- Denmark

- /

- Electrical

- /

- CPSE:VWS

Vestas Wind Systems Leads Trio Of Stocks Estimated To Be Below Intrinsic Value

Reviewed by Simply Wall St

As global markets exhibit a mix of trends with record highs in major indices and nuanced shifts in small-cap stocks, investors are keenly watching for opportunities that may be undervalued relative to their intrinsic worth. In this context, identifying stocks like Vestas Wind Systems that potentially trade below their fundamental value could be particularly compelling amidst the current economic landscape.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| DXN Holdings Bhd (KLSE:DXN) | MYR0.635 | MYR1.26 | 49.7% |

| Acerinox (BME:ACX) | €10.00 | €19.95 | 49.9% |

| Duckhorn Portfolio (NYSE:NAPA) | US$7.19 | US$14.30 | 49.7% |

| hipages Group Holdings (ASX:HPG) | A$1.04 | A$2.06 | 49.5% |

| Eletromidia (BOVESPA:ELMD3) | R$18.45 | R$36.78 | 49.8% |

| Terveystalo Oyj (HLSE:TTALO) | €9.58 | €19.00 | 49.6% |

| Musti Group Oyj (HLSE:MUSTI) | €26.65 | €52.85 | 49.6% |

| YIT Oyj (HLSE:YIT) | €2.33 | €4.66 | 50% |

| Elementis (LSE:ELM) | £1.514 | £3.02 | 49.9% |

| Vasta Platform (NasdaqGS:VSTA) | US$3.025 | US$6.01 | 49.7% |

Let's review some notable picks from our screened stocks.

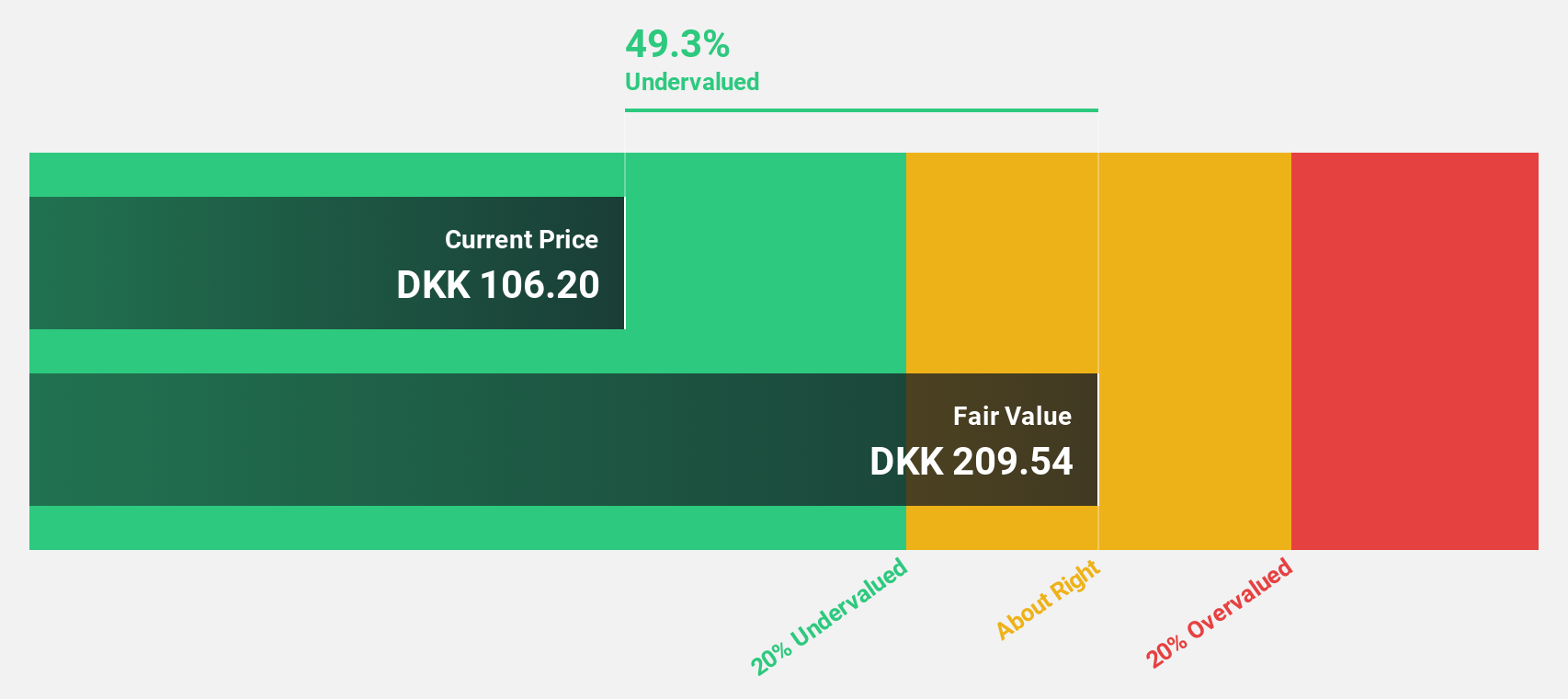

Vestas Wind Systems (CPSE:VWS)

Overview: Vestas Wind Systems A/S is a global company specializing in the design, manufacture, installation, and servicing of wind turbines, with a market capitalization of approximately DKK 170 billion.

Operations: The company generates revenue primarily through two segments: Power Solutions (€11.57 billion) and Service (€3.66 billion).

Estimated Discount To Fair Value: 30.8%

Vestas Wind Systems, currently priced at DKK168.45, is significantly undervalued by 30.8% against a fair value of DKK243.51 based on discounted cash flow analysis. With earnings projected to grow at 39.09% annually, Vestas is expected to turn profitable within the next three years, outpacing average market growth rates. Recent orders for their advanced turbines in global markets underline its operational expansion and potential revenue increase, although current revenue growth forecasts (11.4% annually) slightly trail behind the desired 20% threshold.

- According our earnings growth report, there's an indication that Vestas Wind Systems might be ready to expand.

- Dive into the specifics of Vestas Wind Systems here with our thorough financial health report.

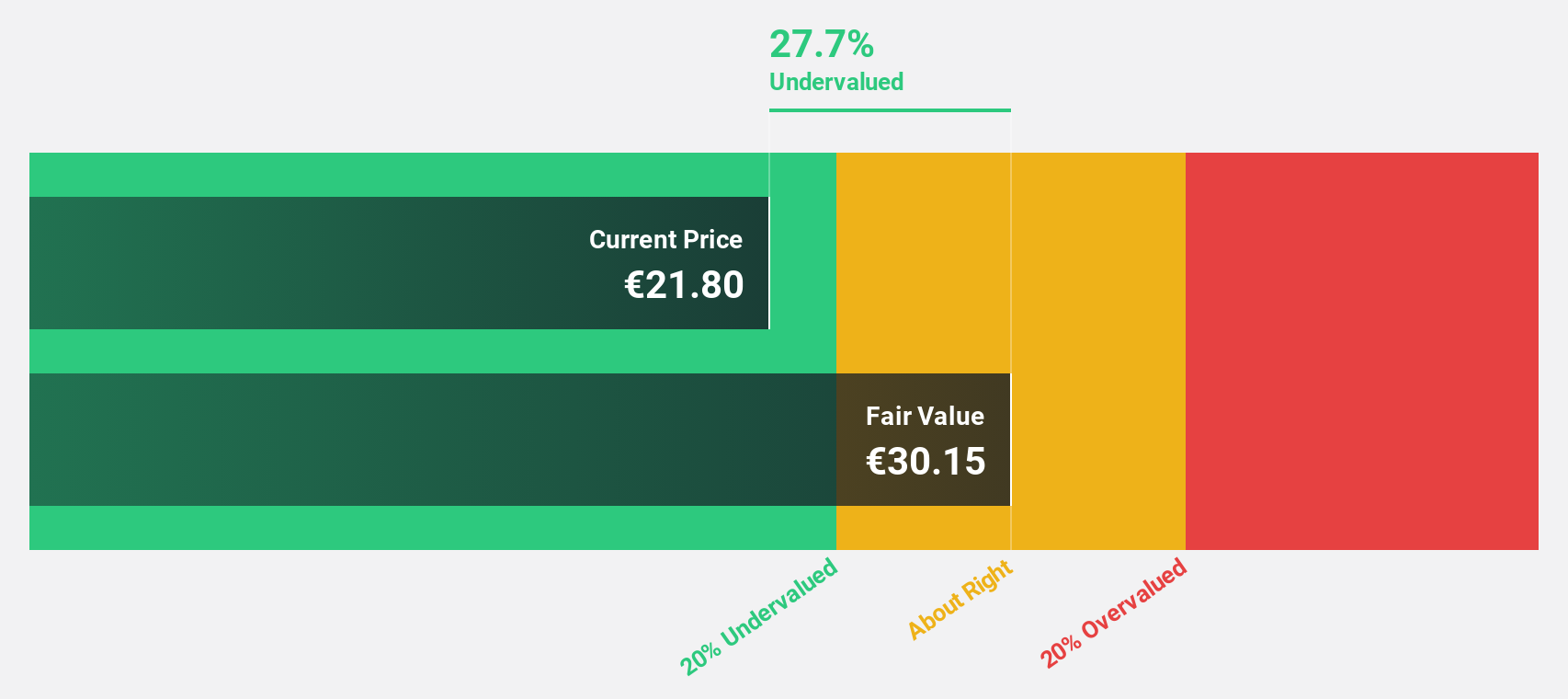

Jerónimo Martins SGPS (ENXTLS:JMT)

Overview: Jerónimo Martins SGPS, S.A. is a company engaged in food distribution and specialized retail, operating across Portugal, Poland, and Colombia, with a market capitalization of approximately €12.33 billion.

Operations: The company generates revenue primarily through its retail operations in Poland and Colombia, with segments reporting €22.41 billion and €2.65 billion respectively.

Estimated Discount To Fair Value: 41.2%

Jerónimo Martins SGPS, trading at €19.62, is valued 41.2% below its estimated fair value of €33.38, reflecting potential underpricing based on cash flows. Despite a recent dip in net income to €97 million from last year's €140 million and lower EPS of €0.15, the company's revenue growth outpaces the Portuguese market at 7.1% annually compared to 5.2%. Earnings are expected to grow by 8.27% per year with a forecasted high Return on Equity of 24.5% in three years, though its dividend record remains unstable.

- Insights from our recent growth report point to a promising forecast for Jerónimo Martins SGPS' business outlook.

- Navigate through the intricacies of Jerónimo Martins SGPS with our comprehensive financial health report here.

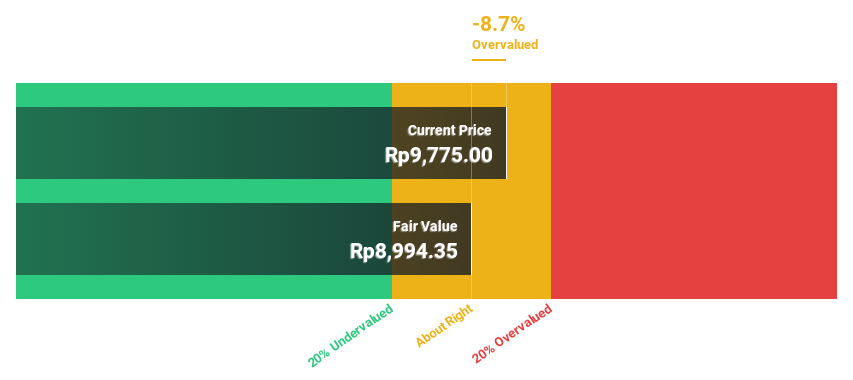

Pantai Indah Kapuk Dua (IDX:PANI)

Overview: PT Pantai Indah Kapuk Dua Tbk, along with its subsidiaries, functions as a property developer in Indonesia with a market capitalization of approximately IDR 87.12 trillion.

Operations: The company's primary revenue of IDR 1.92 billion is generated from its real estate segment.

Estimated Discount To Fair Value: 31.2%

PT Pantai Indah Kapuk Dua Tbk, priced at IDR5575, trades below its fair value of IDR8105.51, suggesting a significant undervaluation based on discounted cash flows. Despite a decrease in sales to IDR 640.36 billion and net income to IDR 122.38 million this quarter from last year's figures, the company is poised for robust future growth with earnings expected to rise by 47.7% annually and revenue forecasted to grow at 29.6% per year—both metrics surpassing market averages significantly.

- In light of our recent growth report, it seems possible that Pantai Indah Kapuk Dua's financial performance will exceed current levels.

- Take a closer look at Pantai Indah Kapuk Dua's balance sheet health here in our report.

Make It Happen

- Reveal the 951 hidden gems among our Undervalued Stocks Based On Cash Flows screener with a single click here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About CPSE:VWS

Vestas Wind Systems

Engages in the design, manufacture, installation, and services of wind turbines the United States, Denmark, and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Community Narratives