Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that aap Implantate AG (ETR:AAQ1) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for aap Implantate

What Is aap Implantate's Net Debt?

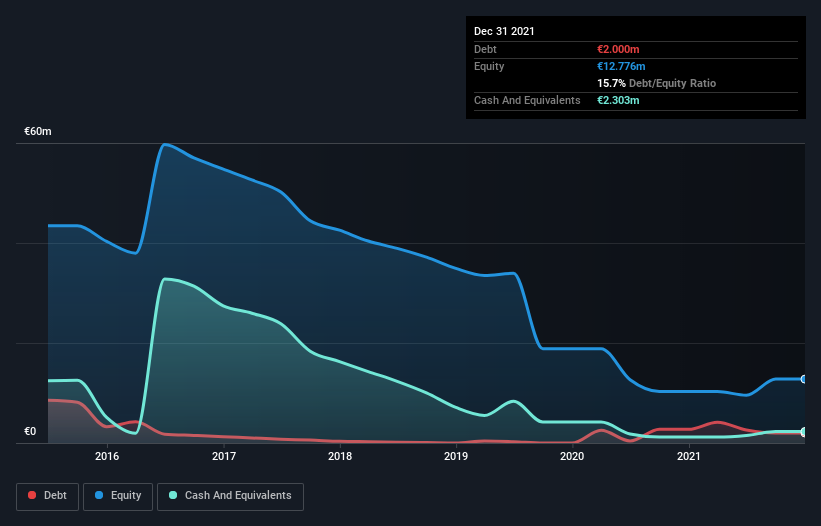

You can click the graphic below for the historical numbers, but it shows that aap Implantate had €2.00m of debt in December 2021, down from €2.74m, one year before. However, it does have €2.30m in cash offsetting this, leading to net cash of €303.0k.

How Healthy Is aap Implantate's Balance Sheet?

According to the last reported balance sheet, aap Implantate had liabilities of €6.34m due within 12 months, and liabilities of €3.84m due beyond 12 months. Offsetting this, it had €2.30m in cash and €3.10m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by €4.78m.

While this might seem like a lot, it is not so bad since aap Implantate has a market capitalization of €15.3m, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt. Despite its noteworthy liabilities, aap Implantate boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine aap Implantate's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, aap Implantate reported revenue of €14m, which is a gain of 46%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is aap Implantate?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months aap Implantate lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through €3.0m of cash and made a loss of €2.5m. Given it only has net cash of €303.0k, the company may need to raise more capital if it doesn't reach break-even soon. aap Implantate's revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. By investing before those profits, shareholders take on more risk in the hope of bigger rewards. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 4 warning signs for aap Implantate (2 don't sit too well with us!) that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you're looking to trade aap Implantate, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:AAQ1

aap Implantate

Develops, manufactures, and markets trauma products for orthopedics.

Low with weak fundamentals.

Market Insights

Community Narratives