear bargain, but nor are they overpaying based on the underlying fundamentals and outlook.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Nordea Bank Abp Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is a simple yet powerful tool that lets you connect your view on a company—its story, strengths, and risks—to a financial forecast, and ultimately to a fair value estimate. Unlike traditional models that focus purely on numbers, a Narrative helps you express the “why” behind your outlook, by combining assumptions about future revenue, earnings, and margins with your own perspective.

On Simply Wall St’s Community page, millions of investors use Narratives to make smarter buy and sell decisions. Narratives let you compare your fair value estimate to the current share price, making it clear whether your story says the stock is a good deal right now. Best of all, these Narratives are dynamic and update automatically as new information from news or earnings reports comes in, so your view stays relevant and up-to-date.

For example, some investors see Nordea Bank Abp’s digital transformation and stable Nordic market position driving future gains and set higher fair value targets. Others stay cautious due to margin compression or regulatory risks, leading to more conservative valuations. Narratives let you see and test these perspectives side by side as you decide your next move.

Do you think there's more to the story for Nordea Bank Abp? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nordea Bank Abp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About HLSE:NDA FI

Nordea Bank Abp

Offers banking products and services for individuals, families, and businesses in Sweden, Finland, Norway, Denmark, and internationally.

Good value with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.2% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|90.0% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.6% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|97.1% undervalued

AG

Community Contributor