Advertisement

Weak Financial Prospects Seem To Be Dragging Down Allgeier SE (ETR:AEIN) Stock

Allgeier (ETR:AEIN) has had a rough month with its share price down 16%. To decide if this trend could continue, we decided to look at its weak fundamentals as they shape the long-term market trends. Particularly, we will be paying attention to Allgeier's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for Allgeier

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Allgeier is:

3.9% = €4.4m ÷ €112m (Based on the trailing twelve months to September 2021).

The 'return' is the income the business earned over the last year. That means that for every €1 worth of shareholders' equity, the company generated €0.04 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Allgeier's Earnings Growth And 3.9% ROE

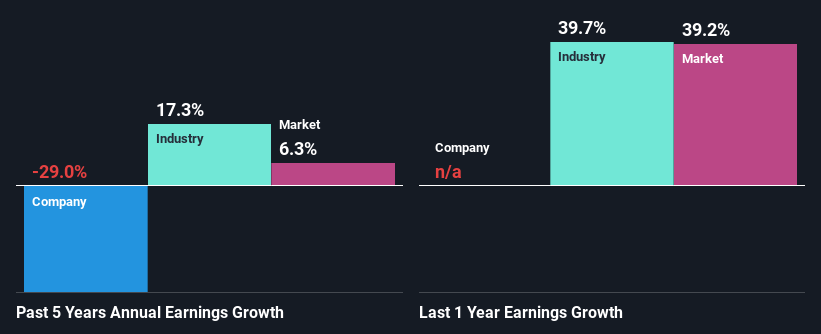

When you first look at it, Allgeier's ROE doesn't look that attractive. Next, when compared to the average industry ROE of 14%, the company's ROE leaves us feeling even less enthusiastic. For this reason, Allgeier's five year net income decline of 29% is not surprising given its lower ROE. We believe that there also might be other aspects that are negatively influencing the company's earnings prospects. For instance, the company has a very high payout ratio, or is faced with competitive pressures.

So, as a next step, we compared Allgeier's performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 17% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. Is Allgeier fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Allgeier Efficiently Re-investing Its Profits?

Allgeier's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its LTM (or last twelve month) payout ratio of 85% (or a retention ratio of 15%). The business is only left with a small pool of capital to reinvest - A vicious cycle that doesn't benefit the company in the long-run. To know the 2 risks we have identified for Allgeier visit our risks dashboard for free.

Additionally, Allgeier has paid dividends over a period of four years, which means that the company's management is rather focused on keeping up its dividend payments, regardless of the shrinking earnings. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 28% over the next three years. As a result, the expected drop in Allgeier's payout ratio explains the anticipated rise in the company's future ROE to 20%, over the same period.

Summary

On the whole, Allgeier's performance is quite a big let-down. Because the company is not reinvesting much into the business, and given the low ROE, it's not surprising to see the lack or absence of growth in its earnings. That being so, the latest industry analyst forecasts show that the analysts are expecting to see a huge improvement in the company's earnings growth rate. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:AEIN

Allgeier

Provides information technology (IT) solutions and software services in Germany.

Reasonable growth potential with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets