Advertisement

- Germany

- /

- Metals and Mining

- /

- XTRA:TKA

Here's Why thyssenkrupp (ETR:TKA) Is Weighed Down By Its Debt Load

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that thyssenkrupp AG (ETR:TKA) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for thyssenkrupp

What Is thyssenkrupp's Net Debt?

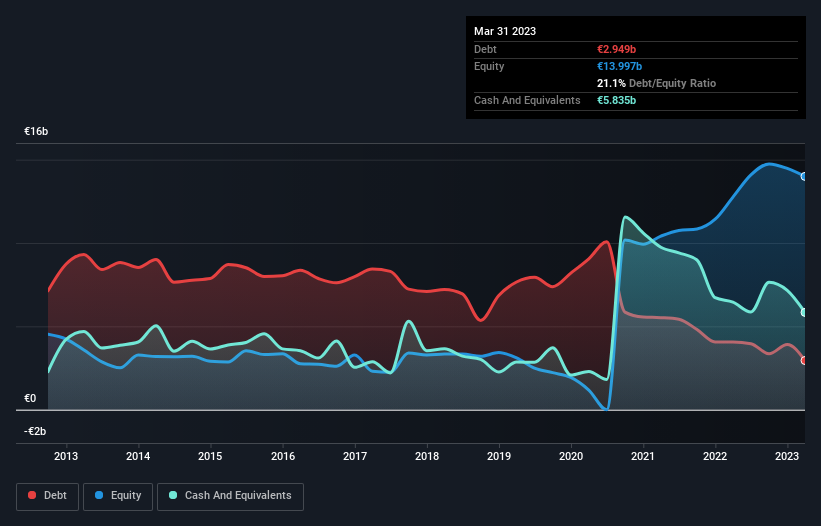

The image below, which you can click on for greater detail, shows that thyssenkrupp had debt of €2.95b at the end of March 2023, a reduction from €4.06b over a year. However, it does have €5.84b in cash offsetting this, leading to net cash of €2.89b.

How Healthy Is thyssenkrupp's Balance Sheet?

According to the last reported balance sheet, thyssenkrupp had liabilities of €13.4b due within 12 months, and liabilities of €7.70b due beyond 12 months. Offsetting this, it had €5.84b in cash and €7.56b in receivables that were due within 12 months. So its liabilities total €7.74b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the €4.29b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, thyssenkrupp would likely require a major re-capitalisation if it had to pay its creditors today. Given that thyssenkrupp has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total.

The modesty of its debt load may become crucial for thyssenkrupp if management cannot prevent a repeat of the 69% cut to EBIT over the last year. When a company sees its earnings tank, it can sometimes find its relationships with its lenders turn sour. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine thyssenkrupp's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While thyssenkrupp has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last two years, thyssenkrupp burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing Up

Although thyssenkrupp's balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of €2.89b. Unfortunately, though, both its struggle level of total liabilities and its EBIT growth rate leave us concerned about thyssenkrupp So even though it has net cash, we do think the business has some risks worth watching. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example - thyssenkrupp has 3 warning signs we think you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:TKA

thyssenkrupp

Operates as an industrial and technology company in Germany and internationally.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.1% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|15.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|0% overvalued

RO

Community Contributor