Investors Appear Satisfied With Berentzen-Gruppe Aktiengesellschaft's (ETR:BEZ) Prospects

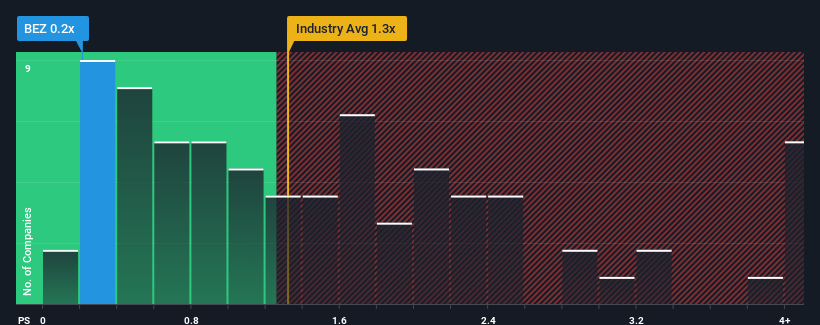

It's not a stretch to say that Berentzen-Gruppe Aktiengesellschaft's (ETR:BEZ) price-to-sales (or "P/S") ratio of 0.2x right now seems quite "middle-of-the-road" for companies in the Beverage industry in Germany, where the median P/S ratio is around 0.5x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for Berentzen-Gruppe

What Does Berentzen-Gruppe's Recent Performance Look Like?

With revenue growth that's inferior to most other companies of late, Berentzen-Gruppe has been relatively sluggish. One possibility is that the P/S ratio is moderate because investors think this lacklustre revenue performance will turn around. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on Berentzen-Gruppe will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For Berentzen-Gruppe?

The only time you'd be comfortable seeing a P/S like Berentzen-Gruppe's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. Still, the latest three year period was better as it's delivered a decent 24% overall rise in revenue. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 4.4% per annum over the next three years. With the industry predicted to deliver 4.2% growth each year, the company is positioned for a comparable revenue result.

With this information, we can see why Berentzen-Gruppe is trading at a fairly similar P/S to the industry. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Bottom Line On Berentzen-Gruppe's P/S

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

A Berentzen-Gruppe's P/S seems about right to us given the knowledge that analysts are forecasting a revenue outlook that is similar to the Beverage industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. All things considered, if the P/S and revenue estimates contain no major shocks, then it's hard to see the share price moving strongly in either direction in the near future.

There are also other vital risk factors to consider and we've discovered 2 warning signs for Berentzen-Gruppe (1 is a bit unpleasant!) that you should be aware of before investing here.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Berentzen-Gruppe might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:BEZ

Berentzen-Gruppe

Produces and distributes spirits and non-alcoholic beverages in Germany, rest of Europe Union, rest of Europe, and internationally.

Undervalued with adequate balance sheet.