Advertisement

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Krones (ETR:KRN). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

View our latest analysis for Krones

How Fast Is Krones Growing Its Earnings Per Share?

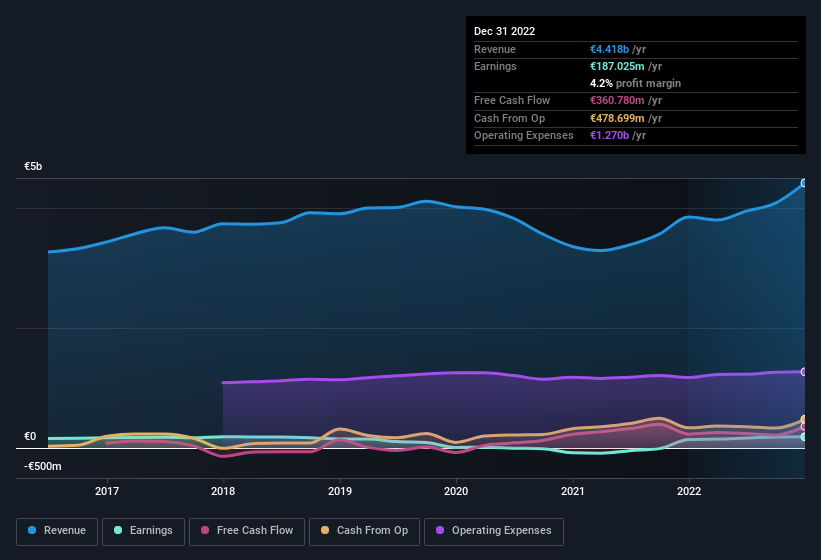

Krones has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. Thus, it makes sense to focus on more recent growth rates, instead. To the delight of shareholders, Krones' EPS soared from €4.47 to €5.92, over the last year. That's a fantastic gain of 32%.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. It's noted that Krones' revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. Krones maintained stable EBIT margins over the last year, all while growing revenue 15% to €4.4b. That's a real positive.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Krones' forecast profits?

Are Krones Insiders Aligned With All Shareholders?

Seeing insiders owning a large portion of the shares on issue is often a good sign. Their incentives will be aligned with the investors and there's less of a probability in a sudden sell-off that would impact the share price. So we're pleased to report that Krones insiders own a meaningful share of the business. Owning 37% of the company, insiders have plenty riding on the performance of the the share price. This should be a welcoming sign for investors because it suggests that the people making the decisions are also impacted by their choices. At the current share price, that insider holding is worth a staggering €1.3b. This is an incredible endorsement from them.

While it's always good to see some strong conviction in the company from insiders through heavy investment, it's also important for shareholders to ask if management compensation policies are reasonable. Our quick analysis into CEO remuneration would seem to indicate they are. The median total compensation for CEOs of companies similar in size to Krones, with market caps between €1.8b and €5.8b, is around €2.4m.

The Krones CEO received €1.7m in compensation for the year ending December 2021. That is actually below the median for CEO's of similarly sized companies. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of a culture of integrity, in a broader sense.

Does Krones Deserve A Spot On Your Watchlist?

You can't deny that Krones has grown its earnings per share at a very impressive rate. That's attractive. If you need more convincing beyond that EPS growth rate, don't forget about the reasonable remuneration and the high insider ownership. The overarching message here is that Krones has underlying strengths that make it worth a look at. It's still necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Krones , and understanding this should be part of your investment process.

Although Krones certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see insider buying, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Krones might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:KRN

Krones

Engages in the planning, development, and manufacture of machines and lines for the production, filling, and packaging technology for the food and beverage industry in Germany and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor