Advertisement

- China

- /

- Electronic Equipment and Components

- /

- SZSE:300440

What Chengdu Yunda Technology Co., Ltd.'s (SZSE:300440) 45% Share Price Gain Is Not Telling You

Chengdu Yunda Technology Co., Ltd. (SZSE:300440) shareholders have had their patience rewarded with a 45% share price jump in the last month. Notwithstanding the latest gain, the annual share price return of 2.1% isn't as impressive.

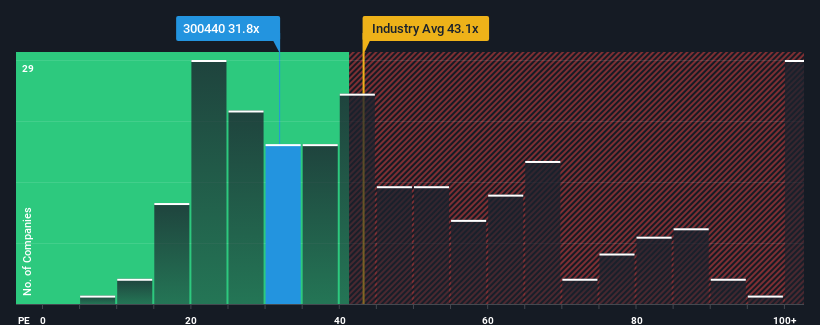

Even after such a large jump in price, it's still not a stretch to say that Chengdu Yunda Technology's price-to-earnings (or "P/E") ratio of 31.8x right now seems quite "middle-of-the-road" compared to the market in China, where the median P/E ratio is around 34x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Chengdu Yunda Technology certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. It might be that many expect the strong earnings performance to wane, which has kept the P/E from rising. If that doesn't eventuate, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

View our latest analysis for Chengdu Yunda Technology

How Is Chengdu Yunda Technology's Growth Trending?

The only time you'd be comfortable seeing a P/E like Chengdu Yunda Technology's is when the company's growth is tracking the market closely.

Retrospectively, the last year delivered an exceptional 254% gain to the company's bottom line. Still, incredibly EPS has fallen 23% in total from three years ago, which is quite disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Comparing that to the market, which is predicted to deliver 37% growth in the next 12 months, the company's downward momentum based on recent medium-term earnings results is a sobering picture.

In light of this, it's somewhat alarming that Chengdu Yunda Technology's P/E sits in line with the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

The Bottom Line On Chengdu Yunda Technology's P/E

Its shares have lifted substantially and now Chengdu Yunda Technology's P/E is also back up to the market median. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Chengdu Yunda Technology currently trades on a higher than expected P/E since its recent earnings have been in decline over the medium-term. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the moderate P/E lower. If recent medium-term earnings trends continue, it will place shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Chengdu Yunda Technology (1 is significant) you should be aware of.

If you're unsure about the strength of Chengdu Yunda Technology's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300440

Chengdu Yunda Technology

Engages in the research and development, production, and sale of rail transit intelligent systems and solutions in China.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor