Advertisement

Assessing Bechtle (XTRA:BC8) Valuation As ROCE Slips And Growth Expectations Cool

Bechtle (XTRA:BC8) is back in focus after a reported slide in return on capital employed from 15% to 12% over five years, raising fresh questions about how efficiently its reinvested cash is working.

See our latest analysis for Bechtle.

At a share price of €44.36, Bechtle has a 90 day share price return of 25.52%, while the 1 year total shareholder return of 52.57% contrasts with a 5 year total shareholder return decline of 17.95%, suggesting momentum has picked up recently even as longer term holders are still behind.

If Bechtle’s mixed track record has you thinking about diversification, this could be a good moment to scan high growth tech and AI stocks for other IT focused opportunities on your radar.

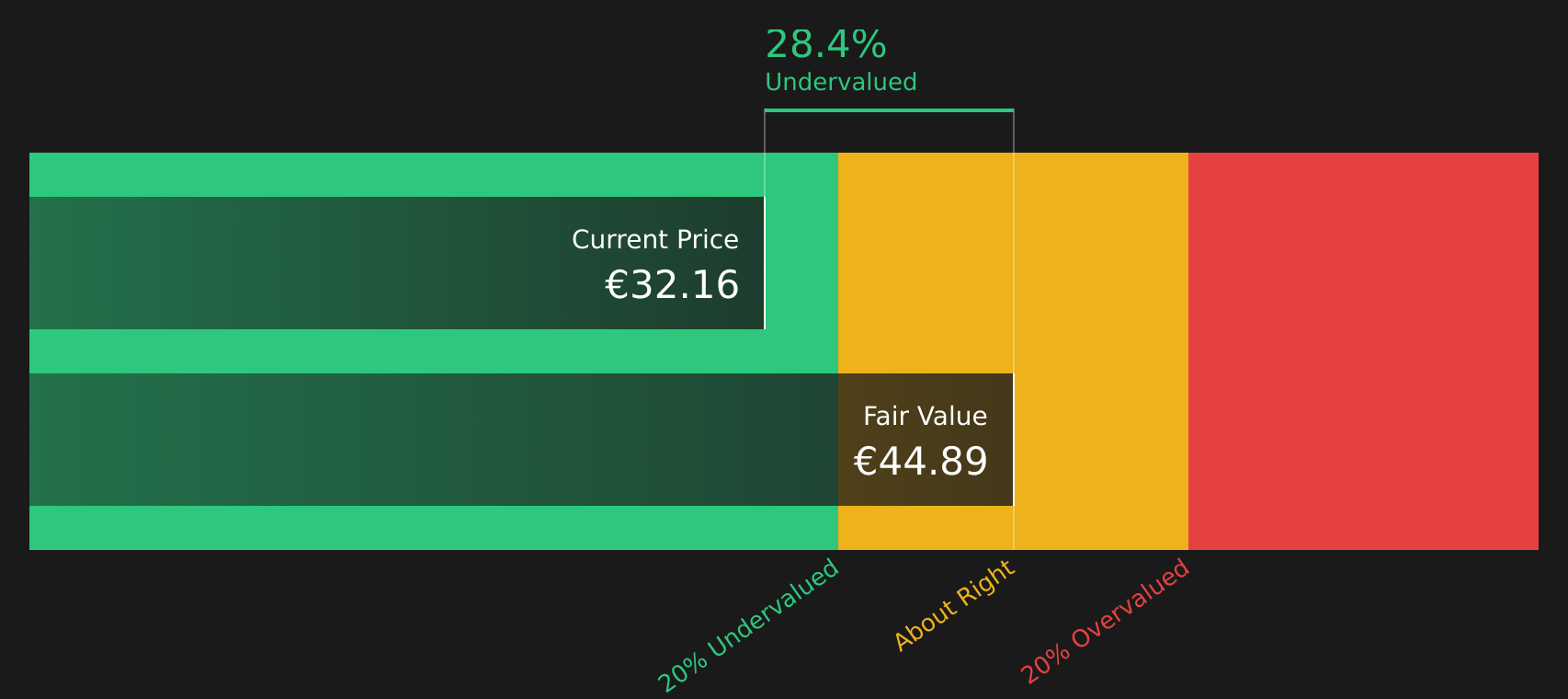

With Bechtle trading around €44.36 and showing a 15% intrinsic discount, while its ROCE remains above the sector average despite easing, investors may wonder whether there is still a buying opportunity or if future growth is already priced in.

Most Popular Narrative: 1% Overvalued

With Bechtle last closing at €44.36 versus a narrative fair value of about €44.08, the gap is narrow, yet the underlying story is detailed and data heavy.

Analysts are assuming Bechtle's revenue will grow by 6.6% annually over the next 3 years. Analysts assume that profit margins will increase from 3.4% today to 3.9% in 3 years time.

Curious what supports that tighter margin profile and higher earnings base over time? The narrative leans on specific revenue paths, firmer profitability and a future earnings multiple that assumes investors stay comfortable paying up for those targets.

Result: Fair Value of $44.08 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative could easily wobble if SME customers keep delaying IT projects or if changes to partner incentives, such as at Microsoft, hit earnings harder than expected.

Find out about the key risks to this Bechtle narrative.

Another View: Cash Flows Paint A Different Picture

While the narrative fair value of about €44.08 suggests Bechtle is roughly fairly priced, our DCF model takes a different line. With shares at €44.36 and a fair value estimate of €52.32, the cash flow view points to meaningful upside that the narrative framework does not fully capture. Which lens do you think fits your expectations better?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bechtle for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 885 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Bechtle Narrative

If you see the figures differently or prefer to rely on your own analysis, you can test the assumptions, adjust the drivers and Do it your way in just a few minutes.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Bechtle.

Ready For More Investment Ideas?

If Bechtle is just one piece of your watchlist, this is a great time to widen your search and see what else stands out on the numbers.

- Spot potential mispricings by scanning these 885 undervalued stocks based on cash flows that may offer a more attractive entry point based on their cash flow profiles.

- Target future facing themes by tracking these 25 AI penny stocks that are tied to artificial intelligence trends across different parts of the market.

- Strengthen your income focus by sorting through these 13 dividend stocks with yields > 3% that meet your yield threshold and help balance out growth oriented positions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bechtle might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:BC8

Bechtle

Provides information technology (IT) services in Germany, France, Benelux, and Europe.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0778.3% undervalued

206 followersusers have followed this narrative

1 commentusers have commented on this narrative

29 likesusers have liked this narrative

SI

SimpleMan887 on GameStop ·

GameStop will ace the financial crisis wave with its strategic Bitcoin investment and cash reserves

Fair Value:US$22089.6% undervalued

51 followersusers have followed this narrative

2 commentsusers have commented on this narrative

21 likesusers have liked this narrative

YI

yiannisz on Hesai Group ·

The First Real Lidar Winner

Fair Value:US$27.0719.2% undervalued

13 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

TR

tripledub on Taiwan Semiconductor Manufacturing ·

The Most Wonderful Monopoly in the Most Dangerous Neighbourhood on Earth

Fair Value:US$3814.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on Ceres ·

Proven business incubator in transition

Fair Value:JP¥2.37k36.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on Hektar Real Estate Investment Trust ·

Hektar REIT: Outlook is getting more interesting as retail stabilises and diversification starts to kick in

Fair Value:RM 0.4910.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Guanajuato Silver ·

A Case for Guanajuato Silver (TSXV:GSVR) to reach (low end) CAD$4 (high end) CAD$18 by 2031

Fair Value:CA$1896.6% undervalued

19 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9828.2% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

38 likesusers have liked this narrative

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.2% undervalued

43 followersusers have followed this narrative

3 commentsusers have commented on this narrative

41 likesusers have liked this narrative

RO

Robbo on Tesla ·

The academically fascinating Tesla

Fair Value:US$301.0k% overvalued

36 followersusers have followed this narrative

11 commentsusers have commented on this narrative

31 likesusers have liked this narrative