- Estonia

- /

- Construction

- /

- TLSE:NCN1T

Don't Race Out To Buy Nordecon AS (TAL:NCN1T) Just Because It's Going Ex-Dividend

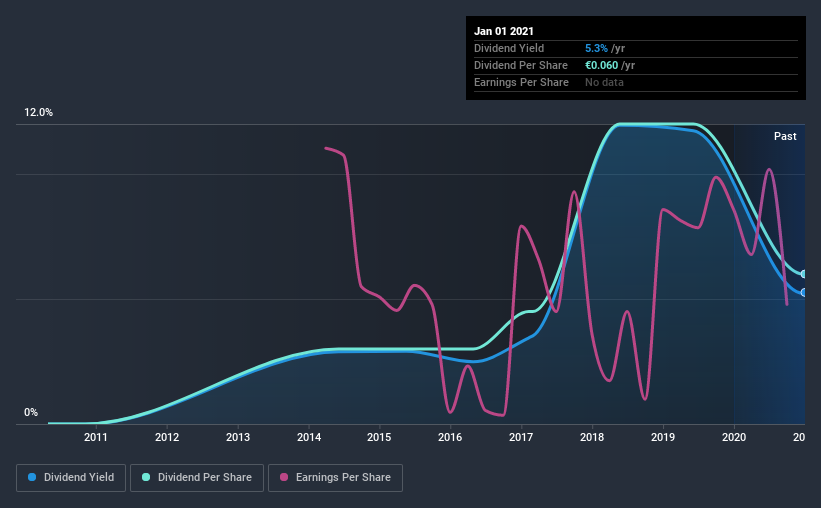

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Nordecon AS (TAL:NCN1T) is about to go ex-dividend in just three days. If you purchase the stock on or after the 6th of January, you won't be eligible to receive this dividend, when it is paid on the 25th of March.

Nordecon's next dividend payment will be €0.06 per share. Last year, in total, the company distributed €0.06 to shareholders. Looking at the last 12 months of distributions, Nordecon has a trailing yield of approximately 5.3% on its current stock price of €1.14. If you buy this business for its dividend, you should have an idea of whether Nordecon's dividend is reliable and sustainable. As a result, readers should always check whether Nordecon has been able to grow its dividends, or if the dividend might be cut.

Check out our latest analysis for Nordecon

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Nordecon paid out 100% of its earnings, which is more than we're comfortable with, unless there are mitigating circumstances. A useful secondary check can be to evaluate whether Nordecon generated enough free cash flow to afford its dividend. It distributed 49% of its free cash flow as dividends, a comfortable payout level for most companies.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Nordecon fortunately did generate enough cash to fund its dividend. If executives were to continue paying more in dividends than the company reported in profits, we'd view this as a warning sign. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

Click here to see how much of its profit Nordecon paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks with flat earnings can still be attractive dividend payers, but it is important to be more conservative with your approach and demand a greater margin for safety when it comes to dividend sustainability. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. It's not encouraging to see that Nordecon's earnings are effectively flat over the past five years. It's better than seeing them drop, certainly, but over the long term, all of the best dividend stocks are able to meaningfully grow their earnings per share.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Since the start of our data, seven years ago, Nordecon has lifted its dividend by approximately 10% a year on average.

Final Takeaway

Has Nordecon got what it takes to maintain its dividend payments? Earnings per share have been effectively flat, which is a bit of a concern given the company is paying out 100% of its profit as dividends, which we feel is uncomfortably high. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

With that being said, if you're still considering Nordecon as an investment, you'll find it beneficial to know what risks this stock is facing. To help with this, we've discovered 4 warning signs for Nordecon (1 doesn't sit too well with us!) that you ought to be aware of before buying the shares.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade Nordecon, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade Nordecon, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nordecon might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TLSE:NCN1T

Nordecon

Operates as a construction company in Estonia, Sweden, Finland, Ukraine, Latvia, and Lithuania.

Adequate balance sheet with acceptable track record.

Similar Companies

Market Insights

Community Narratives