- Denmark

- /

- Specialty Stores

- /

- CPSE:MATAS

These 4 Measures Indicate That Matas (CPH:MATAS) Is Using Debt Reasonably Well

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Matas A/S (CPH:MATAS) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Matas

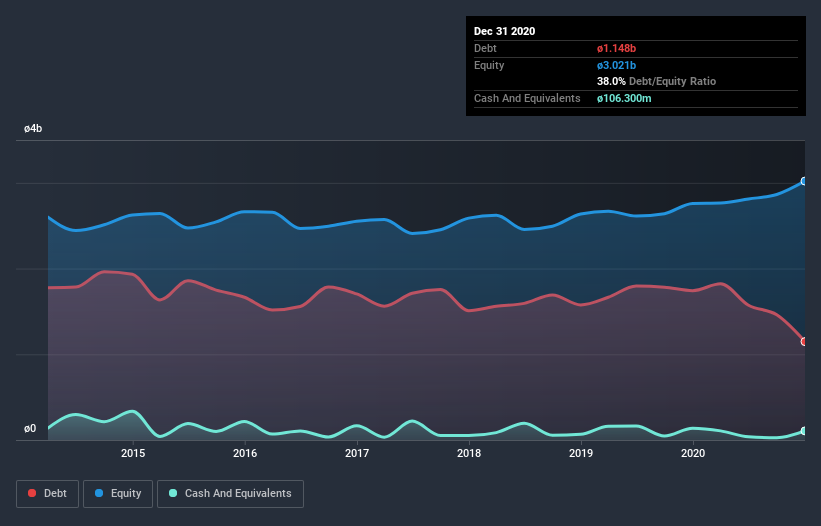

How Much Debt Does Matas Carry?

You can click the graphic below for the historical numbers, but it shows that Matas had kr.1.15b of debt in December 2020, down from kr.1.74b, one year before. However, it does have kr.106.3m in cash offsetting this, leading to net debt of about kr.1.04b.

A Look At Matas' Liabilities

We can see from the most recent balance sheet that Matas had liabilities of kr.1.33b falling due within a year, and liabilities of kr.1.91b due beyond that. Offsetting this, it had kr.106.3m in cash and kr.28.3m in receivables that were due within 12 months. So it has liabilities totalling kr.3.11b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of kr.3.13b, so it does suggest shareholders should keep an eye on Matas' use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Matas's net debt to EBITDA ratio of about 1.8 suggests only moderate use of debt. And its commanding EBIT of 13.4 times its interest expense, implies the debt load is as light as a peacock feather. Matas grew its EBIT by 4.3% in the last year. Whilst that hardly knocks our socks off it is a positive when it comes to debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Matas's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. Happily for any shareholders, Matas actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Matas's interest cover was a real positive on this analysis, as was its conversion of EBIT to free cash flow. Having said that, its level of total liabilities somewhat sensitizes us to potential future risks to the balance sheet. Considering this range of data points, we think Matas is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. Over time, share prices tend to follow earnings per share, so if you're interested in Matas, you may well want to click here to check an interactive graph of its earnings per share history.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

When trading Matas or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About CPSE:MATAS

Matas

Operates a chain of retail stores that offer beauty, personal care, health and wellbeing, and household products in Denmark.

Good value slight.