To find a multi-bagger stock, what are the underlying trends we should look for in a business? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. So, when we ran our eye over TCM Group's (CPH:TCM) trend of ROCE, we really liked what we saw.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for TCM Group, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.20 = kr.143m ÷ (kr.945m - kr.240m) (Based on the trailing twelve months to March 2021).

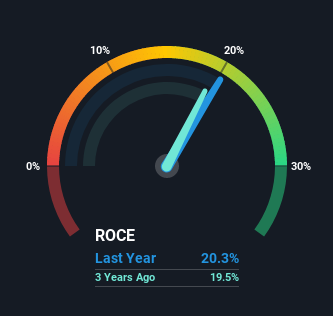

Therefore, TCM Group has an ROCE of 20%. That's a fantastic return and not only that, it outpaces the average of 11% earned by companies in a similar industry.

Check out our latest analysis for TCM Group

Above you can see how the current ROCE for TCM Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering TCM Group here for free.

What Can We Tell From TCM Group's ROCE Trend?

We'd be pretty happy with returns on capital like TCM Group. Over the past five years, ROCE has remained relatively flat at around 20% and the business has deployed 101% more capital into its operations. With returns that high, it's great that the business can continually reinvest its money at such appealing rates of return. If TCM Group can keep this up, we'd be very optimistic about its future.

The Key Takeaway

In the end, the company has proven it can reinvest it's capital at high rates of returns, which you'll remember is a trait of a multi-bagger. Therefore it's no surprise that shareholders have earned a respectable 89% return if they held over the last three years. So while investors seem to be recognizing these promising trends, we still believe the stock deserves further research.

Like most companies, TCM Group does come with some risks, and we've found 1 warning sign that you should be aware of.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if TCM Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About CPSE:TCM

TCM Group

Manufactures and sells kitchen and furniture products for bathrooms and storage in Denmark, Norway, and internationally.

Reasonable growth potential with proven track record.

Market Insights

Community Narratives