- Germany

- /

- Aerospace & Defense

- /

- XTRA:HAG

Hensoldt's (ETR:5UH) Shareholders Will Receive A Bigger Dividend Than Last Year

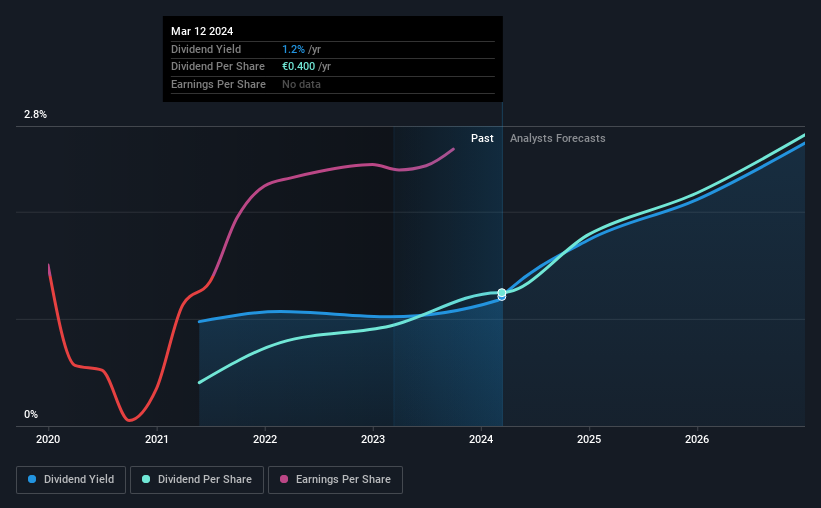

Hensoldt AG's (ETR:5UH) dividend will be increasing from last year's payment of the same period to €0.40 on 22nd of May. This takes the annual payment to 1.2% of the current stock price, which is about average for the industry.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Investors will be pleased to see that Hensoldt's stock price has increased by 37% in the last 3 months, which is good for shareholders and can also explain a decrease in the dividend yield.

Check out our latest analysis for Hensoldt

Hensoldt's Earnings Easily Cover The Distributions

Solid dividend yields are great, but they only really help us if the payment is sustainable. Before making this announcement, Hensoldt was paying a whopping 96% as a dividend, but this only made up 35% of its overall earnings. A cash payout ratio this high could put the dividend under pressure and force the company to reduce it in the future if it were to run into tough times.

The next year is set to see EPS grow by 134.5%. If the dividend continues along recent trends, we estimate the payout ratio will be 27%, which is in the range that makes us comfortable with the sustainability of the dividend.

Hensoldt Doesn't Have A Long Payment History

The dividend hasn't seen any major cuts in the past, but the company has only been paying a dividend for 3 years, which isn't that long in the grand scheme of things. Since 2021, the dividend has gone from €0.13 total annually to €0.40. This means that it has been growing its distributions at 45% per annum over that time. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Hensoldt has seen EPS rising for the last three years, at 89% per annum. Rapid earnings growth and a low payout ratio suggest this company has been effectively reinvesting in its business. Should that continue, this company could have a bright future.

Our Thoughts On Hensoldt's Dividend

In summary, while it's always good to see the dividend being raised, we don't think Hensoldt's payments are rock solid. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would probably look elsewhere for an income investment.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Just as an example, we've come across 2 warning signs for Hensoldt you should be aware of, and 1 of them shouldn't be ignored. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

If you're looking to trade Hensoldt, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hensoldt might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:HAG

Hensoldt

HENSOLDT AG, together with its subsidiaries, provides defense and security electronic sensor solutions worldwide.

High growth potential with solid track record.