- Germany

- /

- Electrical

- /

- XTRA:ENR

3 Stocks Estimated To Be Up To 48% Below Intrinsic Value

Reviewed by Simply Wall St

As global markets navigate a mixed start to the new year, with U.S. stocks closing out a strong 2024 despite some recent volatility, investors are keenly observing economic indicators like the Chicago PMI and GDP forecasts for signs of future trends. In this environment of fluctuating indices and economic uncertainty, identifying undervalued stocks that are trading below their intrinsic value can offer potential opportunities for investors seeking to optimize their portfolios.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Dime Community Bancshares (NasdaqGS:DCOM) | US$30.89 | US$61.61 | 49.9% |

| Wasion Holdings (SEHK:3393) | HK$7.05 | HK$14.02 | 49.7% |

| Tourmaline Oil (TSX:TOU) | CA$66.79 | CA$133.01 | 49.8% |

| Camden National (NasdaqGS:CAC) | US$42.08 | US$83.90 | 49.8% |

| S Foods (TSE:2292) | ¥2737.00 | ¥5472.35 | 50% |

| Zhende Medical (SHSE:603301) | CN¥21.00 | CN¥41.99 | 50% |

| Ally Financial (NYSE:ALLY) | US$35.85 | US$71.62 | 49.9% |

| Shandong Weigao Orthopaedic Device (SHSE:688161) | CN¥23.89 | CN¥47.76 | 50% |

| SkyCity Entertainment Group (NZSE:SKC) | NZ$1.45 | NZ$2.89 | 49.8% |

| LG Energy Solution (KOSE:A373220) | ₩356000.00 | ₩709677.60 | 49.8% |

Here we highlight a subset of our preferred stocks from the screener.

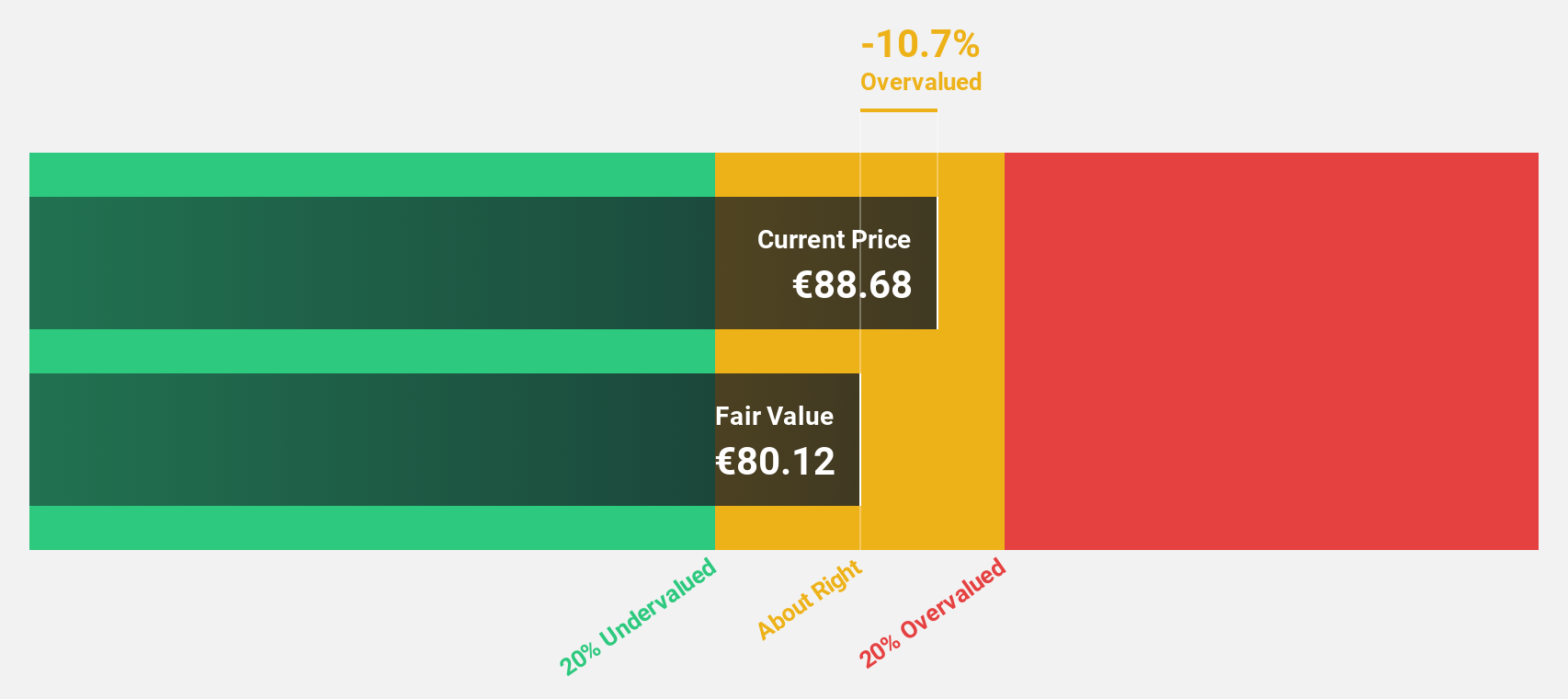

Pharma Mar (BME:PHM)

Overview: Pharma Mar, S.A. is a biopharmaceutical company focused on the research, development, production, and commercialization of bio-active principles for oncology across various international markets with a market cap of €1.44 billion.

Operations: The company's revenue primarily comes from its oncology segment, which generated €154.75 million.

Estimated Discount To Fair Value: 48%

Pharma Mar is trading at €82.85, significantly below its estimated fair value of €159.19, suggesting it may be undervalued based on discounted cash flow analysis. Despite recent volatility and a slight decline in net income to €7.44 million for the first nine months of 2024, earnings are forecast to grow substantially at 56.2% annually over the next three years, outpacing the Spanish market's growth rate. Revenue is also projected to increase by 25.4% per year, driven by positive clinical trial results for Zepzelca®.

- Our earnings growth report unveils the potential for significant increases in Pharma Mar's future results.

- Take a closer look at Pharma Mar's balance sheet health here in our report.

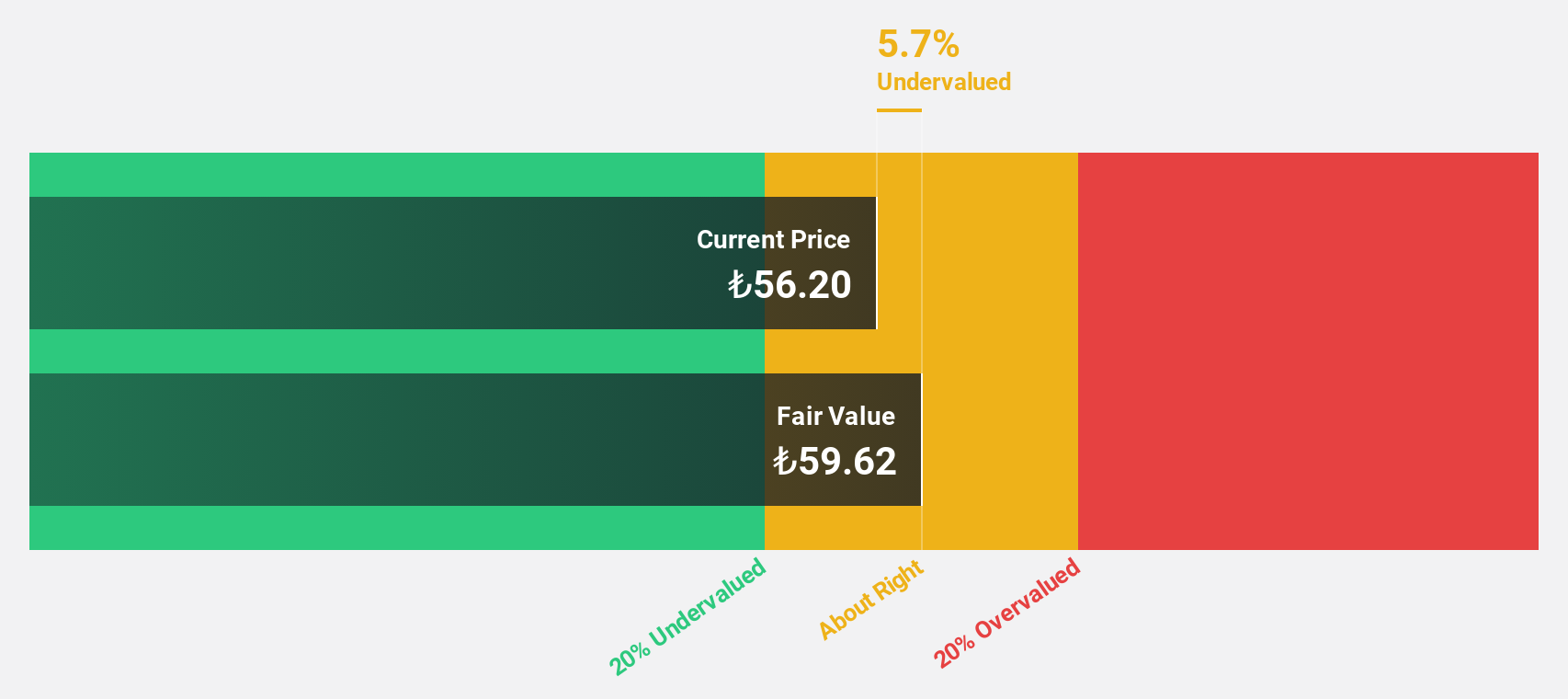

Türk Telekomünikasyon Anonim Sirketi (IBSE:TTKOM)

Overview: Türk Telekomünikasyon Anonim Sirketi, along with its subsidiaries, offers integrated telecommunication services in Turkey and has a market cap of TRY159.53 billion.

Operations: The company generates revenue from its Mobile segment with TRY45.38 billion and Fixed-Line segment with TRY67.30 billion.

Estimated Discount To Fair Value: 10.7%

Türk Telekomünikasyon Anonim Sirketi, trading at TRY 45.58, is slightly below its estimated fair value of TRY 51.04, indicating potential undervaluation based on cash flows. Despite a decline in quarterly net income to TRY 1.14 billion from TRY 3.04 billion last year, the company forecasts robust revenue growth of 26.6% annually and earnings growth of 32.21% per year, albeit slower than the Turkish market's projected rate of 34.8%.

- Insights from our recent growth report point to a promising forecast for Türk Telekomünikasyon Anonim Sirketi's business outlook.

- Click to explore a detailed breakdown of our findings in Türk Telekomünikasyon Anonim Sirketi's balance sheet health report.

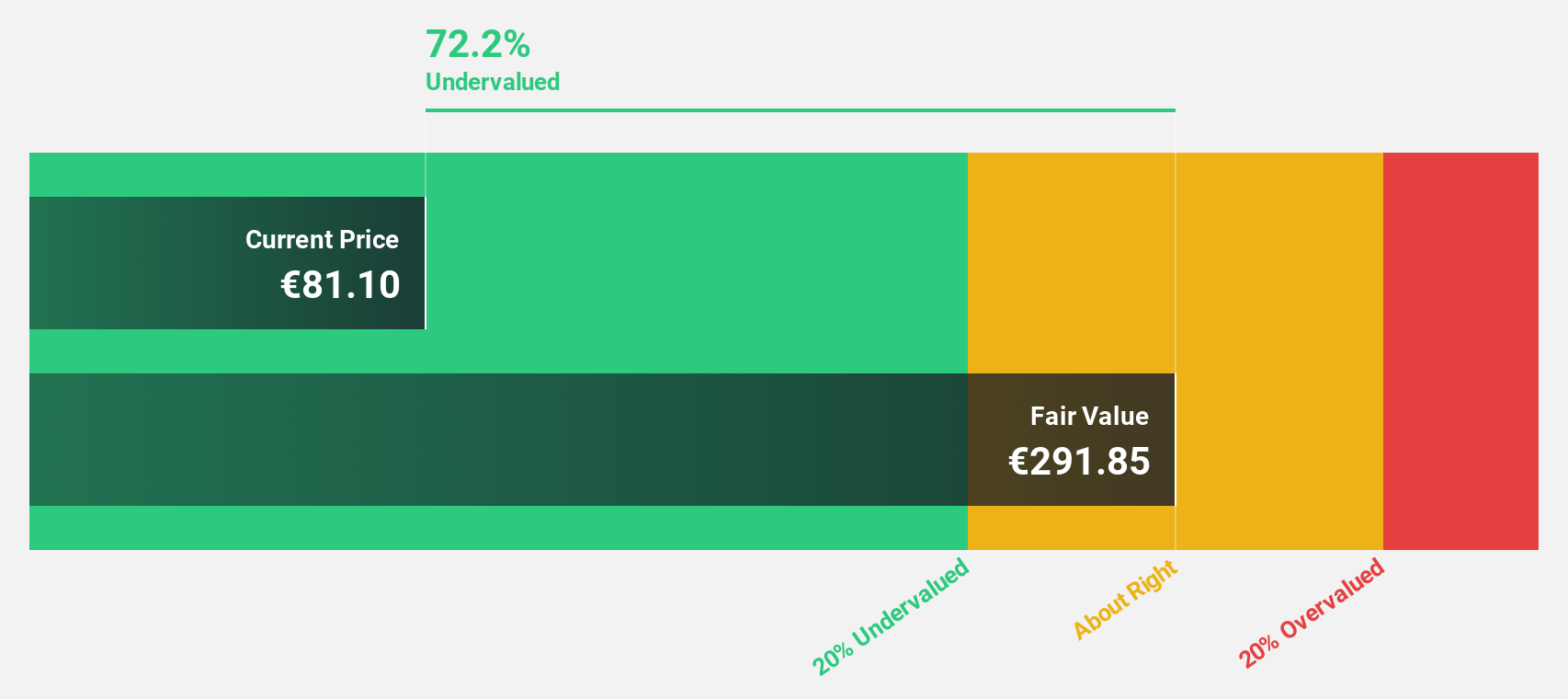

Siemens Energy (XTRA:ENR)

Overview: Siemens Energy AG is a global energy technology company with a market cap of approximately €41.07 billion.

Operations: The company generates revenue through its Gas Services (€10.80 billion), Siemens Gamesa (€10.01 billion), Grid Technologies (€9.28 billion), and Transformation of Industry (€5.11 billion) segments.

Estimated Discount To Fair Value: 18.6%

Siemens Energy, priced at €51.98, is trading 18.6% below its fair value estimate of €63.83, suggesting potential undervaluation based on cash flows. The company has returned to profitability this year with a net income of €1.18 billion and forecasts earnings growth of 22.07% annually over the next three years, outpacing the German market's growth rate. Recent discussions about selling its Indian wind assets could further impact its financial position positively if finalized.

- Our comprehensive growth report raises the possibility that Siemens Energy is poised for substantial financial growth.

- Click here to discover the nuances of Siemens Energy with our detailed financial health report.

Taking Advantage

- Navigate through the entire inventory of 899 Undervalued Stocks Based On Cash Flows here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:ENR

High growth potential with acceptable track record.