Advertisement

- China

- /

- Electronic Equipment and Components

- /

- SZSE:002414

Investors Appear Satisfied With Wuhan Guide Infrared Co., Ltd.'s (SZSE:002414) Prospects As Shares Rocket 36%

Wuhan Guide Infrared Co., Ltd. (SZSE:002414) shareholders have had their patience rewarded with a 36% share price jump in the last month. Notwithstanding the latest gain, the annual share price return of 4.3% isn't as impressive.

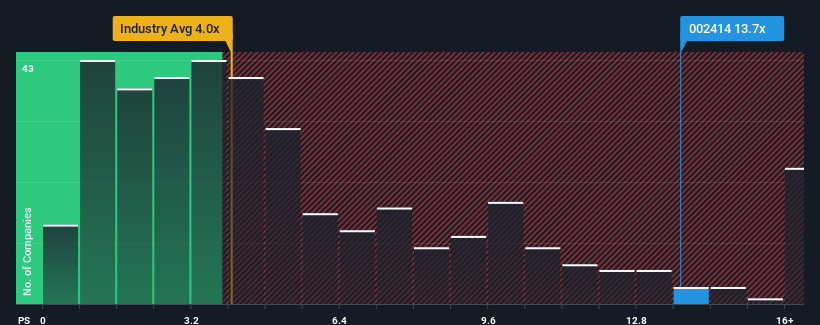

After such a large jump in price, Wuhan Guide Infrared may be sending very bearish signals at the moment with a price-to-sales (or "P/S") ratio of 13.7x, since almost half of all companies in the Electronic industry in China have P/S ratios under 4x and even P/S lower than 2x are not unusual. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Wuhan Guide Infrared

How Wuhan Guide Infrared Has Been Performing

Wuhan Guide Infrared could be doing better as it's been growing revenue less than most other companies lately. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Wuhan Guide Infrared will help you uncover what's on the horizon.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, Wuhan Guide Infrared would need to produce outstanding growth that's well in excess of the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 6.5% last year. Still, lamentably revenue has fallen 37% in aggregate from three years ago, which is disappointing. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Turning to the outlook, the next year should generate growth of 38% as estimated by the dual analysts watching the company. That's shaping up to be materially higher than the 26% growth forecast for the broader industry.

In light of this, it's understandable that Wuhan Guide Infrared's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Wuhan Guide Infrared's P/S

Shares in Wuhan Guide Infrared have seen a strong upwards swing lately, which has really helped boost its P/S figure. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Wuhan Guide Infrared's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Many other vital risk factors can be found on the company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Wuhan Guide Infrared with six simple checks.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Wuhan Guide Infrared might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002414

Wuhan Guide Infrared

Engages in the research and development, production, and sale of infrared thermal imaging technology in Asia.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.0% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|22.8% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|4.3% undervalued

RO

Community Contributor