Advertisement

- Germany

- /

- Medical Equipment

- /

- XTRA:EUZ

Eckert & Ziegler SE's (ETR:EUZ) P/E Is Still On The Mark Following 27% Share Price Bounce

Eckert & Ziegler SE (ETR:EUZ) shareholders are no doubt pleased to see that the share price has bounced 27% in the last month, although it is still struggling to make up recently lost ground. The last 30 days bring the annual gain to a very sharp 47%.

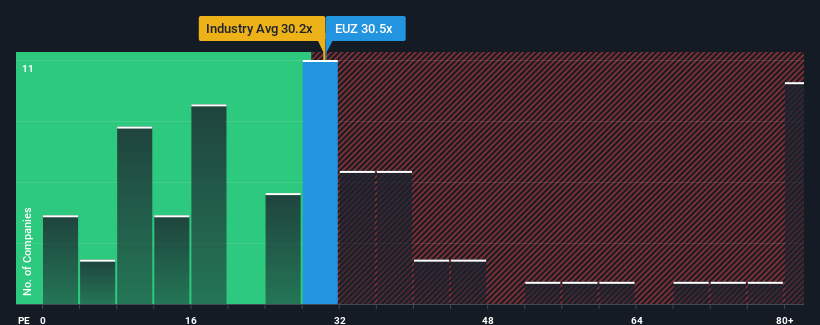

After such a large jump in price, Eckert & Ziegler's price-to-earnings (or "P/E") ratio of 30.5x might make it look like a strong sell right now compared to the market in Germany, where around half of the companies have P/E ratios below 18x and even P/E's below 10x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

We check all companies for important risks. See what we found for Eckert & Ziegler in our free report.Eckert & Ziegler certainly has been doing a good job lately as it's been growing earnings more than most other companies. It seems that many are expecting the strong earnings performance to persist, which has raised the P/E. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Eckert & Ziegler

Is There Enough Growth For Eckert & Ziegler?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Eckert & Ziegler's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 33% gain to the company's bottom line. EPS has also lifted 15% in aggregate from three years ago, mostly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Turning to the outlook, the next year should generate growth of 24% as estimated by the one analyst watching the company. Meanwhile, the rest of the market is forecast to only expand by 18%, which is noticeably less attractive.

With this information, we can see why Eckert & Ziegler is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Eckert & Ziegler's P/E

The strong share price surge has got Eckert & Ziegler's P/E rushing to great heights as well. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Eckert & Ziegler maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. It's hard to see the share price falling strongly in the near future under these circumstances.

The company's balance sheet is another key area for risk analysis. Take a look at our free balance sheet analysis for Eckert & Ziegler with six simple checks on some of these key factors.

You might be able to find a better investment than Eckert & Ziegler. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Eckert & Ziegler might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:EUZ

Eckert & Ziegler

Manufactures and sells isotope technology components worldwide.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.0% undervalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|20.4% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|36.8% undervalued

TR

Community Contributor