Advertisement

Bankinter (BME:BKT) Will Pay A Larger Dividend Than Last Year At €0.1217

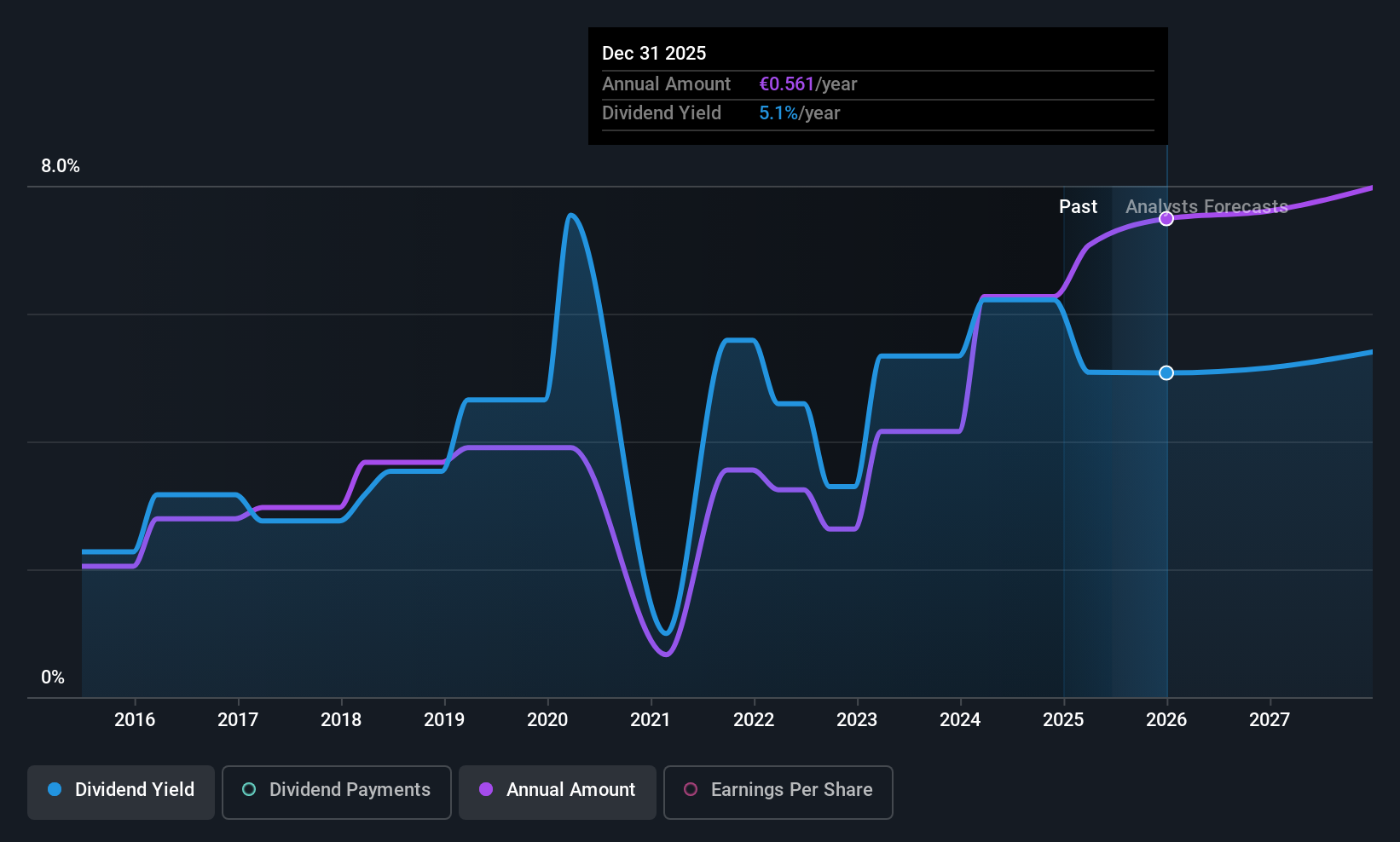

Bankinter, S.A. (BME:BKT) will increase its dividend from last year's comparable payment on the 25th of June to €0.1217. The payment will take the dividend yield to 4.8%, which is in line with the average for the industry.

Bankinter's Earnings Will Easily Cover The Distributions

We like to see a healthy dividend yield, but that is only helpful to us if the payment can continue.

Bankinter has a long history of paying out dividends, with its current track record at a minimum of 10 years. Based on Bankinter's last earnings report, the payout ratio is at a decent 37%, meaning that the company is able to pay out its dividend with a bit of room to spare.

Looking forward, EPS is forecast to rise by 2.6% over the next 3 years. Analysts forecast the future payout ratio could be 51% over the same time horizon, which is a number we think the company can maintain.

View our latest analysis for Bankinter

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The dividend has gone from an annual total of €0.154 in 2015 to the most recent total annual payment of €0.53. This implies that the company grew its distributions at a yearly rate of about 13% over that duration. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Bankinter has impressed us by growing EPS at 20% per year over the past five years. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

Bankinter Looks Like A Great Dividend Stock

Overall, a dividend increase is always good, and we think that Bankinter is a strong income stock thanks to its track record and growing earnings. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All of these factors considered, we think this has solid potential as a dividend stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 1 warning sign for Bankinter that investors need to be conscious of moving forward. Is Bankinter not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Bankinter might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:BKT

Bankinter

Provides various banking products and services to individuals and corporate customers, and small- and medium-sized enterprises in Spain.

Average dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor