Advertisement

- China

- /

- Water Utilities

- /

- SHSE:600168

Is Wuhan Sanzhen Industry HoldingLtd (SHSE:600168) A Risky Investment?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Wuhan Sanzhen Industry Holding Co.,Ltd (SHSE:600168) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Wuhan Sanzhen Industry HoldingLtd

What Is Wuhan Sanzhen Industry HoldingLtd's Debt?

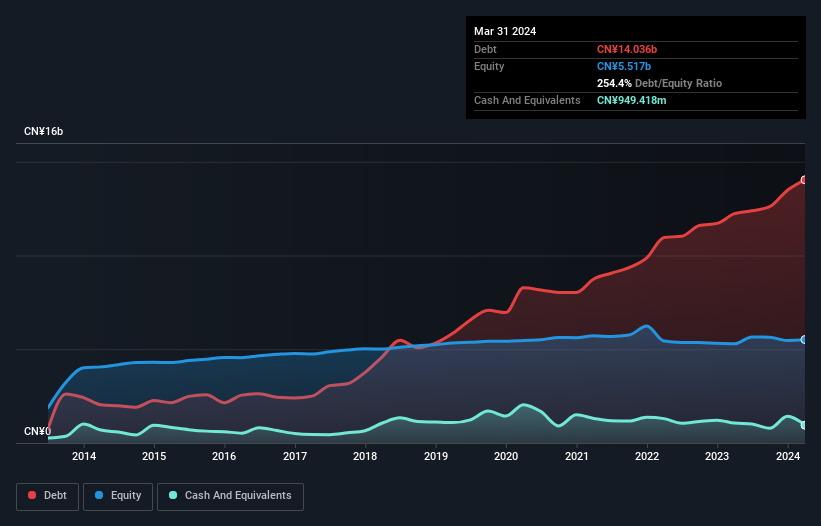

The image below, which you can click on for greater detail, shows that at March 2024 Wuhan Sanzhen Industry HoldingLtd had debt of CN¥14.0b, up from CN¥12.2b in one year. On the flip side, it has CN¥949.4m in cash leading to net debt of about CN¥13.1b.

A Look At Wuhan Sanzhen Industry HoldingLtd's Liabilities

The latest balance sheet data shows that Wuhan Sanzhen Industry HoldingLtd had liabilities of CN¥9.52b due within a year, and liabilities of CN¥7.56b falling due after that. On the other hand, it had cash of CN¥949.4m and CN¥6.30b worth of receivables due within a year. So its liabilities total CN¥9.83b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the CN¥3.98b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Wuhan Sanzhen Industry HoldingLtd would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Wuhan Sanzhen Industry HoldingLtd shareholders face the double whammy of a high net debt to EBITDA ratio (11.2), and fairly weak interest coverage, since EBIT is just 0.89 times the interest expense. The debt burden here is substantial. On the other hand, Wuhan Sanzhen Industry HoldingLtd grew its EBIT by 22% in the last year. If it can maintain that kind of improvement, its debt load will begin to melt away like glaciers in a warming world. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Wuhan Sanzhen Industry HoldingLtd will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Wuhan Sanzhen Industry HoldingLtd burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both Wuhan Sanzhen Industry HoldingLtd's conversion of EBIT to free cash flow and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. But at least it's pretty decent at growing its EBIT; that's encouraging. It's also worth noting that Wuhan Sanzhen Industry HoldingLtd is in the Water Utilities industry, which is often considered to be quite defensive. Taking into account all the aforementioned factors, it looks like Wuhan Sanzhen Industry HoldingLtd has too much debt. While some investors love that sort of risky play, it's certainly not our cup of tea. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 4 warning signs we've spotted with Wuhan Sanzhen Industry HoldingLtd (including 2 which can't be ignored) .

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Wuhan Sanzhen Industry HoldingLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:600168

Wuhan Sanzhen Industry HoldingLtd

Engages in the tap water production and supply activities in China.

Low and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor