USU Software AG Just Recorded A 6.1% EPS Beat: Here's What Analysts Are Forecasting Next

Investors in USU Software AG (ETR:OSP2) had a good week, as its shares rose 4.8% to close at €28.40 following the release of its yearly results. The result was positive overall - although revenues of €107m were in line with what the analysts predicted, USU Software surprised by delivering a statutory profit of €0.52 per share, modestly greater than expected. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on USU Software after the latest results.

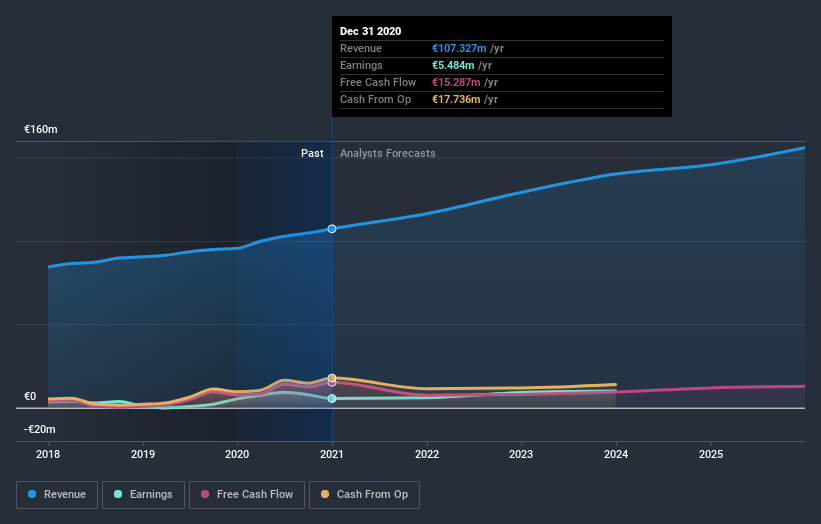

View our latest analysis for USU Software

Following the latest results, USU Software's twin analysts are now forecasting revenues of €116.4m in 2021. This would be a notable 8.4% improvement in sales compared to the last 12 months. Statutory earnings per share are predicted to increase 9.4% to €0.57. Yet prior to the latest earnings, the analysts had been anticipated revenues of €117.9m and earnings per share (EPS) of €0.78 in 2021. So there's definitely been a decline in sentiment after the latest results, noting the pretty serious reduction to new EPS forecasts.

Althoughthe analysts have revised their earnings forecasts for next year, they've also lifted the consensus price target 5.7% to €27.75, suggesting the revised estimates are not indicative of a weaker long-term future for the business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. The period to the end of 2021 brings more of the same, according to the analysts, with revenue forecast to display 8.4% growth on an annualised basis. That is in line with its 9.4% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 6.1% per year. So it's pretty clear that USU Software is forecast to grow substantially faster than its industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for USU Software. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2025, which can be seen for free on our platform here.

You can also see our analysis of USU Software's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

When trading USU Software or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About XTRA:OSP2

USU Software

Provides software and service solutions for information technology (IT) and customer service management in Germany and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Automotive Electronics Manufacturer Consistent and Stable

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion