Did Construcciones y Auxiliar de Ferrocarriles' (BME:CAF) Share Price Deserve to Gain 56%?

Stock pickers are generally looking for stocks that will outperform the broader market. And in our experience, buying the right stocks can give your wealth a significant boost. For example, long term Construcciones y Auxiliar de Ferrocarriles, S.A. (BME:CAF) shareholders have enjoyed a 56% share price rise over the last half decade, well in excess of the market decline of around 5.7% (not including dividends).

See our latest analysis for Construcciones y Auxiliar de Ferrocarriles

While Construcciones y Auxiliar de Ferrocarriles made a small profit, in the last year, we think that the market is probably more focussed on the top line growth at the moment. Generally speaking, we'd consider a stock like this alongside loss-making companies, simply because the quantum of the profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

For the last half decade, Construcciones y Auxiliar de Ferrocarriles can boast revenue growth at a rate of 18% per year. Even measured against other revenue-focussed companies, that's a good result. It's good to see that the stock has 9%, but not entirely surprising given revenue shows strong growth. If you think there could be more growth to come, now might be the time to take a close look at Construcciones y Auxiliar de Ferrocarriles. Of course, you'll have to research the business more fully to figure out if this is an attractive opportunity.

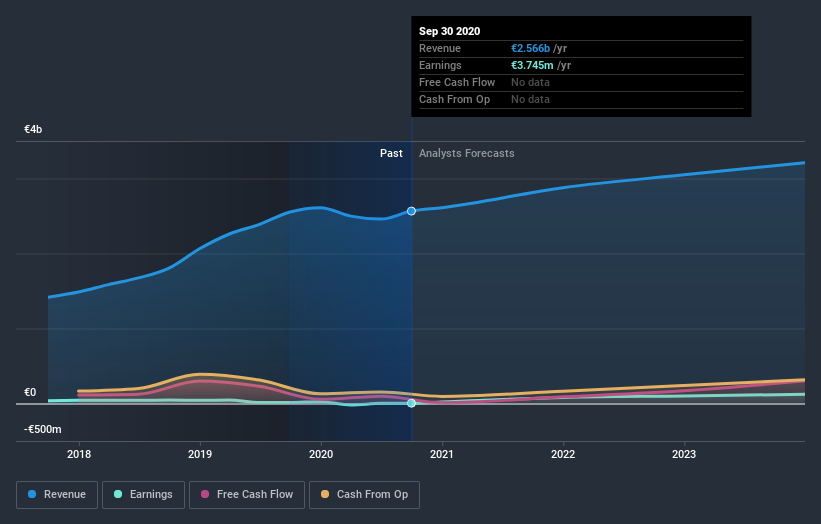

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

What About Dividends?

When looking at investment returns, it is important to consider the difference between total shareholder return (TSR) and share price return. The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. It's fair to say that the TSR gives a more complete picture for stocks that pay a dividend. In the case of Construcciones y Auxiliar de Ferrocarriles, it has a TSR of 68% for the last 5 years. That exceeds its share price return that we previously mentioned. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

Although it hurts that Construcciones y Auxiliar de Ferrocarriles returned a loss of 3.8% in the last twelve months, the broader market was actually worse, returning a loss of 11%. Of course, the long term returns are far more important and the good news is that over five years, the stock has returned 11% for each year. It could be that the business is just facing some short term problems, but shareholders should keep a close eye on the fundamentals. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For instance, we've identified 4 warning signs for Construcciones y Auxiliar de Ferrocarriles (1 is concerning) that you should be aware of.

But note: Construcciones y Auxiliar de Ferrocarriles may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on ES exchanges.

If you decide to trade Construcciones y Auxiliar de Ferrocarriles, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BME:CAF

Construcciones y Auxiliar de Ferrocarriles

Construcciones y Auxiliar de Ferrocarriles, S.A.

Undervalued with proven track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives