Advertisement

- Hong Kong

- /

- Entertainment

- /

- SEHK:2400

Discover XD And 2 More Stocks Estimated To Be Trading At A Discount

Simply Wall St

Reviewed by Simply Wall St

In the wake of a U.S. election resulting in a "red sweep," global markets have seen significant movements, with major benchmarks like the S&P 500 reaching record highs amid expectations of policy shifts that could influence growth and inflation. As investors navigate these changing economic landscapes, identifying undervalued stocks becomes crucial; such stocks often present opportunities when their intrinsic value appears higher than their current market price, particularly in times of market optimism and regulatory changes.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| UMB Financial (NasdaqGS:UMBF) | US$122.86 | US$245.13 | 49.9% |

| Taiwan Union Technology (TPEX:6274) | NT$156.00 | NT$311.03 | 49.8% |

| KMC (Kuei Meng) International (TWSE:5306) | NT$125.00 | NT$249.85 | 50% |

| PharmaResearch (KOSDAQ:A214450) | ₩219000.00 | ₩437485.60 | 49.9% |

| Cambi (OB:CAMBI) | NOK15.10 | NOK30.14 | 49.9% |

| TBC Bank Group (LSE:TBCG) | £31.35 | £62.68 | 50% |

| Afya (NasdaqGS:AFYA) | US$16.16 | US$32.25 | 49.9% |

| Decisive Dividend (TSXV:DE) | CA$6.05 | CA$12.06 | 49.8% |

| XPEL (NasdaqCM:XPEL) | US$45.46 | US$90.91 | 50% |

| Grupo Traxión. de (BMV:TRAXION A) | MX$19.39 | MX$38.77 | 50% |

Let's take a closer look at a couple of our picks from the screened companies.

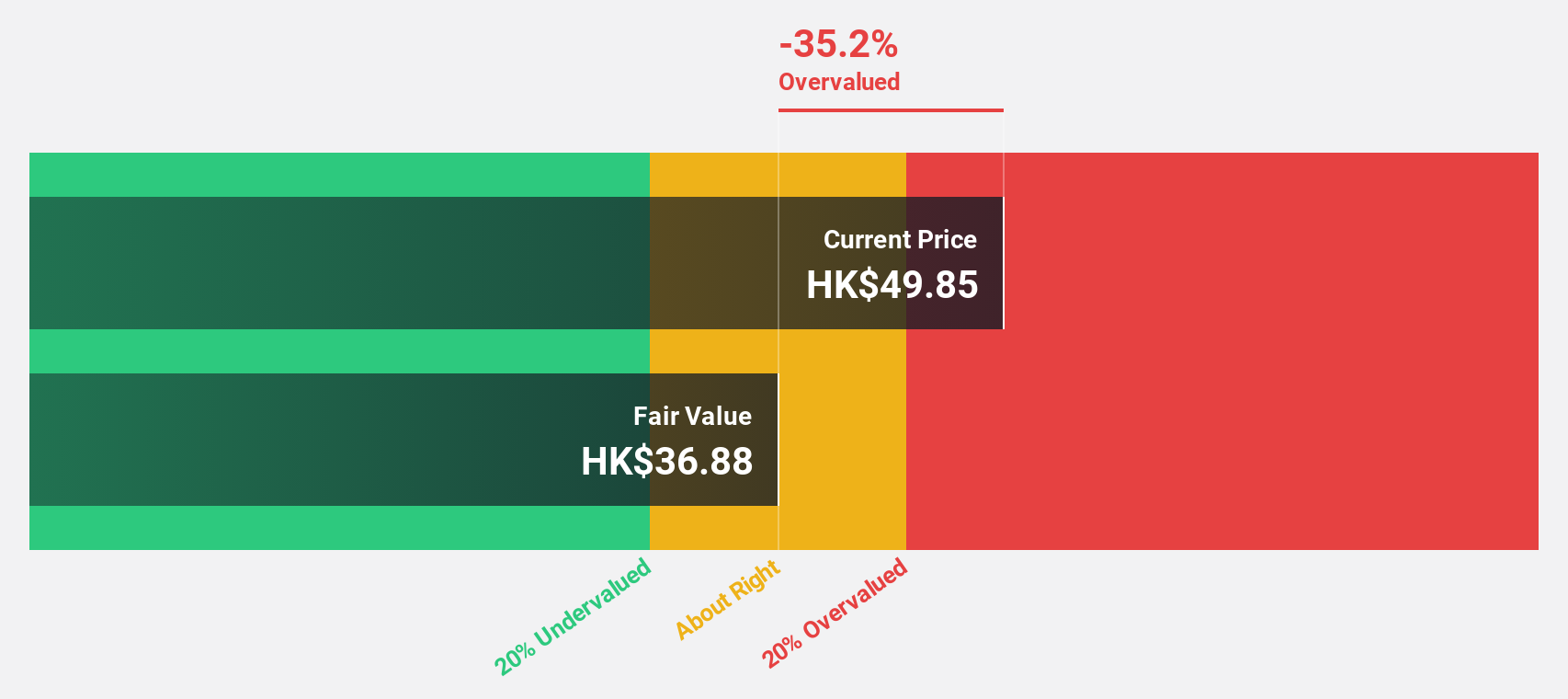

XD (SEHK:2400)

Overview: XD Inc. is an investment holding company that focuses on developing, publishing, operating, and distributing mobile and web games in Mainland China and internationally, with a market cap of HK$10.17 billion.

Operations: The company's revenue segments consist of CN¥2.43 billion from Game operations and CN¥1.43 billion from the TapTap Platform.

Estimated Discount To Fair Value: 49.6%

XD is trading at HK$22.4, significantly below its estimated fair value of HK$44.41, indicating potential undervaluation based on cash flows. The company's earnings are expected to grow substantially at 51.9% annually over the next three years, outpacing the Hong Kong market's growth rate of 11.7%. Despite past shareholder dilution, XD became profitable this year with net income rising from CNY 90.19 million to CNY 205.1 million in the first half of 2024.

- Our expertly prepared growth report on XD implies its future financial outlook may be stronger than recent results.

- Navigate through the intricacies of XD with our comprehensive financial health report here.

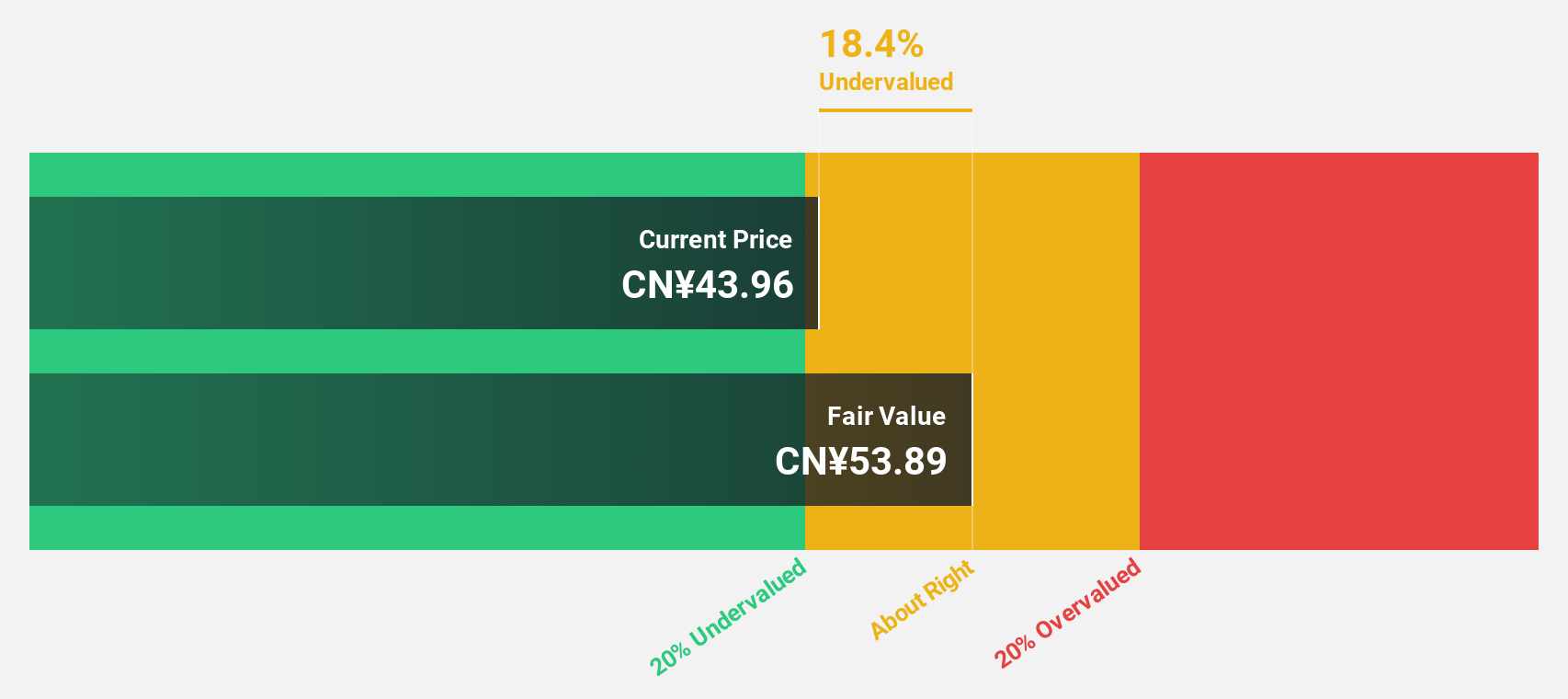

Electric Connector Technology (SZSE:300679)

Overview: Electric Connector Technology Co., Ltd. focuses on the research, design, development, manufacture, sale, and marketing of electronic connectors and interconnection system products globally with a market cap of CN¥19.95 billion.

Operations: The company generates revenue of CN¥3.89 billion from the connector industry segment.

Estimated Discount To Fair Value: 13%

Electric Connector Technology reported a strong performance with net income rising to CNY 458.59 million for the nine months ended September 2024, compared to CNY 247.4 million a year ago. Trading at CN¥46.91, it is priced below its estimated fair value of CN¥53.93, suggesting undervaluation based on cash flows. The company's earnings are expected to grow significantly at 28.4% annually over the next three years, surpassing market averages despite low forecasted return on equity of 16.8%.

- Insights from our recent growth report point to a promising forecast for Electric Connector Technology's business outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Electric Connector Technology.

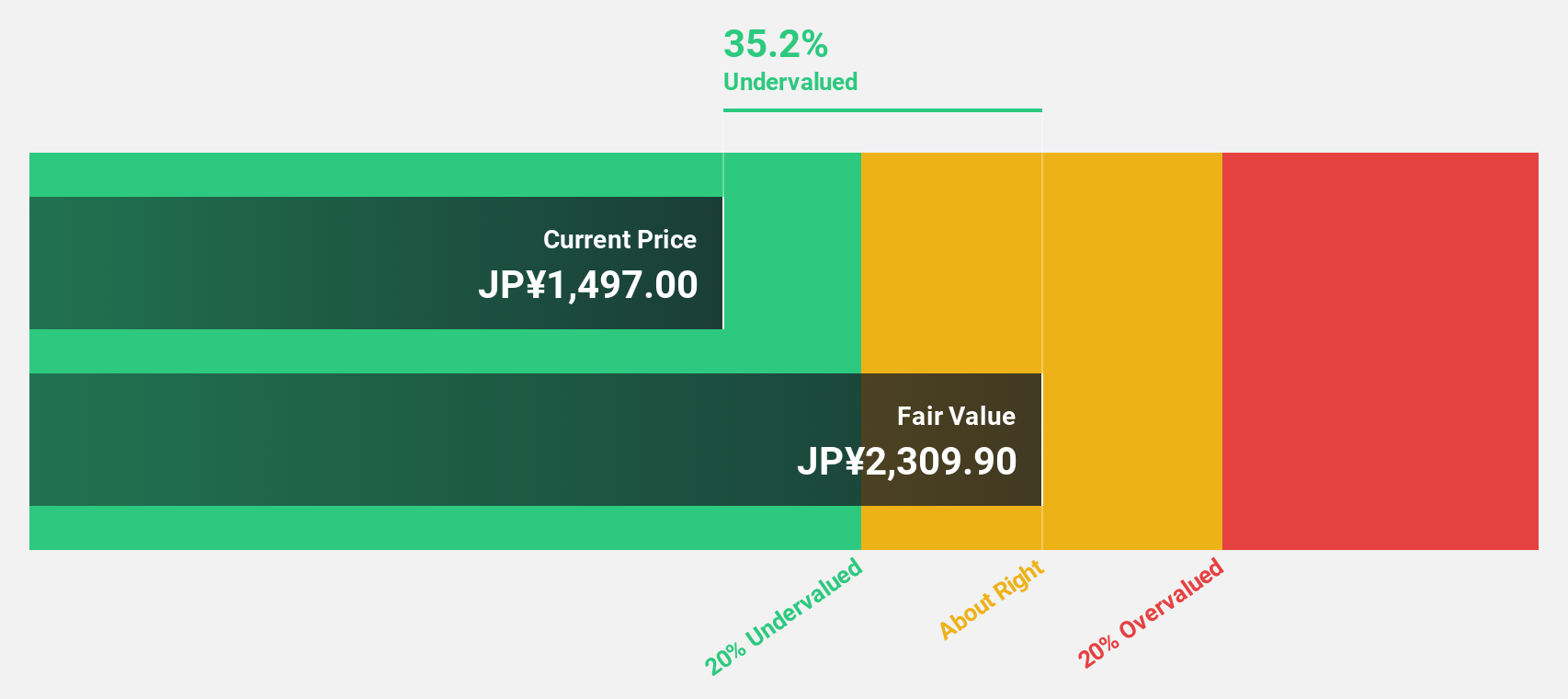

Avant Group (TSE:3836)

Overview: Avant Group Corporation, with a market cap of ¥74.29 billion, operates through its subsidiaries to offer accounting, business intelligence, and outsourcing services.

Operations: The company generates revenue from accounting services, business intelligence solutions, and outsourcing activities.

Estimated Discount To Fair Value: 46.1%

Avant Group, trading at ¥2044, is significantly undervalued with a fair value estimate of ¥3789.74. Despite recent share price volatility, its earnings grew by 35.2% last year and are projected to rise 18.1% annually, outpacing the JP market's average growth rate. The company completed a share buyback worth ¥828.93 million, enhancing shareholder value while maintaining robust revenue growth forecasts of 15.8% per year against the market's 4.2%.

- The analysis detailed in our Avant Group growth report hints at robust future financial performance.

- Click here to discover the nuances of Avant Group with our detailed financial health report.

Taking Advantage

- Click here to access our complete index of 900 Undervalued Stocks Based On Cash Flows.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2400

XD

An investment holding company, develops, publishes, operates, and distributes mobile and web games in Mainland China and internationally.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor