- China

- /

- Electronic Equipment and Components

- /

- SZSE:002236

Zhejiang Dahua Technology Co., Ltd. (SZSE:002236) Stock Rockets 32% But Many Are Still Ignoring The Company

Zhejiang Dahua Technology Co., Ltd. (SZSE:002236) shareholders would be excited to see that the share price has had a great month, posting a 32% gain and recovering from prior weakness. Looking back a bit further, it's encouraging to see the stock is up 38% in the last year.

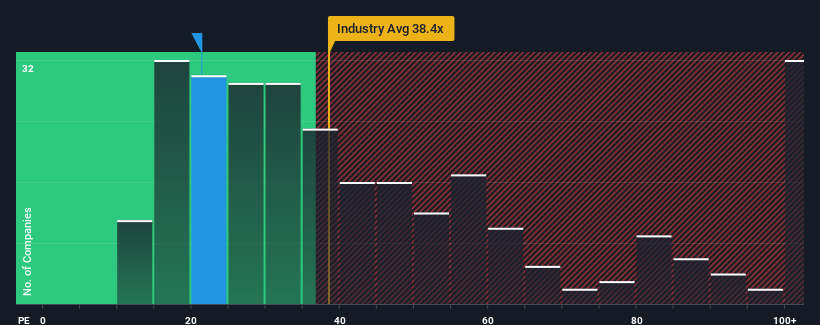

In spite of the firm bounce in price, Zhejiang Dahua Technology may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 21.3x, since almost half of all companies in China have P/E ratios greater than 31x and even P/E's higher than 56x are not unusual. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

Zhejiang Dahua Technology certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Zhejiang Dahua Technology

Does Growth Match The Low P/E?

Zhejiang Dahua Technology's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

If we review the last year of earnings growth, the company posted a terrific increase of 15%. Despite this strong recent growth, it's still struggling to catch up as its three-year EPS frustratingly shrank by 31% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 50% over the next year. That's shaping up to be materially higher than the 41% growth forecast for the broader market.

In light of this, it's peculiar that Zhejiang Dahua Technology's P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Final Word

Despite Zhejiang Dahua Technology's shares building up a head of steam, its P/E still lags most other companies. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Zhejiang Dahua Technology's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Zhejiang Dahua Technology you should know about.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Dahua Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002236

Zhejiang Dahua Technology

Operates in the intelligent Internet of Things industry worldwide.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Community Narratives