- Germany

- /

- Medical Equipment

- /

- XTRA:AFX

Carl Zeiss Meditec AG (ETR:AFX) Passed Our Checks, And It's About To Pay A €1.10 Dividend

Carl Zeiss Meditec AG (ETR:AFX) stock is about to trade ex-dividend in three days. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. Meaning, you will need to purchase Carl Zeiss Meditec's shares before the 23rd of March to receive the dividend, which will be paid on the 27th of March.

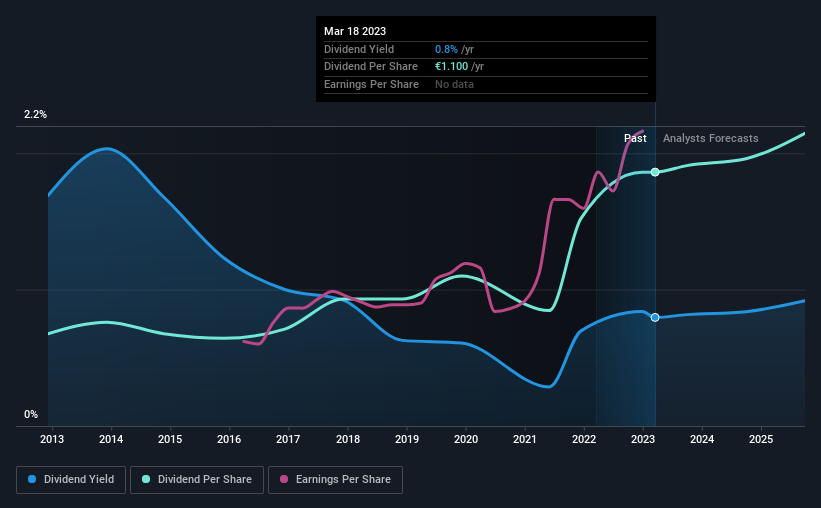

The company's next dividend payment will be €1.10 per share. Last year, in total, the company distributed €1.10 to shareholders. Based on the last year's worth of payments, Carl Zeiss Meditec has a trailing yield of 0.8% on the current stock price of €138.15. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to check whether the dividend payments are covered, and if earnings are growing.

See our latest analysis for Carl Zeiss Meditec

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. That's why it's good to see Carl Zeiss Meditec paying out a modest 32% of its earnings. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. It paid out 76% of its free cash flow as dividends, which is within usual limits but will limit the company's ability to lift the dividend if there's no growth.

It's positive to see that Carl Zeiss Meditec's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. For this reason, we're glad to see Carl Zeiss Meditec's earnings per share have risen 17% per annum over the last five years. It paid out more than three-quarters of its earnings in the last year, even though earnings per share are growing rapidly. We're surprised that management has not elected to reinvest more in the business to accelerate growth further.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. In the last 10 years, Carl Zeiss Meditec has lifted its dividend by approximately 11% a year on average. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

To Sum It Up

Has Carl Zeiss Meditec got what it takes to maintain its dividend payments? From a dividend perspective, we're encouraged to see that earnings per share have been growing, the company is paying out less than half of its earnings, and a bit over half its free cash flow. It's a promising combination that should mark this company worthy of closer attention.

Curious what other investors think of Carl Zeiss Meditec? See what analysts are forecasting, with this visualisation of its historical and future estimated earnings and cash flow.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

If you're looking to trade Carl Zeiss Meditec, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:AFX

Carl Zeiss Meditec

Operates as a medical technology company in Germany, rest of Europe, North America, and Asia.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Community Narratives