Advertisement

adesso SE (ETR:ADN1) Just Reported And Analysts Have Been Lifting Their Price Targets

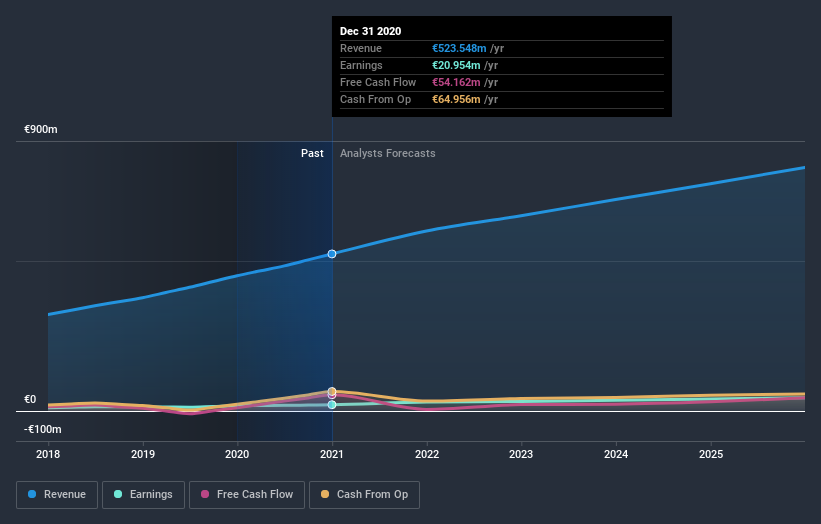

Investors in adesso SE (ETR:ADN1) had a good week, as its shares rose 9.0% to close at €113 following the release of its yearly results. It was a pretty mixed result, with revenues beating expectations to hit €524m. Statutory earnings fell 4.4% short of analyst forecasts, reaching €3.39 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for adesso

Following the latest results, adesso's twin analysts are now forecasting revenues of €600.0m in 2021. This would be a decent 15% improvement in sales compared to the last 12 months. Per-share earnings are expected to jump 42% to €4.82. Before this earnings report, the analysts had been forecasting revenues of €584.1m and earnings per share (EPS) of €4.30 in 2021. So it seems there's been a definite increase in optimism about adesso's future following the latest results, with a substantial gain in the earnings per share forecasts in particular.

With these upgrades, we're not surprised to see that the analysts have lifted their price target 6.5% to €123per share.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the adesso's past performance and to peers in the same industry. We can infer from the latest estimates that forecasts expect a continuation of adesso'shistorical trends, as the 15% annualised revenue growth to the end of 2021 is roughly in line with the 18% annual revenue growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 7.8% annually. So it's pretty clear that adesso is forecast to grow substantially faster than its industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around adesso's earnings potential next year. Happily, they also upgraded their revenue estimates, and are forecasting revenues to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2025, which can be seen for free on our platform here.

Even so, be aware that adesso is showing 1 warning sign in our investment analysis , you should know about...

When trading adesso or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About XTRA:ADN1

adesso

Provides IT services in Germany, Austria, Switzerland, and internationally.

Reasonable growth potential with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor