Advertisement

As global markets navigate a period of cautious optimism following the Federal Reserve's recent rate cuts and political uncertainties, investors are closely watching how these developments will impact broader economic trends. Amidst this backdrop, stocks with high insider ownership can be particularly appealing due to the potential alignment of interests between company insiders and shareholders. In such a volatile environment, companies where insiders have significant stakes may indicate confidence in long-term growth prospects, making them worth considering for those interested in growth opportunities.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Arctech Solar Holding (SHSE:688408) | 37.9% | 25.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 39.9% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 37.3% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.3% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 34.2% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.5% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Underneath we present a selection of stocks filtered out by our screen.

MilDef Group (OM:MILDEF)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MilDef Group AB (publ) develops, manufactures, and sells rugged IT solutions and special electronics primarily for the security and defense sectors, with a market cap of SEK4.77 billion.

Operations: The company generates revenue from its Computer Hardware segment, amounting to SEK1.14 billion.

Insider Ownership: 17%

Earnings Growth Forecast: 70.2% p.a.

MilDef Group is experiencing significant growth potential, with earnings projected to rise by 70.2% annually, outpacing the Swedish market. Despite trading below estimated fair value, insider activity shows more buying than selling recently. Recent contracts with the Swedish Defense Materiel Administration and BAE Systems highlight MilDef's strategic positioning in defense technology, securing deals worth up to SEK 407 million. However, a follow-on equity offering of SEK 499.99 million may dilute existing shareholder value.

- Delve into the full analysis future growth report here for a deeper understanding of MilDef Group.

- In light of our recent valuation report, it seems possible that MilDef Group is trading beyond its estimated value.

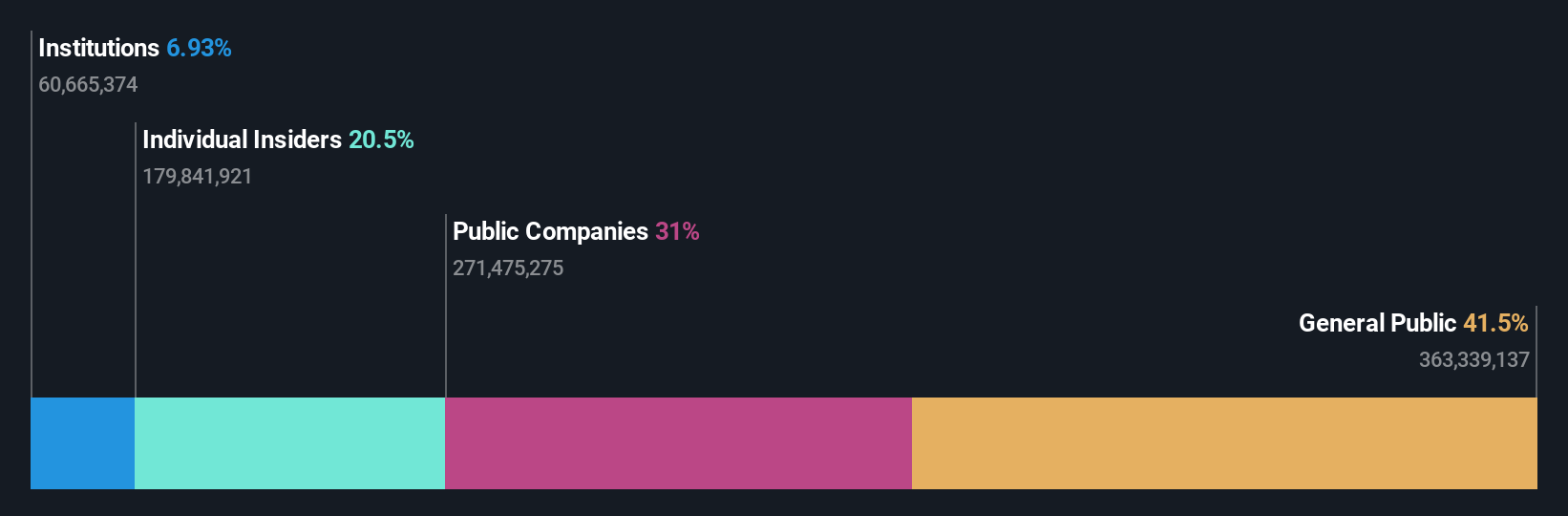

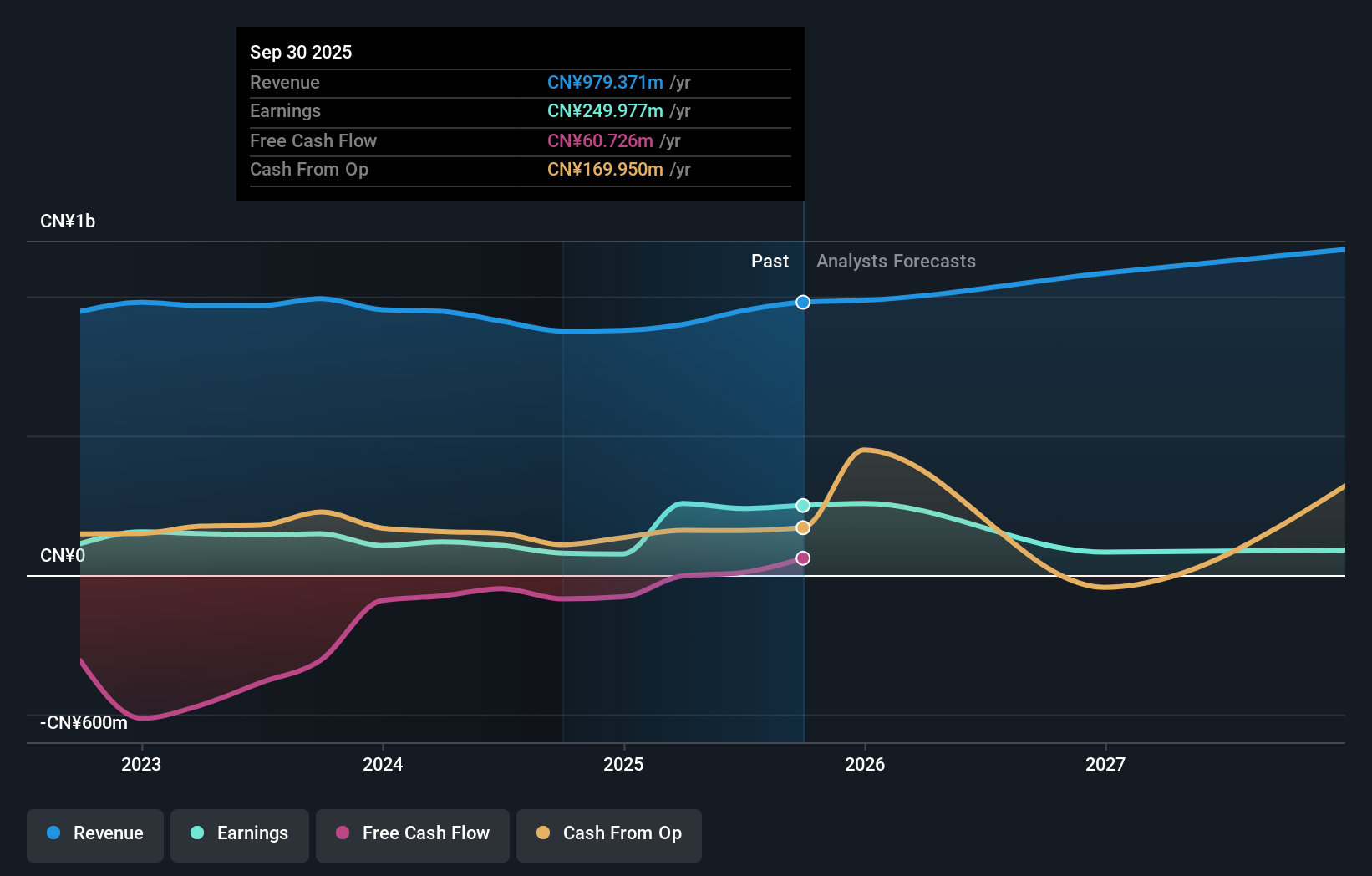

Jade Bird Fire (SZSE:002960)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Jade Bird Fire Co., Ltd. develops, manufactures, and sells professional fire safety electronic products and systems both in China and internationally, with a market cap of CN¥8.79 billion.

Operations: The company generates revenue from the development, manufacturing, and sales of specialized electronic products and systems for fire safety across domestic and international markets.

Insider Ownership: 23.2%

Earnings Growth Forecast: 30.8% p.a.

Jade Bird Fire's earnings are forecast to grow significantly at 30.83% per year, surpassing the Chinese market average. Despite a recent decline in net income to CNY 335.33 million for the first nine months of 2024, insider ownership remains strong with no substantial selling or buying activity reported recently. The company completed a share buyback program totaling CNY 100 million, potentially enhancing shareholder value and indicating management's confidence in future growth prospects.

- Take a closer look at Jade Bird Fire's potential here in our earnings growth report.

- The valuation report we've compiled suggests that Jade Bird Fire's current price could be quite moderate.

Zhejiang Truelove Vogue (SZSE:003041)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zhejiang Truelove Vogue Co., Ltd. engages in the research and development, design, manufacture, and sale of blankets in China with a market cap of CN¥4.02 billion.

Operations: The company's revenue primarily stems from its activities in research, design, production, and sales of blankets within the Chinese market.

Insider Ownership: 10.2%

Earnings Growth Forecast: 69.6% p.a.

Zhejiang Truelove Vogue's earnings are projected to grow significantly at 69.57% annually, outpacing the Chinese market average. Despite a decline in net income to CNY 56.14 million for the first nine months of 2024, revenue growth is expected at 29.7% per year, exceeding market expectations. Insider ownership remains stable with no recent substantial trading activity reported, although profit margins decreased from last year due to large one-off items impacting results.

- Unlock comprehensive insights into our analysis of Zhejiang Truelove Vogue stock in this growth report.

- Our expertly prepared valuation report Zhejiang Truelove Vogue implies its share price may be too high.

Summing It All Up

- Delve into our full catalog of 1512 Fast Growing Companies With High Insider Ownership here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Truelove Vogue might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:003041

Zhejiang Truelove Vogue

Research and development, designs, manufactures, and sells blankets in China.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor