- Germany

- /

- Industrials

- /

- XTRA:SIE

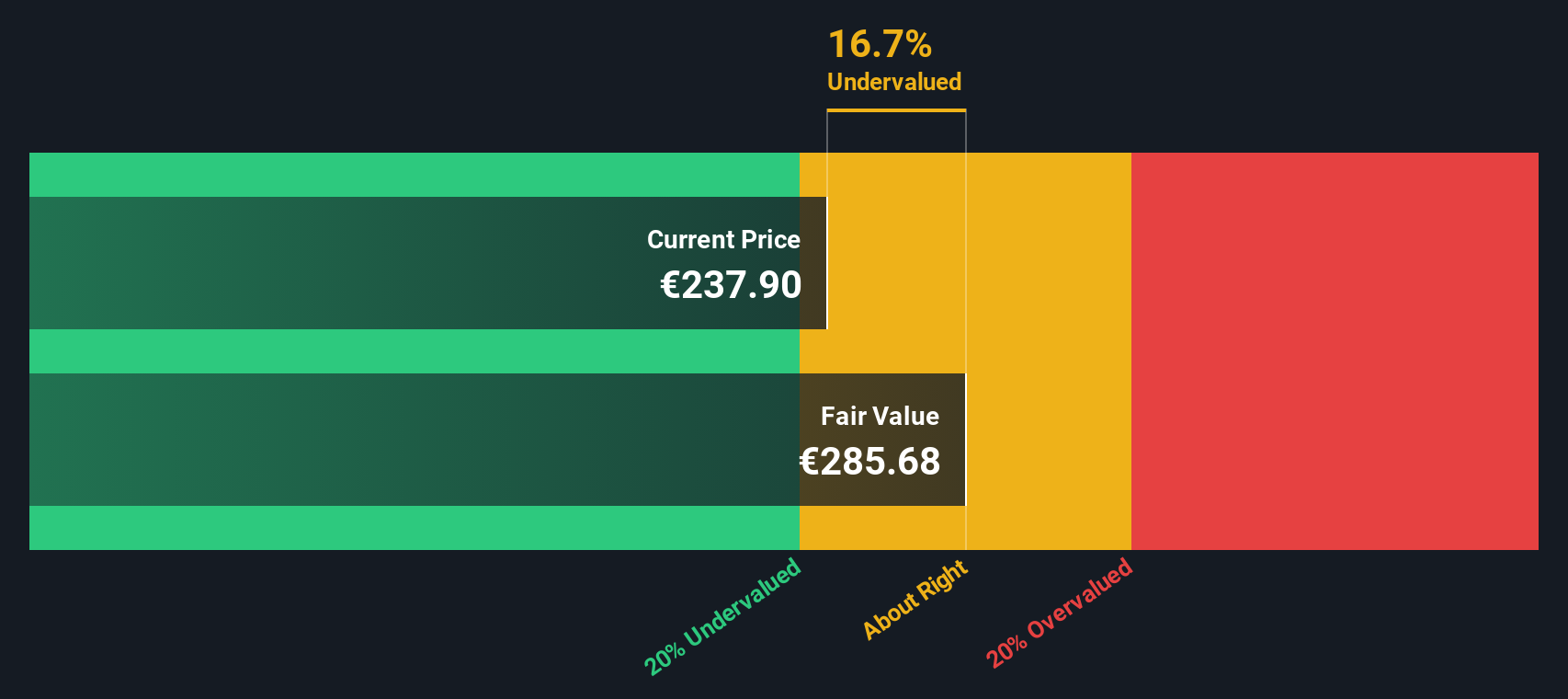

Siemens (XTRA:SIE) Announces Major Product Update and Dividend Increase, Strengthening Market Position

Reviewed by Simply Wall St

See the full analysis report here for a deeper understanding of Siemens.

Key Assets Propelling Valmont Industries Forward

Valmont Industries has demonstrated remarkable financial growth, with earnings surging by 89.5% over the past year, far surpassing its five-year average of 9.4%. This impressive performance is complemented by an increase in net profit margin, which improved from 3.7% to 7.4% over the last year. Additionally, the company's dividend payments have been consistently stable over the past decade, with a low payout ratio of 16.2%, underscoring strong coverage by earnings and cash flows. This financial strength is further supported by the fact that shareholders have not experienced dilution in the past year. Valmont's valuation is also compelling, with a Price-To-Earnings Ratio of 22.2x, which is lower than both the peer average of 32.8x and the US Construction industry average of 31.4x, trading significantly below the SWS fair value of $476.64.

Internal Limitations Hindering Valmont Industries's Growth

Valmont Industries faces some challenges. The company's Return on Equity stands at 19.3%, slightly below the 20% threshold considered strong. Moreover, its revenue growth is forecasted at 3.1% per year, which is slower than the US market average of 9.1%. Additionally, the company's net debt to equity ratio is 44.2%, exceeding the 40% threshold, indicating a relatively high level of leverage. These factors suggest that while Valmont's financial health is strong, there are areas where it lags behind industry standards, potentially impacting its competitive position.

Areas for Expansion and Innovation for Valmont Industries

Looking ahead, Valmont Industries has promising opportunities for growth. The company's earnings are projected to grow at a rate of 9.03% per year, highlighting its potential for future profitability. Furthermore, trading at 30.5% below its estimated fair value presents a significant opportunity for price appreciation. This undervaluation could attract investors seeking to capitalize on the company's growth trajectory. By leveraging these opportunities, Valmont can enhance its market position and drive performance, potentially increasing its market share in the future.

External Factors Threatening Valmont Industries

However, Valmont Industries must navigate several external threats. The high level of debt poses risks to its financial stability, potentially affecting its ability to invest in growth initiatives. Additionally, significant insider selling over the past three months may indicate a lack of confidence from insiders, which could influence investor sentiment. These factors, combined with broader economic uncertainties, highlight the need for Valmont to strategically manage its financial and operational risks to sustain its growth momentum.

To gain deeper insights into Siemens's historical performance, explore our detailed analysis of past performance.To learn about how Siemens's valuation metrics are shaping its market position, check out our detailed analysis of Siemens's Valuation.See what the latest analyst reports say about Siemens's future prospects and potential market movements.Explore the current health of Siemens and how it reflects on its financial stability and growth potential.Conclusion

Valmont Industries has exhibited significant financial growth, with earnings rising by 89.5% in the past year, indicating strong operational efficiency and profitability. This is further supported by an improved net profit margin and stable dividend payments, reflecting sound financial management. While facing challenges such as a slightly lower Return on Equity and higher leverage, Valmont's Price-To-Earnings Ratio of 22.2x, which is lower than both its peers and the industry average, positions it as an attractive investment opportunity. Trading well below its estimated fair value of $476.64, the company presents a compelling case for potential price appreciation. However, to sustain its growth trajectory, Valmont must address its debt levels and manage external threats, ensuring strategic investments in growth initiatives to enhance its competitive edge and market position.

Taking Advantage

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:SIE

Siemens

A technology company, focuses in the areas of automation and digitalization in Europe, Commonwealth of Independent States, Africa, the Middle East, the Americas, Asia, and Australia.

Established dividend payer and good value.