With EPS Growth And More, Sydbank (CPH:SYDB) Makes An Interesting Case

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Sydbank (CPH:SYDB). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Sydbank with the means to add long-term value to shareholders.

Check out our latest analysis for Sydbank

How Fast Is Sydbank Growing Its Earnings Per Share?

Sydbank has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. As a result, we'll zoom in on growth over the last year, instead. Outstandingly, Sydbank's EPS shot from kr.26.65 to kr.56.24, over the last year. It's not often a company can achieve year-on-year growth of 111%. The best case scenario? That the business has hit a true inflection point.

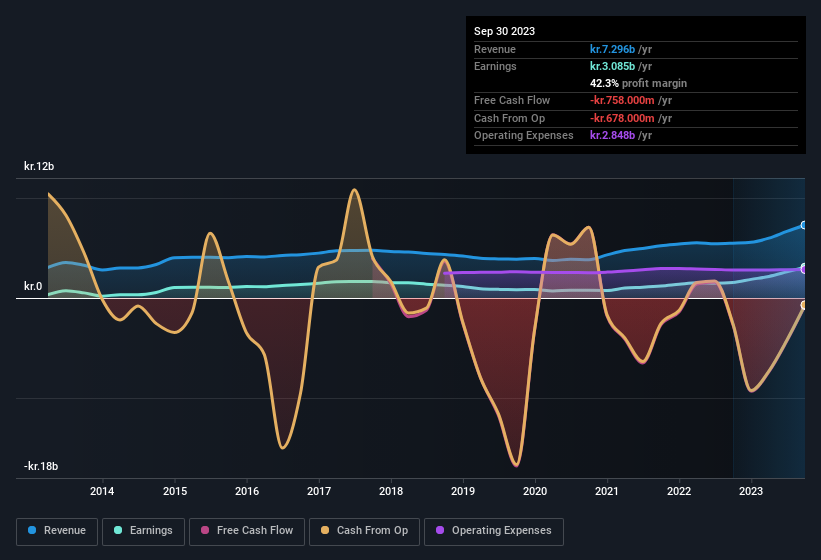

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. Our analysis has highlighted that Sydbank's revenue from operations did not account for all of their revenue in the previous 12 months, so our analysis of its margins might not accurately reflect the underlying business. EBIT margins for Sydbank remained fairly unchanged over the last year, however the company should be pleased to report its revenue growth for the period of 33% to kr.7.3b. That's progress.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

Fortunately, we've got access to analyst forecasts of Sydbank's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Sydbank Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Despite some Sydbank insiders disposing of some shares, we note that there was kr.933k more in buying interest among those who know the company best Although some people may hesitate due to the share sales, the fact that insiders bought more than they sold, is a positive thing to note. Zooming in, we can see that the biggest insider purchase was by Independent Director Soren Holm for kr.319k worth of shares, at about kr.319 per share.

Recent insider purchases of Sydbank stock is not the only way management has kept the interests of the general public shareholders in mind. To be specific, the CEO is paid modestly when compared to company peers of the same size. For companies with market capitalisations between kr.6.8b and kr.22b, like Sydbank, the median CEO pay is around kr.16m.

Sydbank offered total compensation worth kr.8.3m to its CEO in the year to December 2022. That seems pretty reasonable, especially given it's below the median for similar sized companies. While the level of CEO compensation shouldn't be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Does Sydbank Deserve A Spot On Your Watchlist?

Sydbank's earnings have taken off in quite an impressive fashion. Better yet, we can observe insider buying and the chief executive pay looks reasonable. It could be that Sydbank is at an inflection point, given the EPS growth. For those attracted to fast growth, we'd suggest this stock merits monitoring. Before you take the next step you should know about the 2 warning signs for Sydbank (1 is a bit unpleasant!) that we have uncovered.

The good news is that Sydbank is not the only growth stock with insider buying. Here's a list of growth-focused companies in DK with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About CPSE:ALSYDB

AL Sydbank

Provides various banking products and services to corporate, private, retail, and institutional clients in Denmark and internationally.

Excellent balance sheet established dividend payer.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)